Corporate Hybrids: strong demand, diminishing reward?

Let’s start with a simple explanation of what a hybrid is: a perpetual bond that combines features of both debt and equity. Hybrids are subordinated to senior bonds but rank ahead of equity and possess equity-like features, such as loss-absorption and the ability to defer coupons.

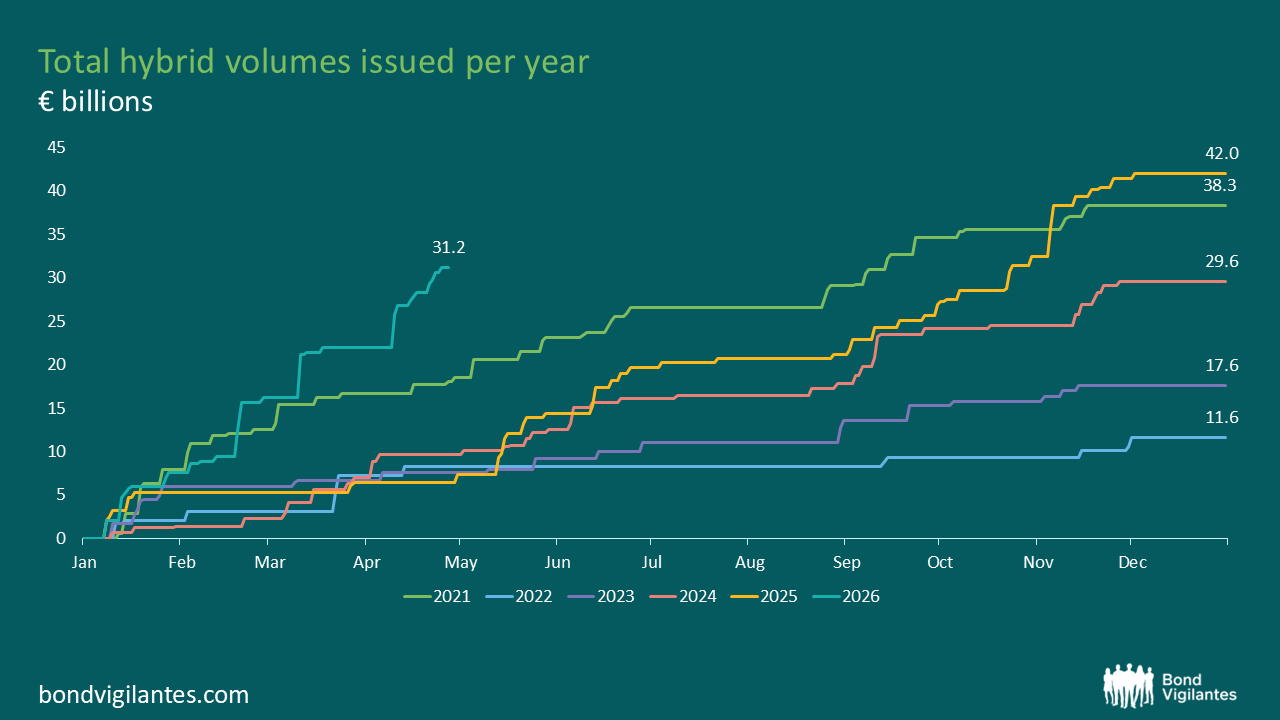

The corporate hybrid market has kicked off 2026 with a bang. Year‑to‑date gross issuance has already surpassed €31bn, well ahead of prior run‑rates (full‑year 2025 ended at €42bn). Indeed, we have already exceeded 2022 & 2023 FY supply.

Source: J.P. Morgan, European Credit Research – Corporate Bonds, issued 28 April 2026

In the past week alone we have seen over €3bn of supply, with issuance from Adecco, Abertis, Amprion, Var Energi and Grand City Properties. Order books were typically six times covered, with pricing tightening by 50bp from initial guidance. A clear signal of demand overwhelming supply.

We also saw the long-awaited blockbuster hybrid issuance from Stellantis in March; a €4bn dual‑tranche along with a £825m tranche. A nod to the expanding asset class and another great example of the demand for hybrids.

Of all the issuance we’ve seen, five‑year call structures have emerged as the market’s sweet spot. Here’s why – from both sides of the trade.

The investor perspective

As with most of the credit market today, valuations are stretched. I don’t think that’s up for debate given I have asked myself many times when looking at pricing “is that bid for the senior or subordinated bond?!”. The senior-sub spread has compressed to cycle tights; meaning subordinated risk offers far less compensation than it has done in many other periods.

Yet in a world driven by relentless yield‑seekers, some investors are looking for carry and beta that they can’t find elsewhere.

Coupons in the high-4% to 6% range are satisfying the carry argument.

With regard to the beta argument, the market is clearly telling us that investors are confident issuers will call their hybrids at the first opportunity. This was demonstrated by Grand City Properties this week. A higher-beta real estate issuer, with an outstanding hybrid paying a 1.5% coupon. The market has long-debated the motivations of issuers to call these low-reset hybrids, particularly in a higher all-in-yield environment. Repeated liability-management exercises like these are building confidence that issuers will indeed refinance. This appears to be providing a supportive technical for the market, as investors determine there is potential for additional capital gain, if bonds are called at above market pricing.

The final factor I’d like to discuss is liquidity. The investment-grade investor base dramatically outsizes the high-yield one. Therefore the liquidity in hybrids compared to high-yield bonds is vastly better. A €10-20m bid in an investment grade rated issuer with its hybrid rated at BB+ is very routine, whereas a €10-20m bid in a high-yield issuer BB+ bond, would be far less so.

Are all hybrids as compelling as one another?

Most attractive Short-dated calls (three to five years) are the sweet-spot; along with coupon income, they offer good rolldown yield (see recent blog on rolldown from Matt and Keith) – even in markets that trade sideways or in a modest move wider. Investors are highly confident these bonds will be called, given how efficient a capital tool they are for issuers.

Least attractive further out the curve, particularly beyond seven years. Hybrid curves are currently pricing very flat versus historical performance. Longer-calls present a different type of market beta and face greater risk of capital losses if the market does start to question whether the risks warrant greater scrutiny.

The issuer perspective

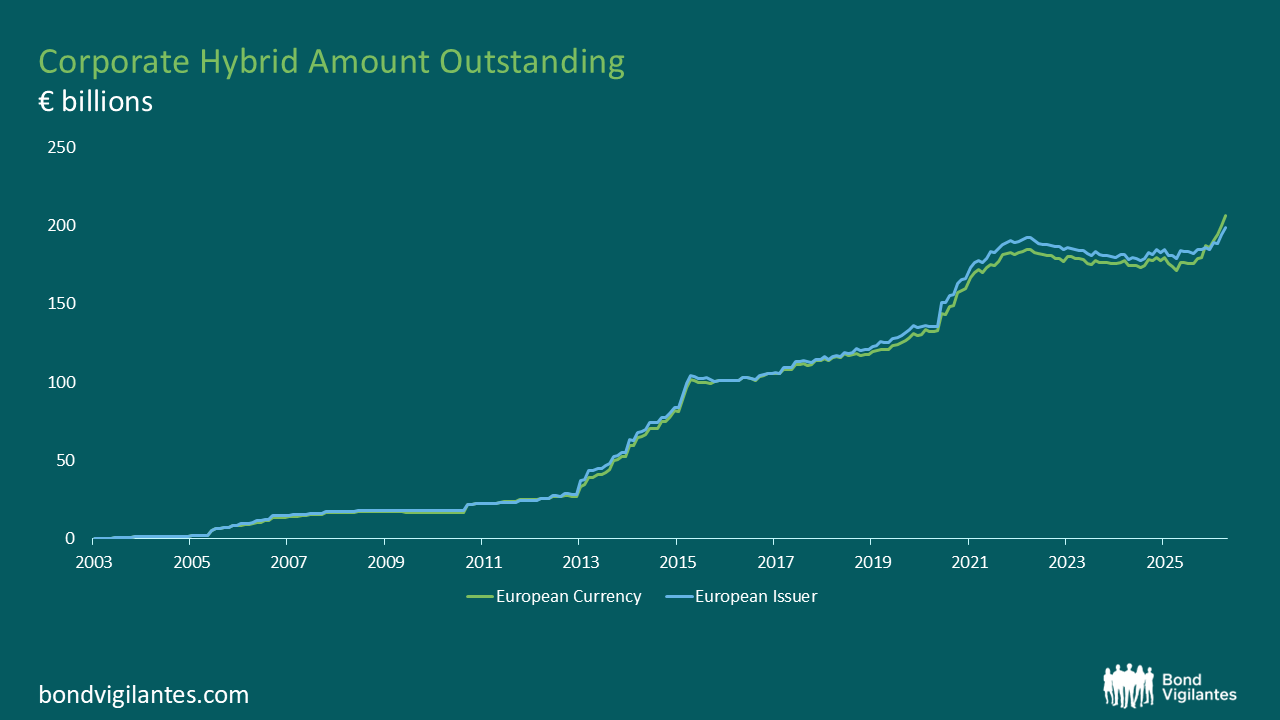

From an issuer’s perspective, hybrids have become a core balance‑sheet tool, across both Europe and the US. The outstanding stock of hybrid debt has been steadily growing for a number of years to around €200bn today. This has been helped by inaugural deals from a number of issuers such as Stellantis, Amprion and General Mills.

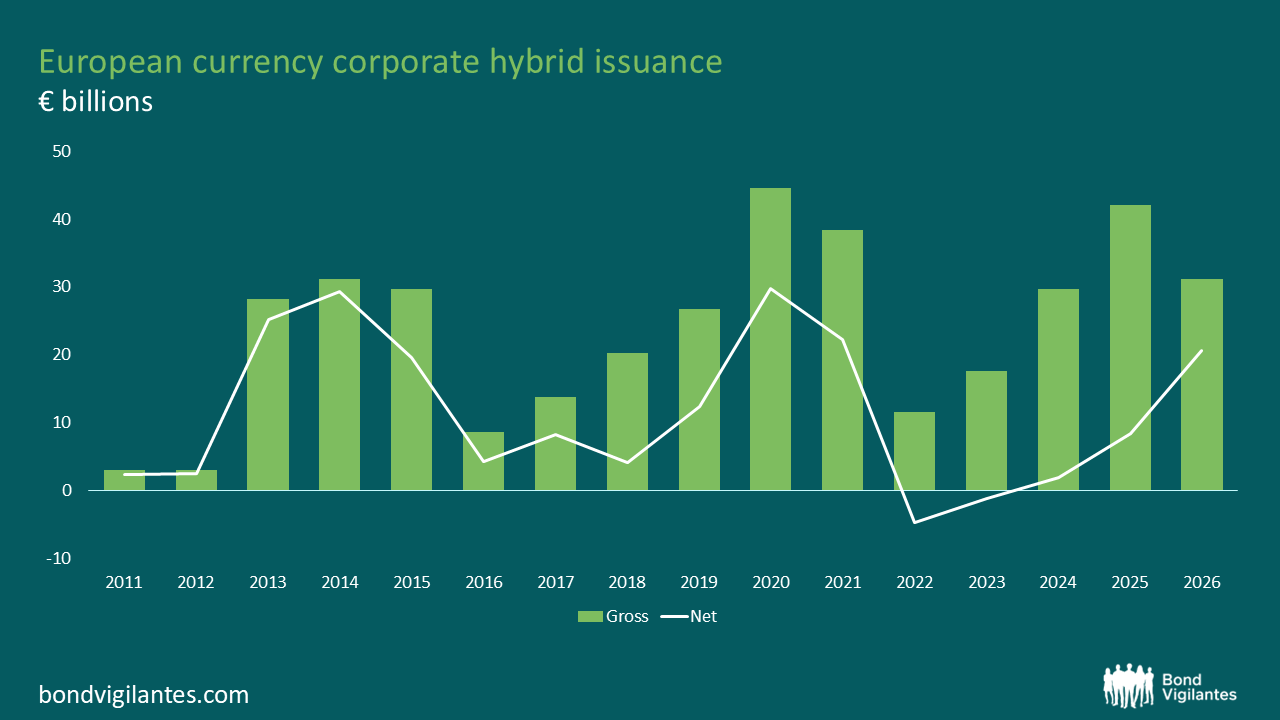

Source: J.P. Morgan, European Credit Research – Corporate Bonds, issued 28 April 2026

Source: J.P. Morgan, European Credit Research – Corporate Bonds, issued 28 April 2026

In terms of structure, hybrids with a five‑year call have proved favourable for issuers to optimise the equity content that credit rating-agencies provide to issuers (equity content is the proportion of the instrument that credit rating agencies treat as equity rather than debt when they assess an issuer’s balance sheet and credit metrics). This equity component helps issuers manage leverage ratios and can play a key part to maintaining investment‑grade ratings for large issuers such as Volkswagen or Telefonica. There are limits to the equity-content received however. S&P impose a 15% cap on the total equity capitalisation of an issuer. This is to ensure hybrids as a funding tool are used for their intended purpose – to supplement equity rather than replace it.

Are all hybrids issuers as committed as one another?

The utility and telecoms sectors are the heaviest issuers of hybrids. Today, senior–sub spreads are priced around 70-100bps apart. That is at historical tights, meaning the incentive for issuers to access hybrids as a cheap funding is high. These heavy-capex sectors have structural demand, such as the renewable build out, data-centre capacity or spectrum costs. Therefore, it is likely that issuers will keep looking to both the senior and subordinated parts of the market for funding.

Conclusion – Demand is strong. Compensation is not.

Hybrids continue to offer some investors the solutions they are looking for in a world of compressed valuations. Investors are clearly willing to fund issuer balance‑sheet optimisation on what looks like a tactical basis, comforted by strong demand and low volatility.

If sustained volatility does return, or supply remains elevated, the distinction between a tactical trade and a structural allocation will be tested quickly — and the shrinking reward for taking subordinated risk will become harder to ignore.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.