Europe’s debt/GDP levels are worse today than during the Euro crisis. So why are bond yields falling?

Two and a half years ago, there was a real fear in the marketplace that the euro would not survive. It appeared unlikely that Greece would be able to remain in the Eurozone and that some of the larger distressed economies like Italy and Spain may follow them out. High levels of government debt, unemployment and a banking system creaking under all this pressure did not bode well for the future. The mere possibility of a Eurozone nation leaving triggered massive volatility in asset markets from government bonds to equities, as investors grappled with the consequences of such an event occurring.

Of course, the bearish forecast for Europe did not eventuate. Perceptions had shifted significantly from the darkest days of the euro crisis. Politicians and central bankers have shown significant determination in keeping the euro intact, despite often only acting at the darkest hour. In markets, confidence returned after ECB President Mario Draghi’s now famous “whatever it takes” comment and it had a real effect on government bond yields with spreads over German bunds collapsing across the Eurozone.

Unfortunately for European government bond investors, the Eurozone could re-emerge as a source of risk. The reason is, since 2011 European government and economic fundamentals have generally gotten worse and not better.

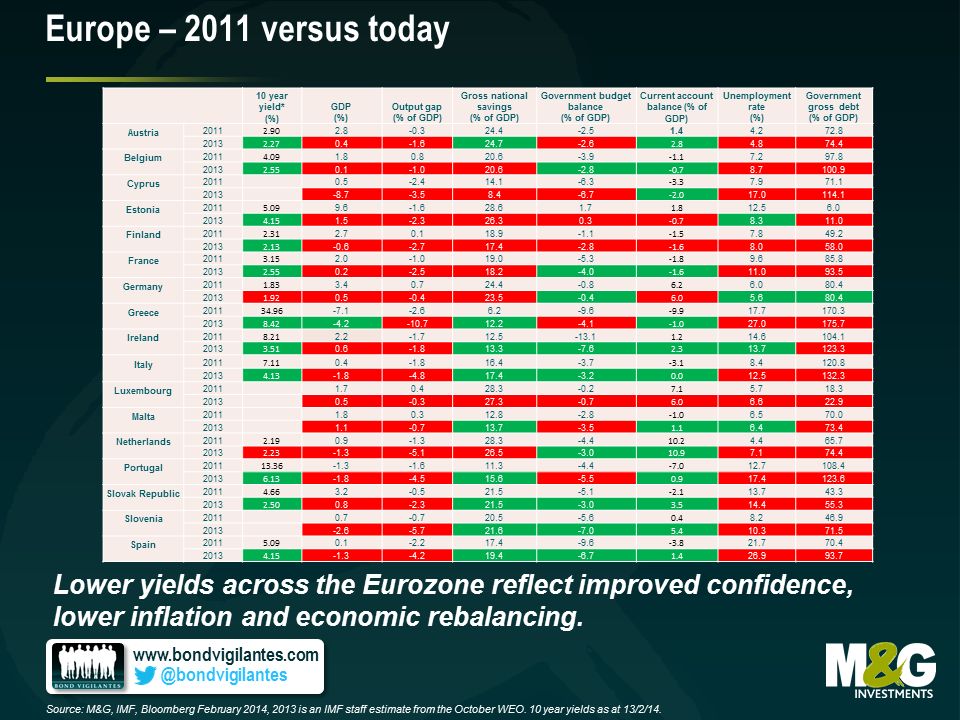

When we look at the above table – which measure fundamental indicators like total investment, the unemployment rate and gross levels of government debt to GDP from 2011 and compares it to now – we can see a lot more red (which indicates a deterioration) than green (which indicates an improvement). Yet what is striking is that apart from Germany and the Netherlands who have seen their 10 year government bond yields increase slightly, all other European nations have seen their yields fall. This is not what we would expect to see given that various metrics like GDP, the unemployment rate, output gap and government debt to GDP are actually worse now than they were at the height of the Eurozone crisis.

I can see three main reasons why yields have fallen across the Eurozone despite a worsening in the economic statistics. The first is that confidence has returned and the credit risk premium demanded by bond investors has fallen. Investors in European bonds now believe that default risk has fallen from the dark days of 2011, despite a general worsening in conditions which would imply higher – and not lower – default risk. When Draghi said the ECB would do “whatever it takes”, the market believed him.

Secondly, the inflation risk premium that investors demand has collapsed as Eurozone inflation has collapsed. Low inflation in the Eurozone is largely the result of painful internal devaluation, high unemployment and government austerity. Countries like Ireland, Portugal and Greece are feeling this the most, having experienced deflation over the last couple of years. As we can see in the table, austerity has meant that budget deficits have improved across the Eurozone, but this has also resulted in deflationary forces becoming more pronounced. Lower European inflation means higher real yields, and this has contributed to nominal yields falling or remaining low in Eurozone government bonds. However, the danger for the periphery is that lower inflation implies lower nominal growth rates, and this means even greater pressure on the Eurozone periphery’s huge debt burdens. Markets should react to lower nominal growth rates by questioning these counties’ solvency, pushing bond yields higher.

Thirdly, the other main reason that peripheral yields have converged is that there are genuine signs of rebalancing, as indicated by improving current account balances and falling unit labour costs. The majority of Eurozone nations are now running a current account surplus, including Spain, Portugal, and Ireland. Despite being locked into the single exchange rate which is arguably way too high for these countries, global competitiveness has improved and exports have increased.

There are good reasons the euro will survive. However, it is important to question whether the market is charging a high enough credit risk premium given the challenges that continue to face the Eurozone. Increasingly, bond investors need to assess the risks of deflation in Europe as well. Arguably a lot of good news is priced in to government bond markets at the moment, and we remain hesitant to lend to those European countries displaying weaker financial metrics at this point in the cycle. With the IMF recently finding “no evidence of any particular debt threshold above which medium-term growth prospects are dramatically compromised”, it suggests that there are many more important things to bond investors than the public debt/GDP ratio (like credit growth, labour markets and inflation). Public debt/GDP ratios are what investors have been fixated on since the financial crisis, but they are a lazy and incomplete way of assessing the risks in government bond markets.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox