Mini Bonds – who is buying them?

One of the many unintended consequences of structurally low interest rates over the past few years has been the emergence of mini-bonds in the UK. These are typically non-tradable debt instruments issued by companies directly to individual investors*. We’ve commented before on one such bond issued by Chilango, a London based vendor of Mexican food, and highlighted some of the risks relative to the more established institutional bond market (very limited disclosure, an absence of legal covenants, lack of call option protection and no secondary market liquidity).

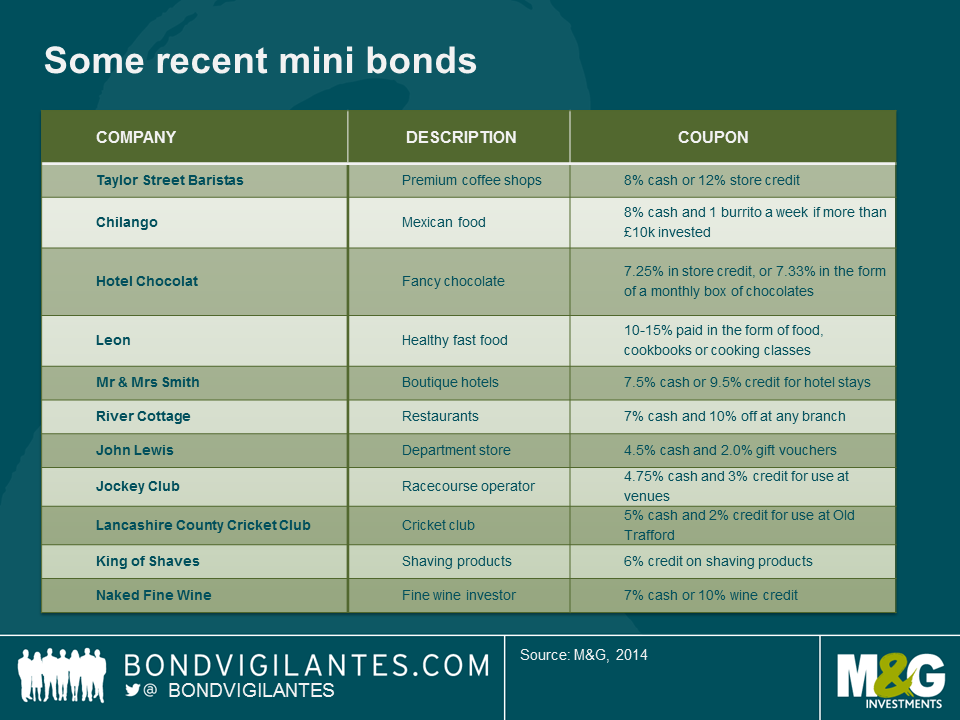

Nonetheless, these instruments are proving to be popular, not least given the interest rates on offer, but also due to some of the more exotic features such as coupons in the form of goods and services. Indeed, the latest addition to the pack is Taylor Street Baristas, who are offering a bond with the choice of an 8% cash coupon or 12% store credit.

The question always intrigues us – who are buying these bonds? Looking at some of the mini bonds issued over the past 3 years and some of the non-cash coupons on offer, we can build up an interesting profile of the quintessential “mini bond” investor.

When we consider the above, this is the profile that starts to emerge:

Location – London – the food selection on offer (Taylor St Baristas, Chilango and Leon) is only of any practical use to someone who lives and works in London and can access the relevant branches on a regular basis. Until such time as these chains expand outside the capital, our quintessential mini bond buyer is almost certainly a Londoner.

Holidays – South West – the combination of the River Cottage discount (with branches mainly in the West Country) and the Mr & Mrs Smith credit means our mini bond buyer is well incentivised to spend any down-time in a boutique hotel in the South West of England.

Diet – Poor – Whilst the River Cottage and Leon may offer food at the healthier end of the spectrum, the weekly burrito, fine coffee, lots of chocolate and a steady supply of wine suggests an indulgent lifestyle.

Hobbies – Cricket / Horseracing – The numerous Jockey Club venues offer up a range of opportunities for a day at the races peppered with the odd trip up to Old Trafford.

Without going as far as saying that mini bonds are targeted at obese London based oenophiles who occasionally venture out to Newmarket, there is a more serious point to be made when we look beyond the gimmicky features of this market.

A new source of finance for businesses at a time when bank lending conditions are difficult is something to be welcomed. What we would not want, however, is this to come at the expense of investor protections for bondholders. These protections have evolved over several decades in the institutional bond market and serve an important function in protecting investor rights and indeed their capital. These protections really matter when things go wrong and we are yet to see any default in this particular market so this deficiency is yet to manifest itself.

With this in mind this is what we would like to see in any future mini-bond :

- Call option protection – if an issuer wants to redeem a bond earlier than the stated maturity (the so called issuer call option), the investor should receive a premium to the face value of the bond to offset the loss of potential coupon.

- Adequate financial disclosure – Historical audited accounts including full balance sheet, cash flow statement and profit and loss must be disclosed and a commitment made to update investors with new accounts on a timely basis.

- Explicit security and/or collateral over the assets of the business – in the event of a default, the ranking of the bond in the capital structure should be made explicit with reference to any assets on the balance sheet.

- Equity participation/return – in the absence of any security or collateral, if an issuer wishes to raise finance for an aggressive expansion, it is only fair that an investor who risks their capital shares in the upside either through a high coupon or an element of equity participation.

- Restrictions on payments and leverage – the ability for the company to strip cash out in the form of dividends at the expense of bondholders should be explicitly limited as well as the ability to raise additional amounts of debt that pose a risk to existing creditors.

- Transferability – the option to buy or sell a bond to a 3rd party before maturity would greatly enhance an investor’s ability to manage their risk and their exposure.

With these additional features in place, mini-bond holders would begin to share some of the beneficial features of the institutional market whilst at the same time allowing them to enjoy the more exotic coupons on offer. Otherwise, even with the extra wine and burritos, mini bond investors are getting a raw deal compared to the more established corporate bond markets.

*NB – this is in parallel to the development of the more regulated retail bond market that has emerged in the UK, Italy and Germany where issuers are subject to more stringent oversight and the bonds themselves are listed on an exchange and are transferable.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox