Why the US Dollar now looks cheap against, well, basically everything

Back in January I wrote about why we loved the US dollar and worry about EM currencies, and did an update on EM in June (see EM debt funds hit by record daily outflow – is this a tremor, or is this ‘The Big One’?). Another EM piece will follow soon (the short version is that while it was ‘just’ a tremor, I’m increasingly worried that ‘The Big One’ is coming).

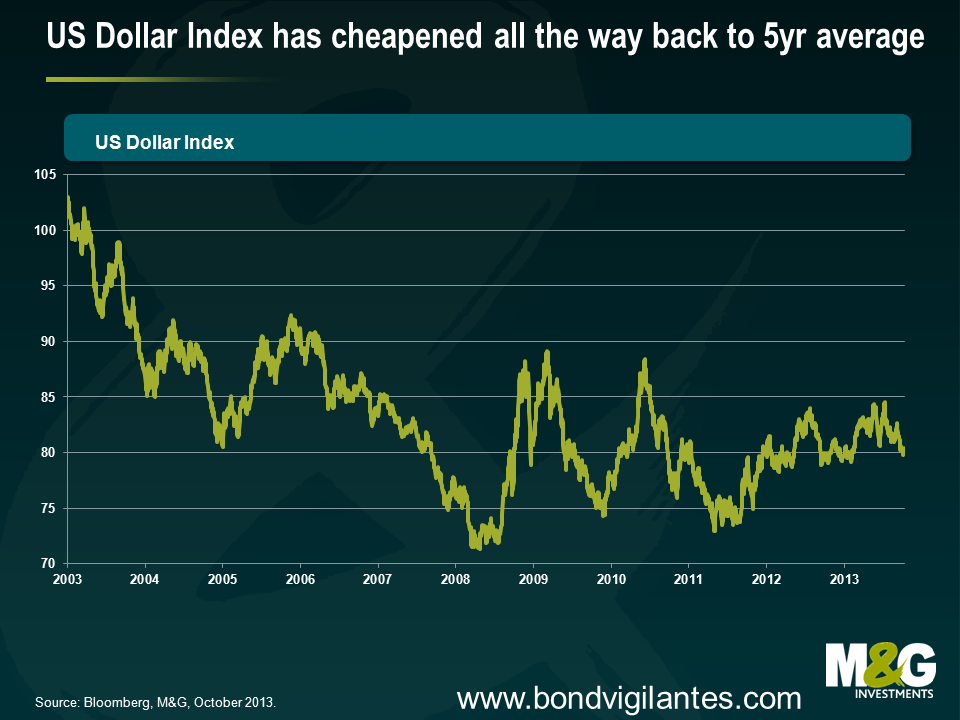

The US Dollar was strong through Q1 and Q2, but an interesting development in Q3 was that while the US Dollar held up OK against most EM currencies, it performed abysmally against other developed currencies. Below is a chart of the US Dollar Index, a gauge of US Dollar performance against a basket of major world currencies, where the basket contains EUR (57.6%) JPY( 13.6%) GBP (11.9%) CAD (9.1%) SEK (4.2%) CHF (3.6%). The Dollar Index is back to where it was at the beginning of the year, and despite the relative strength of the US economy versus other developed countries, the Dollar Index has now returned to the average level of the last five years.

The reasons that led us (and an increasing number of others) to be so excited about the US dollar over the past 18 months were namely compelling USD valuations following a decade long slump, an improving current account balance, the rapid move towards energy independence, and a strengthening US economic recovery where a surging housing market and a steadily falling unemployment rate made it likely that the US would lead most of the world in the monetary policy tightening cycle.

The long term positives for the US dollar are still there, but have recently been overshadowed by negative ones. So what has changed? Recent US Dollar weakness is probably to do with the Fed’s non-tapering in September, the ongoing budget nonsense, and a very big unwind in a whole heap of long USD positions.

It makes sense to be more bullish on the US dollar because these negative forces appear to be dissipating.

Firstly the non-tapering event. Treasury yields and the US dollar had already started to drop ahead of the non-tapering decision thanks to a slight weakening in US data, with US 10 year yields dropping from 3% on September 5th to 2.9% on September 18th and the Dollar Index falling 2%. Nevertheless markets were still taken by surprise, and Treasury yields and the US Dollar had another leg lower with US 10 year yields briefly dropping below 2.6% at the end of September, and the Dollar Index falling almost another 2%.

But then on Wednesday we had September’s FOMC minutes, which were surprisingly hawkish. The decision not to taper was a close call, where most members still viewed it as appropriate for tapering to start this year and for asset purchases to be finished by the middle of next year. Yes, the US government shutdown that has occurred since the meeting took place appears to be already starting to hit US economic data (estimates vary enormously for the total hit to Q4 US GDP), and the weaker data is therefore likely to push the start date for tapering back a little. But if you assume that the US government shutdown is a one off event (admittedly not a particularly safe assumption), then the shutdown should merely slightly delay the tapering decision and the normalisation of US monetary policy, it should not result in a permanent postponement.

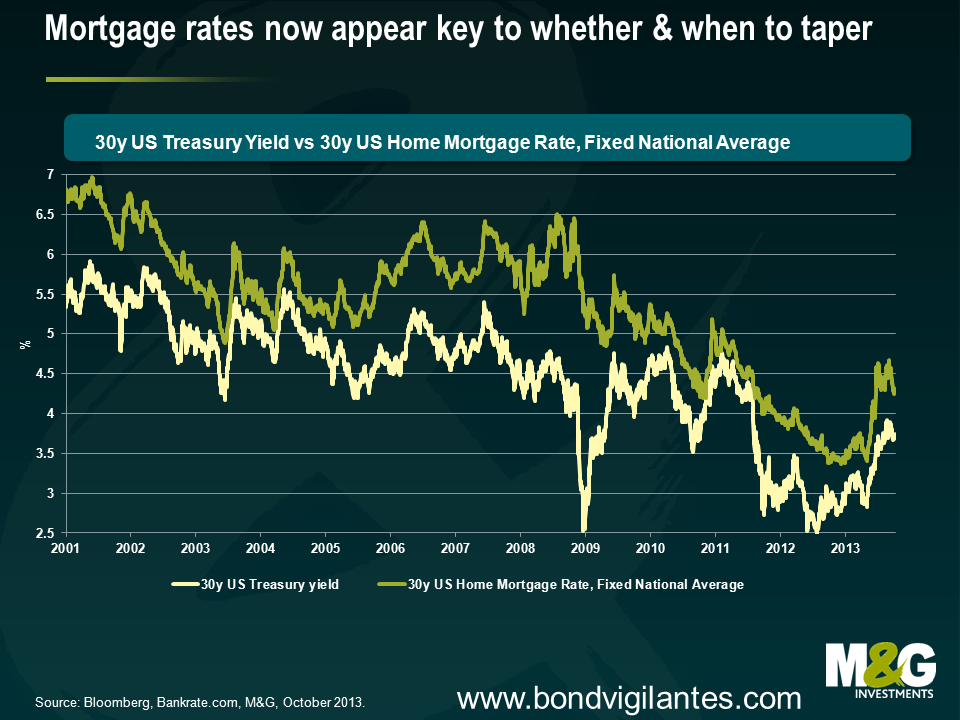

That said, something that was a little disconcerting from the minutes of the September FOMC meeting was that the jump in mortgage rates played a key role in the decision not to start tapering, with some members worrying that a reduction in asset purchases “might trigger an additional unwarranted tightening of financial conditions”. HSBC’s Kevin Logan makes the good point that higher mortgage rates present Fed policy makers with a dilemma; if rates rise because the markets expect a tapering of QE, and that in turn stops the Fed from tapering, then it makes any QE exit pretty tricky and it appears that the Fed now has an additional criterion for reducing QE – not only must the economy and labour market be doing better, but long-term interest rates cannot rise too much in advance, or even during, the tapering process. If the Fed’s decision not to taper was heavily influenced by higher mortgage rates, though, then their fears should now be allayed given the chart below. This chart, together with the effect that mortgage rates have on the US housing market, has clearly taken on added importance.

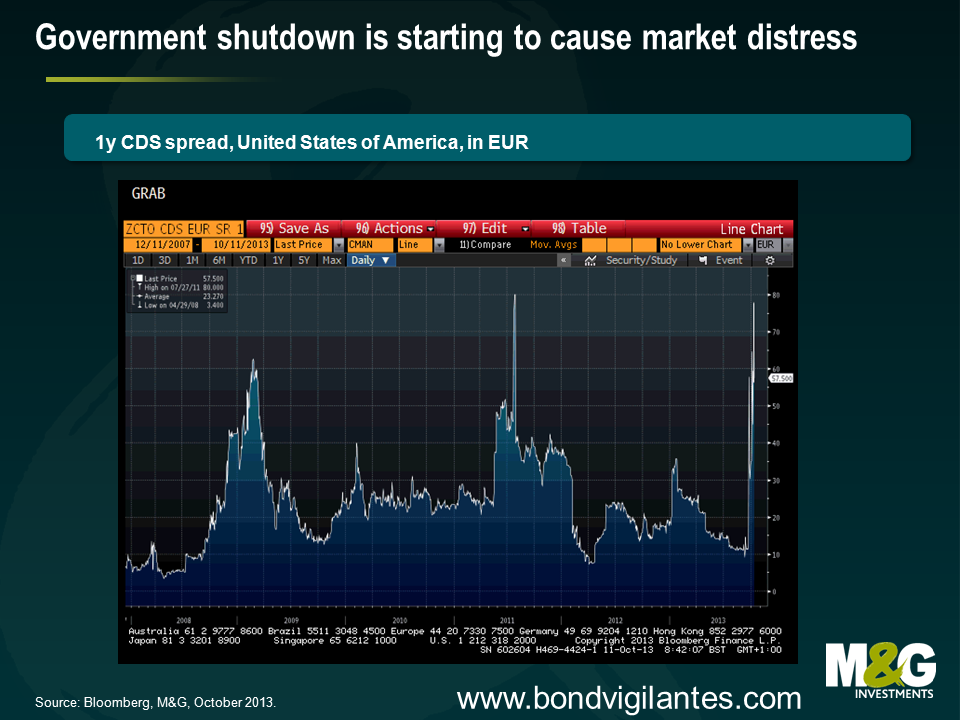

What about the ongoing budget nonsense? This one takes a bit of a leap of faith, but markets are clearly starting to price in the risk of something going very badly wrong as demonstrated by the jump in T-bill yields and the surge in 1yr US CDS (i.e. the cost of insuring against a US default, see chart below). But market stresses should make the prospect of a deal more likely, and this appears to be starting to happen. It’s dangerous reading too much into the headline tennis, but the latest news is that Republican and Democratic leaders are open to a short term increase in the debt limit. And don’t forget, the debt ceiling has been raised 74 times since March 1962 – past performance is no guide to the future as everyone knows, but while this episode is particularly chaotic, is this time really different?

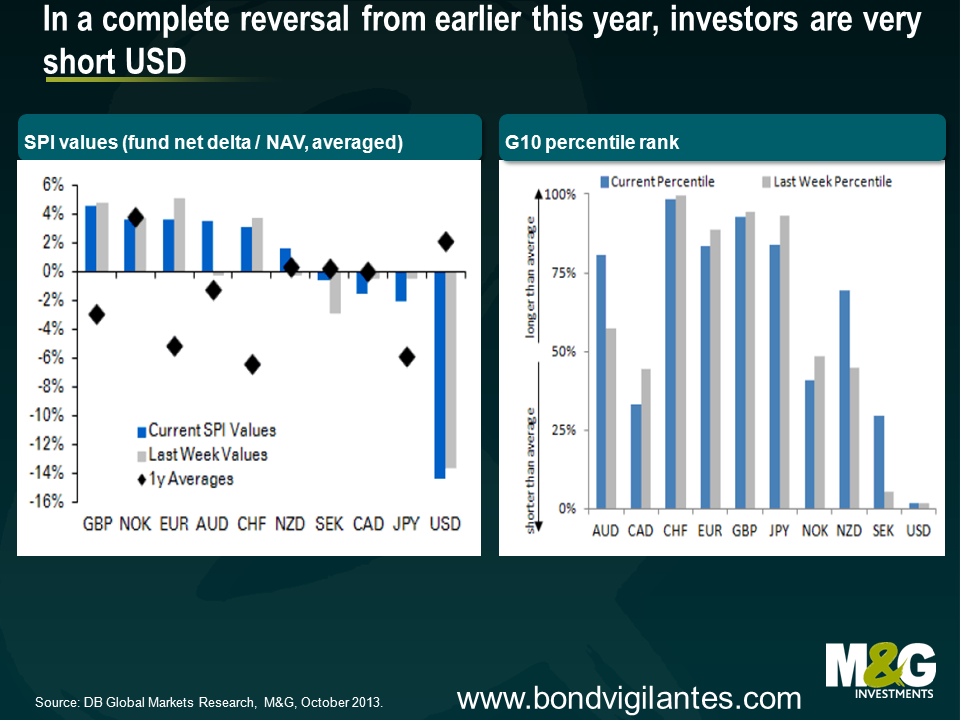

Finally, the technicals for the US Dollar are now much more appealing. US Dollar positioning has seen a sharp reversal from earlier this year, and Deutsche Bank estimates the US dollar is the only substantial short in the market (see charts below). Does this matter? To finish with a quote from John Maynard Keynes* regarding investing, “It is the one sphere of life and activity where victory, security and success is always to the minority and never to the majority. When you find any one agreeing with you, change your mind. When I can persuade the Board of my Insurance Company to buy a share, that, I am learning from experience, is the right moment for selling it”‘.

*Keynes is famous for amassing a fortune through investing, but in 1920 he had to be bailed out by his father together with an emergency loan from Sir Ernest Cassel, and he came very close to being wiped out in the 1929 and 1937 stock market crashes. So clearly the consensus can occasionally be right.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox