BHP turns to the bond markets for help

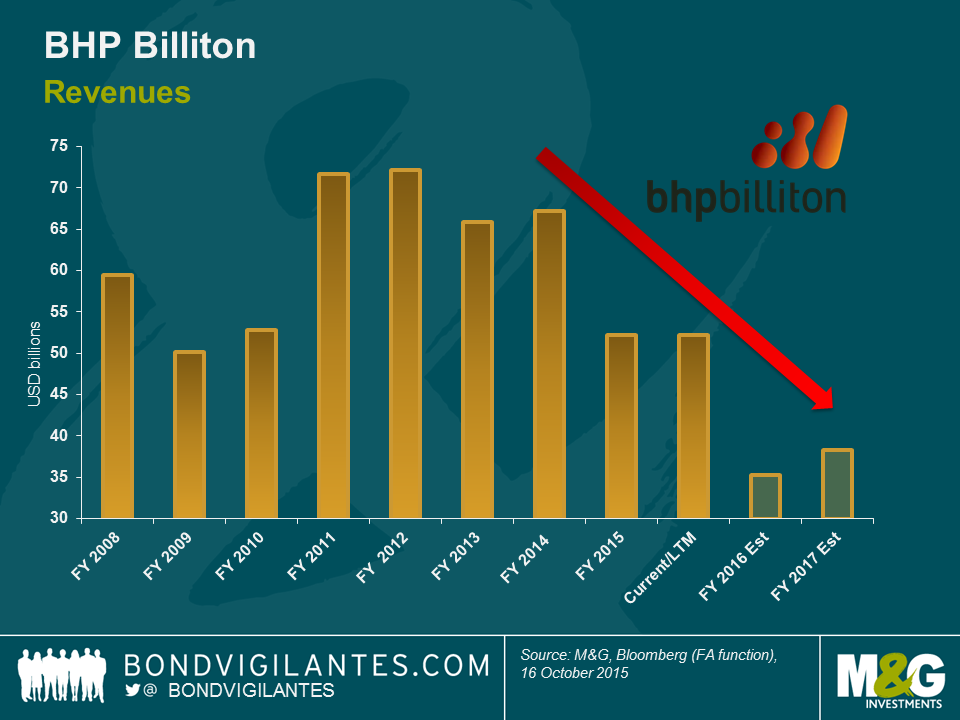

It has been a rough ride for metal and mining giant BHP Billiton. Revenues have come under persistent pressure due to weakening commodity prices. Despite one of the strongest balance sheets in the sector, promises made to shareholders have proven tough to keep.

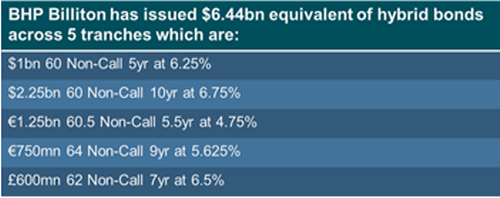

With these commitments in mind the company turned to a nervous bond market earlier this week for some $6.44bn equivalent of hybrid debt funding as outlined below.

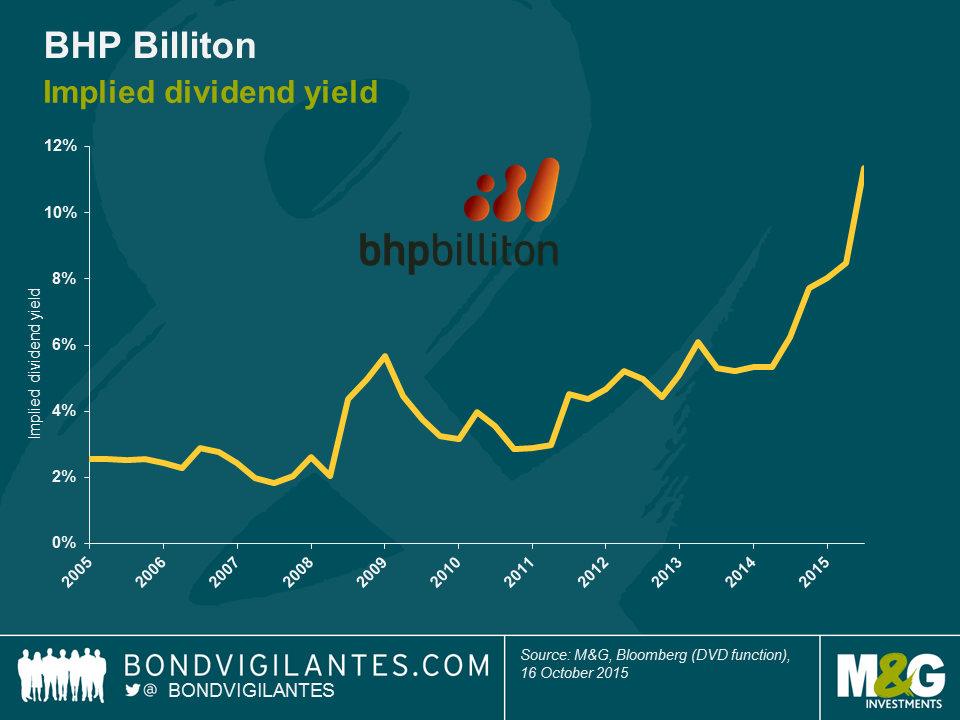

Back in May 2015 BHP spun off certain assets into a new business – South32 – whilst assuring investors it would be able to maintain the company’s dividend in line with its policy to ‘steadily increase or at least maintain the dividend per share.’ At current prices and despite a significant cost cutting exercise, the company will be free cash flow negative to the tune of -$2.5bn after maintaining said dividend. With little sign of a near term recovery in commodity prices and a commitment to a solid single A rating, it would seem management have somewhat backed themselves into a corner. A sceptical equity market has watched the implied dividend yield climb significantly through 2014 and 2015 to an elevated 10% area today.

Locking in a blended cost of hybrid debt funding at 6% for a minimum of five years, primarily to maintain the dividend in the face of commodity weakness, may well prove to be a costly error. With an interest bill set to rise by $160m per annum (before tax shield savings), perhaps a near term cut to the dividend would have been a more appropriate response which frankly is already discounted by the market.. Companies often pay special dividends when times are good and turn to bond markets when times are tough. The reason is that reducing the dividend can be a costly exercise for existing equity owners which is a short-sighted strategy in my opinion. Cyclical companies – like BHP – should leave themselves scope to respond to both cyclical downturns as well as upturns. No one can tame the commodities cycle.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox