The Middle-East – an expensive safe haven for bond investors

I am just back from a fascinating investor trip to the Middle-East, where I spent a week meeting with corporate and government bond issuers as well as market participants in the United Arab Emirates (UAE). We spoke at length about Islamic finance, the oil price impact and geopolitical risk.

When I asked the question of the oil price impact on the region to corporate issuers and government officials the response was “there is no impact”. In contrast, most unbiased investors and bankers living in the UAE acknowledge that the new oil price context (down 60% in the past 6 months) will result in the Gulf Cooperation Council’s (GCC) growth rates moderating in 2015 and 2016, following a strong 2014.

The impact of lower oil prices on countries within the GCC is not uniform. Saudi Arabia will be challenged most as the economy has little buffer due to social spending needs (the government need to deliver 2 million jobs to Saudi nationals by 2025). This is a contributing factor to my view that Saudi Arabia should cut oil supply by the end of the year. Tourist destinations such as Dubai, and to a lesser extent Abu Dhabi, will be less affected should oil prices remain at current levels. However, the indirect impact will nevertheless be negative. There are a number of reasons for this view:

- The residential real estate sector in Dubai has already begun to slow down and a number of units’ prices are down by between 15% to 20%, although it is hard to tell given the shrinking number of transactions year-to-date. On the other hand, commercial real estate has held up well and is expected to continue to be resilient going forward.

- The trade sector in the UAE, a major driver of GDP for the Emirates, decelerated in the first two months of the year and is likely to record mid-single digit growth in 2015 (2014: +9%), according to one large Emerging Market bank with a significant footprint in the region.

- With a lower amount of Russian tourists (due to the Rouble depreciation) and likely lower number of GCC tourists this year (directly affected by lower oil prices), tourism should experience a short-term downfall. However, I believe this will be more than offset in the medium run by the increasing share of Asian tourists, in particular Indian and Chinese nationals that are benefiting from lower oil prices. The tourism sector still has very strong fundamentals in the UAE and, in my view, will be a key driver of resilience this year and after.

- The weakening macroeconomic environment is expected to weigh on the UAE banking sector with a slowdown in credit and deposit growth to the mid-single digits. While banks are in much better shape than in 2009 and should not face any major liquidity issues in the next 12 months, they are nonetheless very dependent on government deposits and are likely to face an increase in non-performing loans (NPLs) and a deterioration of asset quality (real estate being a large exposure).

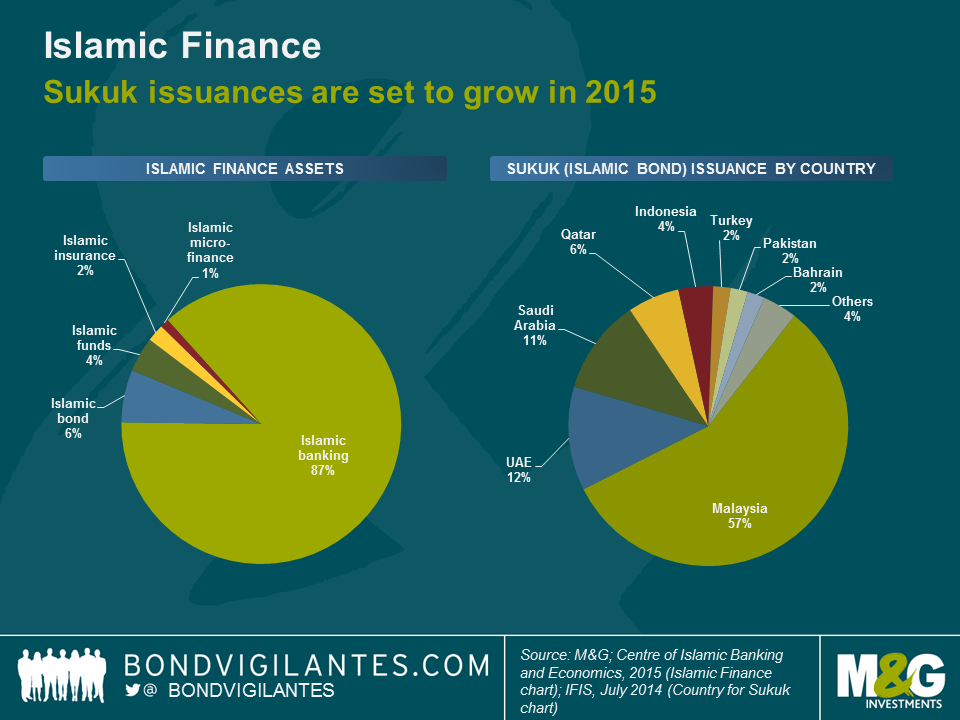

Moving on, Islamic finance has grown at a fast pace (average +20%) since the 2008 global financial crisis and was estimated to be worth USD2.1 trillion of assets in 2014 by the Centre of Islamic Banking and Economics (CIBE). In 2015, the Dubai-based CIBE has estimated that global Islamic financial assets will reach USD2.5 trillion, of which an expected USD150 billion will be sukuk (Islamic bonds) issuance.

Muslim countries obviously dominate the sukuk market – as per the chart below – and Islamic finance is not expected to be a major game-changer in the near future of global financial markets. However, investors have recently seen increasing supply from Western (non-Muslim) countries. Last year, the UK issued its first ever £200 million sukuk bond which has been trading well in the secondary market. On top of this, three banks (Societe Generale, Bank of Tokyo-Mitsubishi and Goldman Sachs) set up sukuk programmes in 2014 which, if successful, will improve liquidity in the global sukuk market.

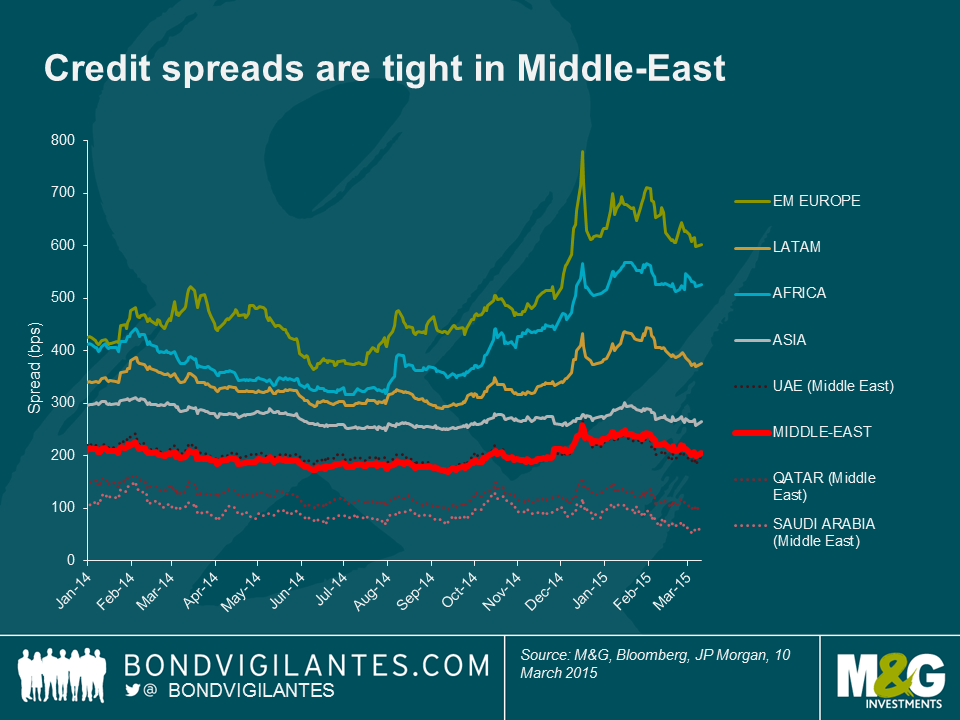

Turning to valuations, from an emerging market perspective, credit spreads have been tight for a long time in the Middle-East due to two major reasons: (i) historical excess cash from oil revenues that fuelled the GCC economies and ultimately supported the corporate bond market, and (ii) political stability in the UAE which account for most of the bond market in the Middle-East.

First, I believe current spreads are not pricing in the new oil price context and the above mentioned negative impact it will have on the real economy of the GCC countries. As a result, relative value looks expensive and some of the most vulnerable bonds could widen significantly by the end of 2015. In addition, I believe that bond investors have been underestimating the increasing geopolitical risk in the region, evidenced by the UAE’s direct military involvement in the Arab coalition against the Islamic State (IS) militant positions in Syria. While the IS is by all means more a direct threat to Syria, Iraq, Libya, Egypt and even Jordan than the UAE, the Arab allies’ involvement in the conflict is to me a risk of spreading the conflict in these countries.

That said, it appears that a large correction across the board is unlikely as the region remains a relative safe haven compared to other EM regions that have their own problems: Russia geopolitics in EM Europe, Brazil weaknesses in Latin America, and China slowdown in Asia. In terms of sectors, bonds issued by banks may weaken due to the soft economic outlook and the residential property sector – particularly privately-held issuers – could come under selling pressure. The commercial real estate sector could prove resilient for investors, as could any corporates benefitting from strong government support. Bond technicals will also be key in the region and a strong local and sticky investor base could provide some protection against more volatile times ahead.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox