The Bond Market is Looking Through Present Inflation Numbers

CPI in the UK today fell into negative territory for the first time, posting a 0.1% decline year-over-year. Airfares presented a meaningful drag on the April figures, owing to the timing of Easter compared to last year. Carriers increase their prices over Easter holidays, so when Easter moves between months this causes flight prices to move around, thereby affecting the headline inflation numbers. However, petrol prices were up slightly on the month which slightly offset some of this effect of flights.

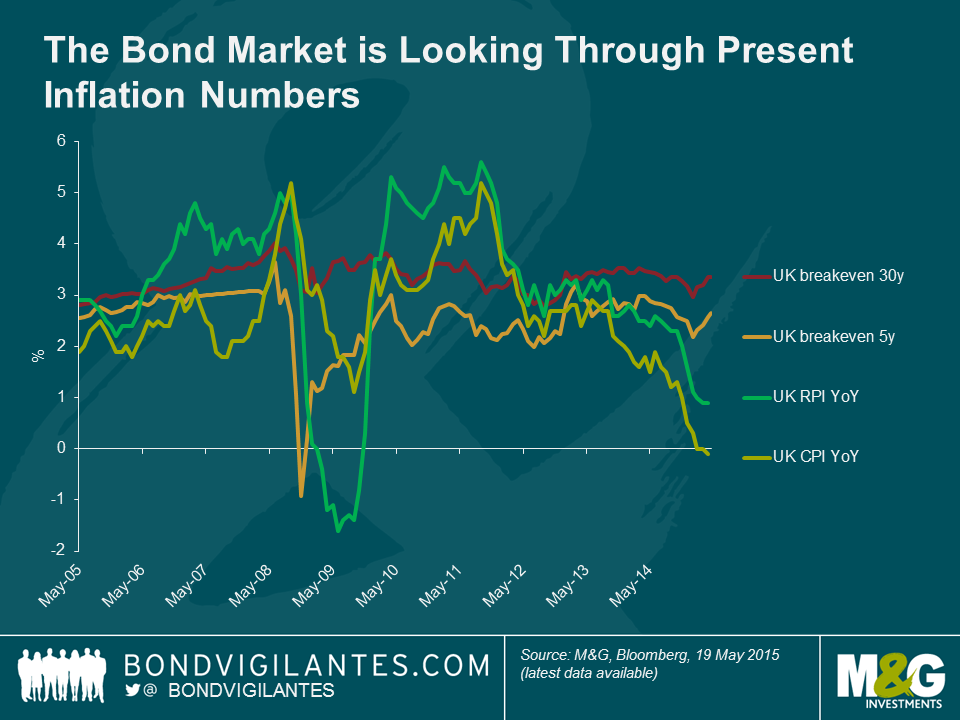

The market expects that deflation will be short lived in the UK. By the end of 2015, on the assumption of oil’s stabilising here or hereabouts, CPI will be 0.8% to 1% higher than today’s numbers, as the negative drag of oil’s decline will fall out of the year over year comparisons.

Also noteworthy is that with RPI in April registering a gain of 0.9% year over year, the ‘wedge’ (the extent of the difference between RPI and CPI) has increased to 1%, which is slightly higher than the long-term average. Whilst most of this difference owes to different calculation methodologies (the formula effect), some of this also owes to RPI’s greater inclusion of housing than CPI. Indeed, following the election result and the early signs of a relief rally in the housing market, one should potentially be watchful for the wedge trending higher in the medium term. This is especially important for investors in UK inflation linked bonds, as RPI is the benchmark. In other words, holders of inflation linked bonds are a safe distance away from a deflationary outcome, and the aforementioned base effects should mean RPI moves higher towards the end of the year.

If anyone is looking for potential reasons to see upside inflation surprises, they should be mindful of real wage growth accelerating from here, as well as consumer confidence. Both of these indicators are suggestive of a benign disinflation in the UK at the moment rather than anything worse, with wages on the rise (and having just increased by 0.1% in real terms today), and with consumers indicating that they are more, not less, inclined to make major purchases at this point.

With 5yr breakevens in the UK at 2.65% today, it is very evident that the bond market is looking through the present headline inflation numbers to a more normal environment on average for the next 5 years. Whilst UK breakevens are not as cheap as they were at the turn of 2015, we still feel that the next 5yrs’ inflation outcomes are more likely than not to make an investment in inflation linked bonds a better one than in nominal bonds. Further illustration of the fact that the bond market is less than overly concerned with current low headline inflation numbers can be clearly seen from observing the 30yr, long term, inflation breakeven. At a cost of 3.35% for long term inflation protection, the fixed income market is paying more than the average price of the last 5yrs to protect against long-term inflation, at the very moment that CPI turns negative for the first time.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox