Why the UK has a real rate problem

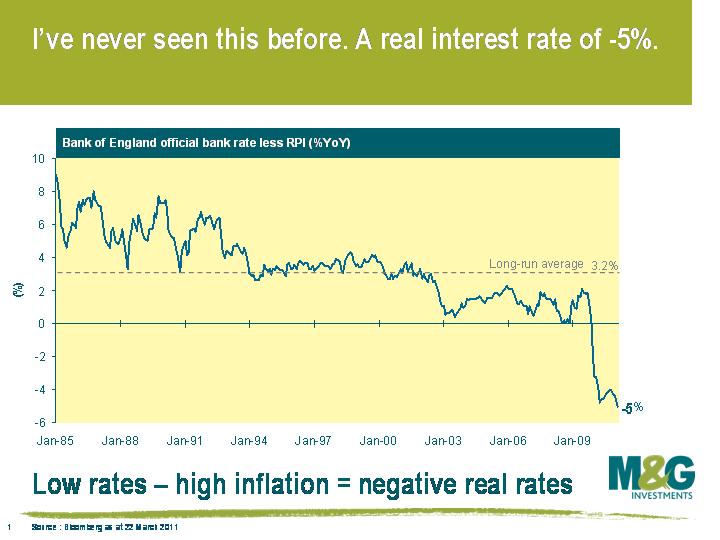

The financial crisis is resulting in the authorities, the public, and investment managers seeing things they did not expect to see. Today’s headline RPI level of 5.5% is a record 5% above the Bank of England base rate of 0.5%, resulting in a negative real interest rate (base rate – RPI) of -5%. This is the most divergent I’ve seen this in my 25 years in the city (see chart).

The bond bears think that the relationship will be normalised by a rapid increase in the base rate and a fall in inflation towards more normal levels. The bulls would suggest that the inflation measure reflects temporary factors and will therefore decline to more normal levels with only modest rate increases by the Bank of England.

However, the fate of the base rate and inflation does not sit with the bond bulls and bears but with the Bank of England Monetary Policy Committee (MPC). Their policy of ultra low rates means the MPC is missing their CPI based inflation target of 2% on a regular monthly basis. Since September 2007, inflation has been above 2% in 35 out of 42 months.

Why are they doing this? Presumably the MPC believes that the high inflation rate will be temporary in nature, however there could be other motives behind their policy stance. The Bank of England via QE has previously determined that interest rates had reached their effective bounds in stimulating the economy, as a central bank cannot achieve negative nominal rates. Therefore in order for their rate setting policy to work they have become very relaxed with negative real short term interest rates as they pursue a policy of cleansing the system of its financial hangover from the credit bubble as best it can.

Lets hope from the Bank of England’s point of view that the hair of the dog cure of ultra low real rates is actually an appropriate diagnosis of a fragile, staggering UK economy. Otherwise we could all end up in a dizzy inflation spiral.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox