It’s not 1993-1994 in the government bond markets. Unemployment is still way too high to provoke a Fed hike. But the Bank of England might be on the brink of a policy error…

Government bonds have been selling off over the past month. Since mid October the 10 year gilt yield has risen from 2.85% to 3.63%, the 10 year bund from 2.25% to 3.00%, and the 10 year US Treasury from 2.40% to 3.40%. The damage has been even greater in peripheral Europe – Spanish 10 year yields are up by nearly 150 bps over that same period. Part of this reflects the return to a “risk on” world, where equity valuations looked compelling as the economic data came in generally stronger than expected, leading to less demand for safe haven assets – especially as those safe haven assets were trading around record low yields.

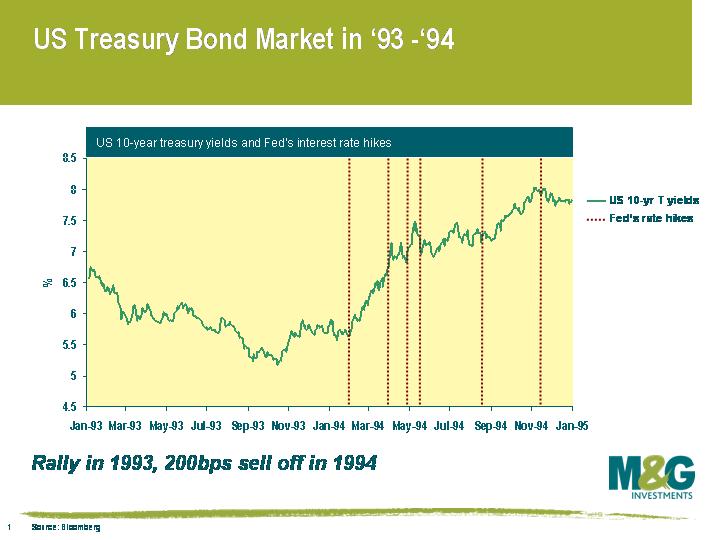

The other important part of the move is about a rise in inflation expectations. This had already started in mid 2010, as commodity price inflation (for example cotton, coffee, energy) had taken off, but the move was exacerbated by the US Fed’s announcement of QE2 in early November. 5 year inflation expectations as derived from TIPS yields have risen from a low of 1.13% at the end of August to 1.95% now. Add to this fears about sovereign creditworthiness (others have now joined us in worrying about the US’s AAA credit rating, and Europe faces its own default crisis) and it is no wonder that bond yields have risen. Might this be a re-run of 1993/1994, when government bonds rallied hard in 1993 before the Fed unexpectedly hiked rates in February 1994, provoking a 200 bps sell off in 10 year Treasury yields?

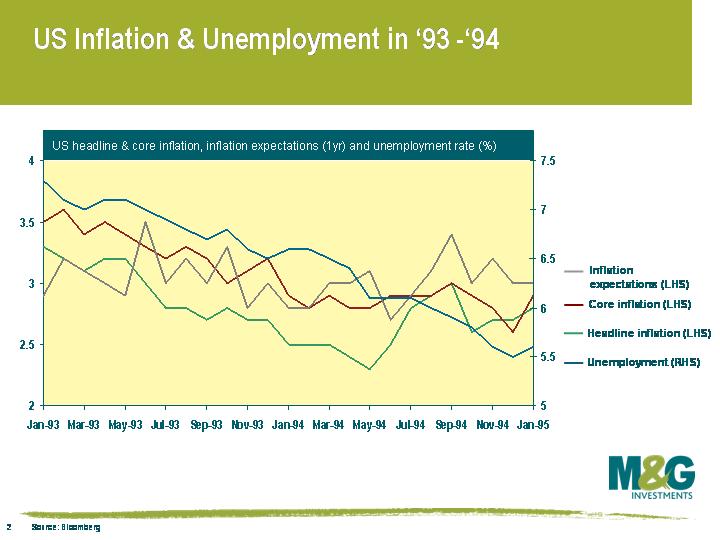

I went back to look at the economic environment at the time, to see how different it was to today. The thing that surprised me was that inflation had been steadily falling throughout 1993, both on a core and a headline measure. It didn’t start to pick up until the second quarter of 1994, after the Fed had hiked.

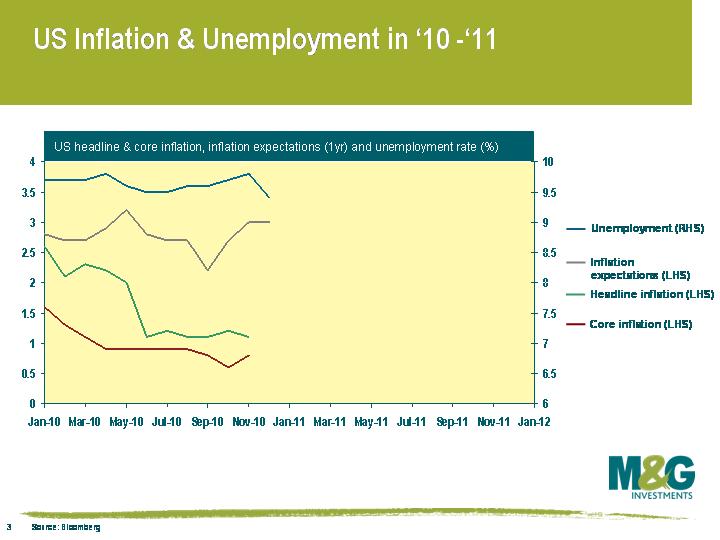

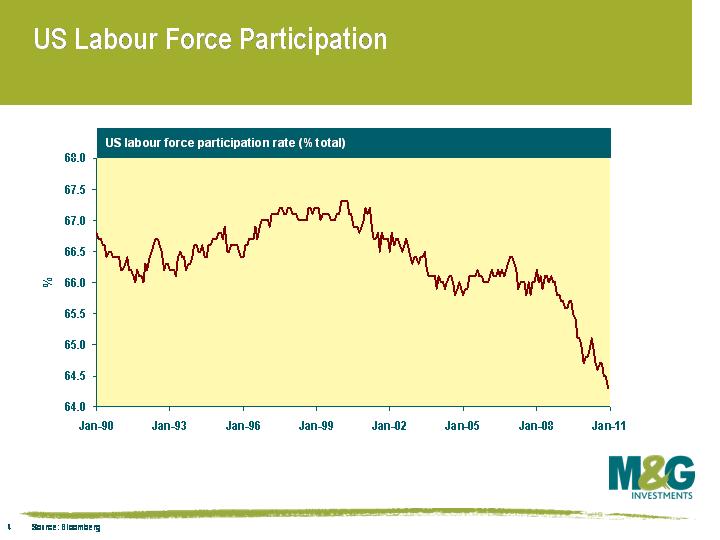

The inflation picture is similar now – the starting point is lower, but actual inflation had been coming down throughout 2010, towards record lows on the core measure. So when the Fed hiked in 1994 they were doing so in a falling inflation environment. What is different is the employment situation. In 1993 the unemployment rate was falling decisively, and was at a much lower level than it is today – i.e. the unemployment rate was falling towards 6.5%, with some estimates of full employment at just under 6%. The US currently has an unemployment rate of over 9%, and whilst it may have come off its peak, it is miles away from full employment. In fact some would argue that the unemployment rate is understated at this point thanks to a significant fall in the labour force participation rate, as discouraged workers stop looking for jobs, the young go back into education, and people retire early. Over the past couple of years the participation rate has fallen from 66% to 64.3%, compared with over 66% in `93/`94.

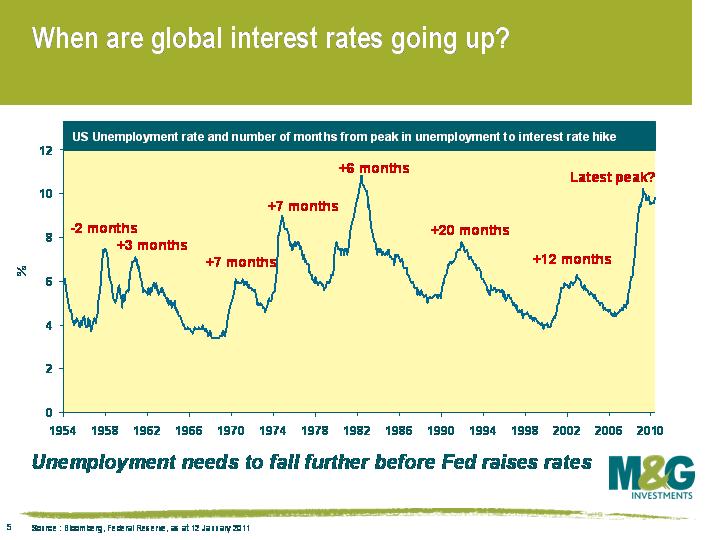

We think the Fed is still massively more worried about the jobs situation than it is about generating inflation. We’ve been following the chart on the left for years – it shows that the Fed’s reaction function means that they wait for unemployment to start falling on a sustained basis before they start to hike. In the last two cycles the lag was a year to twenty months from when the unemployment rate started to fall. You could argue that US unemployment did start to fall towards the end of Q1 last year, which means that the Fed might hike later this year. But in our view the level of unemployment is still way too high, and the fall in the participation rate is too severe. In any case, in the US you can rule out an early 2011 rate hike.

Is that also true in the UK? Unemployment here is sticky too, just below 8% on the ILO measure. And the public sector job cuts are yet to bite. But inflation is very sticky here and the Bank of England has missed its 2% CPI target and been at or above 3% for all of 2010. RPI inflation is at 4.7%! The 2.5% VAT hike will start feeding into retail prices from this month onwards, and utility and petrol prices are rising sharply. The money markets are already pricing in two 0.25% rate hikes in the UK this year, with a small chance that there will be a third rate hike by year end.

Rate hikes would kill core inflation (although remember that mortgage rates are a component of RPI, so that measure of inflation would likely rise with every rate hike) – but they would also be GDP-suicide in this fragile economy, bringing deflation risks back into play. Hopefully the Bank still feels it can target future inflation, and has the confidence to ignore those reacting to current inflation newsflow and calling for imminent rate hikes. But I don’t think that the Bank of England has much breathing room left, and with persistently high current inflation the Bank’s credibility is under attack. I think we’re only one surprisingly robust inflation print away from a UK rate hike. Let the policy errors begin…

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox