Are corporate bonds still attractive following the rally?

In the worst of the Great Depression, US BBB spreads peaked at 724 basis points (see chart). Then in Q4 last year, extreme risk aversion and a huge number of distressed sellers meant that credit markets collapsed. On December 16 2008, soon after we last produced the chart on this blog (see here), US BBB spreads peaked at a 76 year record of 804 basis points.

This year has seen a big bounce in corporate bonds. A combination of a more positive economic outlook and a tailing off of hedge fund blow-ups has resulted in the pressures on the corporate bond market easing. While US Treasuries returned -3.0% from the beginning of the year to last Friday, US BBB corporate bonds were up an astonishing +10.2%. European BBB corporates have returned +9.7%, although UK BBBs have lagged with a +1.6% return so far this year, which is due to the UK index having a much larger weighting in subordinated financials at the turn of the year.

Are credit spreads still attractive? On the face of it, yes. If you exclude four months in 1932, US BBB spreads have never been wider prior to this cycle. But wide credit spreads do not necessarily mean that the asset class is attractive. Credit spreads definitely deserve to be wide right now, reflecting both the severe recession that we are currently experiencing, and the risk that the recession may last longer or be deeper than the market currently anticipates.

Another thing to bear in mind is that these charts of nice high credit spreads that investors are probably now familiar with are painting a slightly misleading picture. This is because of the way in which yields are quoted on subordinated financials. In the chart above, UK BBB spreads are significantly wider than in the US or Europe, which is a direct consequence of financials being only 12% of the US BBB index and 13% of the European BBB index, but 23% of the UK BBB index.

To understand why yields on subordinated financials are overstated and to understand the scale of this problem, take the Barclays 6.3688% 2019 as an example. This is a sterling denominated Tier 1 Barclays bond, with a total issue size of £500m. It currently has a price of 57 pence in the pound. Its yield is quoted as 13.9%, which is assuming that the bond is called in 2019. This is a shaky assumption. Barclays may never call the bond, because Tier 1 and Upper Tier 2 bonds do not have official maturity dates – they are perpetual. If Barclays decides not to call the bond in 2019 – a decision that may make economic sense given that the bond would then turn into a floating rate bond paying 170 basis point above LIBOR – then the yield on the bond today is actually a far less impressive 8.9%. Taking prices on Bloomberg, while the yield to call implies a spread of 1030 basis points on the bond, the ‘yield to worst’ (which assumes the bond isn’t called) implies a far less attractive spread of 450 basis points.

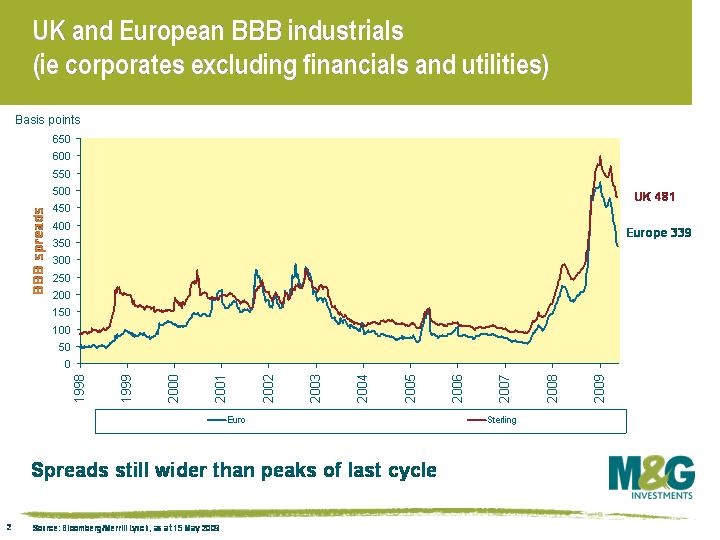

This chart is therefore a better measure of whether there is still value in corporate bonds. It focuses on European and UK Industrial BBB spreads, where an ‘industrial’ is anything that is not a financial or a utility. Industrial spreads are still wider than the peaks seen in 2002, and we do still believe that investment grade corporate bonds are overcompensating investors for the risk of default. But if BBB credit spreads were to fall to perhaps 200 basis points and we hadn’t seen further signs of improvement in the economy, then our positive view would likely change.

This chart is therefore a better measure of whether there is still value in corporate bonds. It focuses on European and UK Industrial BBB spreads, where an ‘industrial’ is anything that is not a financial or a utility. Industrial spreads are still wider than the peaks seen in 2002, and we do still believe that investment grade corporate bonds are overcompensating investors for the risk of default. But if BBB credit spreads were to fall to perhaps 200 basis points and we hadn’t seen further signs of improvement in the economy, then our positive view would likely change.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox