“Global greying” could mean getting used to ultra-low bond yields

The developed world is going through an unprecedented demographic change – “global greying”. This change is having a massive impact on asset prices and resources as populations around the world get older and live longer. It is also having an impact on the effectiveness of monetary policy. We would typically expect older populations to be less sensitive to interest rate changes as they are largely creditors. Younger populations will generally accumulate debt as they set themselves up in life and are therefore more interest rate sensitive. The impact of demographics implies that to generate the same impact on growth and inflation, interest rate changes will need to become larger in older societies relative to younger societies.

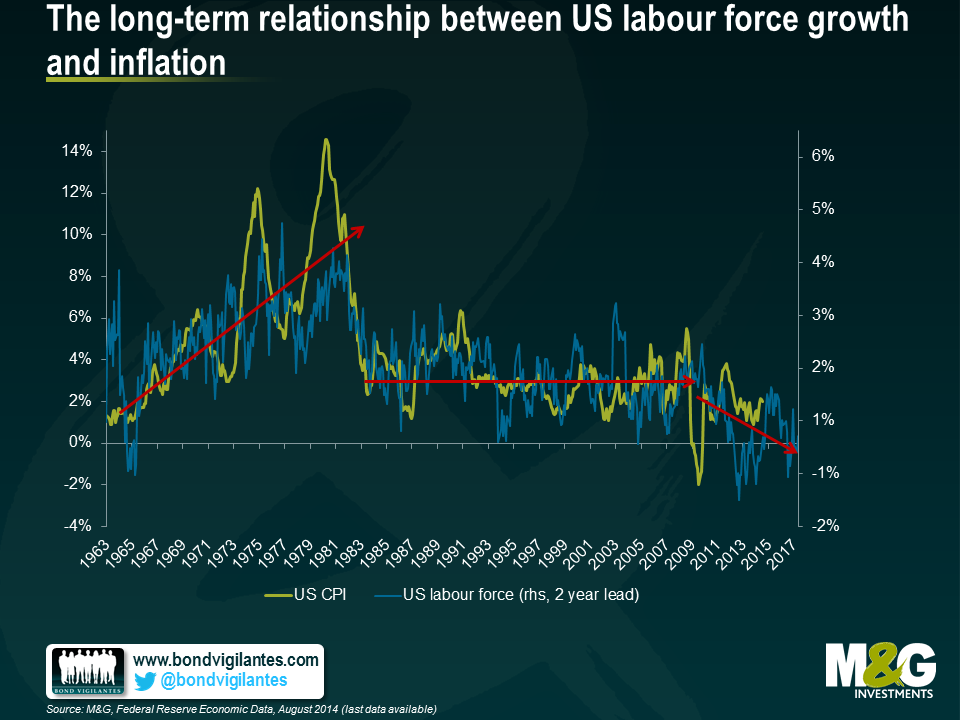

Turning to the impact of demographics on inflation, labour force growth may provide some insight into the potential path of future inflation or at least give us some guide as to the long-term structural impact of an aging population on inflation dynamics. The theory is that a large, young generation is less productive than a smaller, older generation. As the large, young generation enters into the economy after leaving school/university the fall in productivity causes costs to rise and therefore inflation increases. Additionally, the younger generation is consumption and debt hungry as they start a family and buy homes. Eventually, the investment in the younger generation comes good and there is a large increase in productivity due to technological change and innovation. As consumers become savers, inflationary pressures in the economy start to subside.

The long-term interplay between US labour force growth and inflation is shown below. Inflation lags labour force growth by around two years as it takes some time for the economy to begin to benefit from productivity gains. As US labour force growth rises and falls over time, inflation generally follows a similar trend.

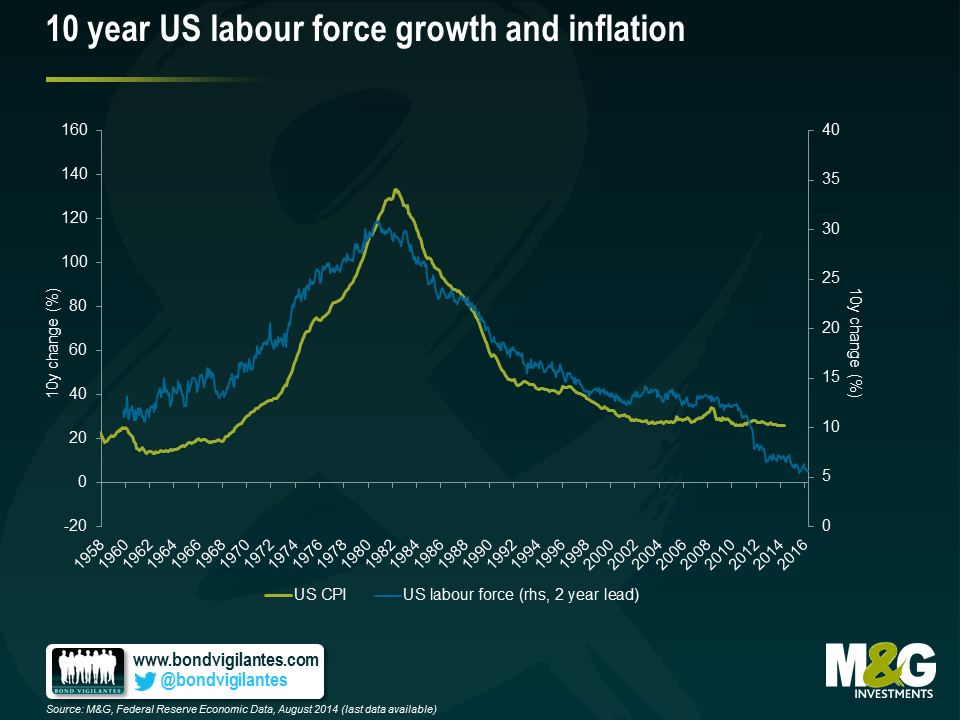

The second chart looks at the same economic indicators, this time looking at 10 year growth in the labour force against inflation. Interestingly, this chart seems to show that the baby boomers entered into the workforce around the same time as the global economy experienced a supply-side oil price shock. The influx of new workers into the US economy is likely to have contributed to the great inflation of the 1970s. For the next thirty years or so, inflation fell as the economy enjoyed the technological advantages and productivity gains generated by the baby boomers. Looking forward, it appears that long-term deteriorating labour force growth may contribute to deflationary pressures within the US economy.

I am not saying that demographics are the only reason that inflation has fallen in recent years. The massive accumulation of private and public sector debt, globalisation and technological change are also secular trends worth monitoring. Rather I believe “global greying” and the impact of demographics on inflation and the real economy is an additional secular trend worth monitoring. Can central banks do anything in the face of this great generational shift should deflation become a reality? Interest rates are at record lows, quantitative easing has been implemented and we are yet to see the large impact on inflation that many economists expected.

Lower interest rates and the yield-dampening forces that exist in the global economy is a topic I previously covered here. In terms of bond markets, deflationary pressures are a “yield-dampener” and another reason why bond yields could remain low for some time and fall further from current levels over the longer-term.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox