Back to school

It’s that time of year once again – school holidays are over and the children are going back to work. This feels very much the same in the grown up (?) world of investment. This year’s questions and tests look as though they are going to be trickier than usual. After all, the financial headmaster Ben Bernanke has just warned that conditions are unusually uncertain.

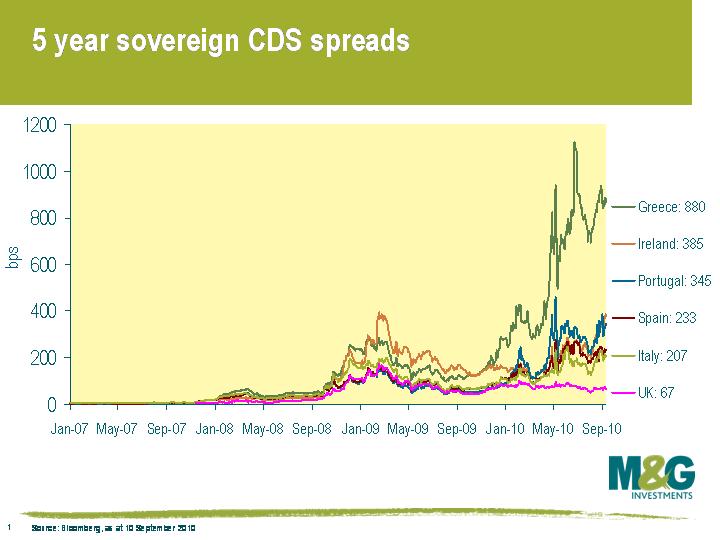

The move from the summer lull to the rigours of testing examination is no more acute than the pressure that has been reapplied to sovereign credits in Europe. The European authorities have generally responded to these challenges by a series of increasingly significant policy measures, but this chart shows they have still not solved the problem. Let’s go back to the economics class and study why their unprecedented actions have failed to soothe the markets.

When I first started studying economics as a 13 year old I didn’t have a professor Ben Bernanke. I had a “professor” Cec Thompson. He was not a real professor, but had acquired the nickname when educating himself while playing professional rugby league, where he reached the heights of playing internationally for Great Britain. Unlike Doctor Greenspan, his autobiography is a very good read. The first economic lesson I can remember that he gave was based on the price discovery and market clearing process in a simple economic example called the hog cycle. This introduced me to the concept of relative price change and market pricing, teaching us the principle of the invisible hand.

The current problems of the European periphery appear to centre on the concept of a single currency zone. By moving to a single currency 10 years ago, a simple and effective method of price discovery and market adjustments was removed from the labour and capital markets. Looking back this seems to have resulted in too much capital at too low a rate being deployed in the European tiger economies – boom and bust on a grand scale. How are we to solve this problem?

In order to make labour and capital markets efficient again, the simple option would be to reintroduce national currencies. The mechanism for doing this is non-existent, and their reintroduction and failure of the euro in this scenario is seen as worse than the current problems we face. The solution is to find a way to reintroduce national currencies, and the invisible hand, in the least damaging way possible. I have talked about this before at length, where the introduction of a new euro (the “Neuro”) would have to be done in a planned way and with a share of the shock born by savers and lenders. In the short term this would still be painful. But the long term alternative of an increasingly pressurised Eurozone, with the peripheral economies unable to adjust due to a lack of efficient market mechanisms, will turn out to be a chronic rather than a temporary problem in my opinion.

In a modern society, labour and capital should be allocated by a combination of governments and the free markets. Removing the efficient, invisible hand provided by national currencies and replacing it with political decision making as occurred with the euro was a big step. The result was political rather than economic responses to the stresses within the Eurozone, as typified by a Jean-Claude Trichet interview in today’s Financial Times, where he argues that in order to get markets to work we need to think about further strengthening the political framework.

Education is not only about doing things right, but learning from mistakes. Let’s hope that the experiment of the euro – which is just getting past its infancy – develops into a successful means of developing the economic fortunes of the Eurozone, and not a dysfunctional teenager in the years ahead.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox