Here’s why Spain’s in trouble

The convention in the market is to estimate a country’s degree of distress by looking at the yield spread over a ‘risk free’ rate. So in the case of eurozone countries, people tend to look at the spread over German government bonds.

While this spread is clearly important, it’s more relevant to look at the absolute yield level if you’re trying to figure out whether a country’s debt is sustainable. After all, if German government bonds yield 1% and the spread is 3%, the country can borrow at 4%. But if German government bonds yield 4% and the spread is 3%, then borrowing costs are 7%. That’s a whole new ball game.

The problem that the Eurozone faces right now is that not only have peripheral spreads been rising, but the risk free rate has increased too. German 10 year government bond yields have jumped from 2.1% at the end of August to 3% now, which is probably due to a combination of stronger European economic data, a sell off in US Treasuries, and the potential for a peripheral bailout to be very expensive for core Europe (Germany and France are hardly debt free, with public debt/GDP ratios likely to exceed 75% in Germany and approach 90% in France next year even in the absence of bailouts).

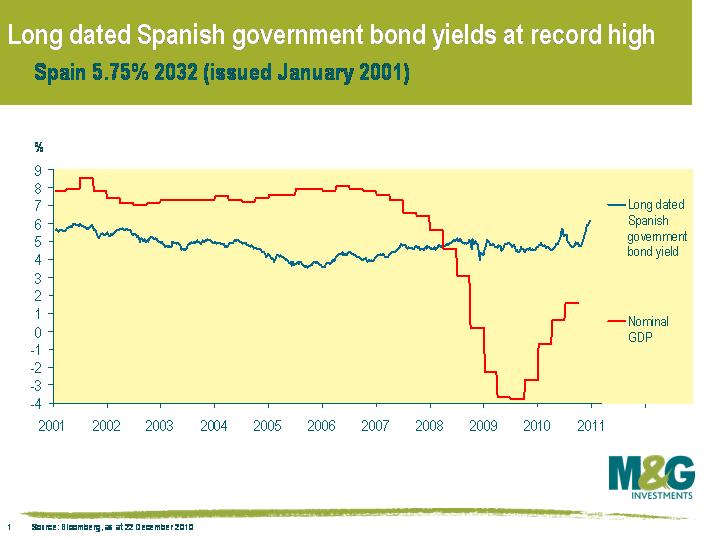

Long dated Spanish government bond yields are now at the highest for a decade, and this is a major problem if you consider the mathematics of government debt ratios. A country’s government debt/GDP ratio is a function of three things; the change in a country’s fiscal balance as a % of GDP, the difference between debt interest costs and nominal growth as a % of GDP, and changes in the stockflow adjustment (which tends to be relatively small). So assuming that a country runs a balanced budget and the stockflow adjustment is zero, if a country’s interest costs on its debt exceed its nominal GDP growth then its debt/GDP ratio will steadily creep up.

The average interest cost on all outstanding Spanish debt is currently just under 4%, which isn’t too alarming. The problem is that long dated Spanish government bonds now yield over 6%. As the chart shows, a 6% interest rate on long term debt was fine a decade ago, when nominal Spanish GDP was running at 7-8% per annum. But Spain’s interest costs will steadily climb higher as it comes to the market to borrow more money and roll over its existing debt. Any increase in interest rates from the ECB will accelerate the increase in interest costs and put even more pressure on the weaker Eurozone countries since short term borrowing costs will jump in tandem (five year Spanish government bonds already yield more than 4%). Spain needs to offset this steady rise in debt service costs with a budget surplus, which is not likely for the foreseeable future, or hope that its nominal growth rate jumps back above its borrowing costs, which is also not likely for the foreseeable future. Long term borrowing costs of 6% are not sustainable.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox