Unconventional interest rate tightening underway in the US economy

Last week, the Federal Open Market Committee (FOMC) decided that despite low unemployment and a sustained increase in breakeven inflation expectations since September, it was appropriate to maintain the Fed Funds rate between 0.25-0.50%. In trying to understand this action, and why the Fed is happy to wait until December to hike rates, a number of theories have been suggested by the financial community. These include:

- The FOMC is waiting for the election to be out of the way for political reasons, before enacting further tightening;

- The FOMC is refraining from tightening as even though the Fed Funds rate is low, it should have gone negative after the crisis but was constrained by the zero bound;

- The economic cycle is already a long one and the FOMC are worried about potentially tightening policy into an economic downturn;

- The FOMC genuinely don’t know that they are making a policy mistake and are underestimating the build-up in inflationary pressures.

From reading my opinion in previous blogs you will find that I agree with the reason number 4. A tight labour market, developing wage pressures, and the dissipating deflationary impacts of a collapsing oil price, suggest to me that the US economy needs higher interest rates.

What is less well known than the official Fed Funds rate, is that under the surface there has actually been a steady tightening of policy in the real world that the FOMC has been happy to accept.

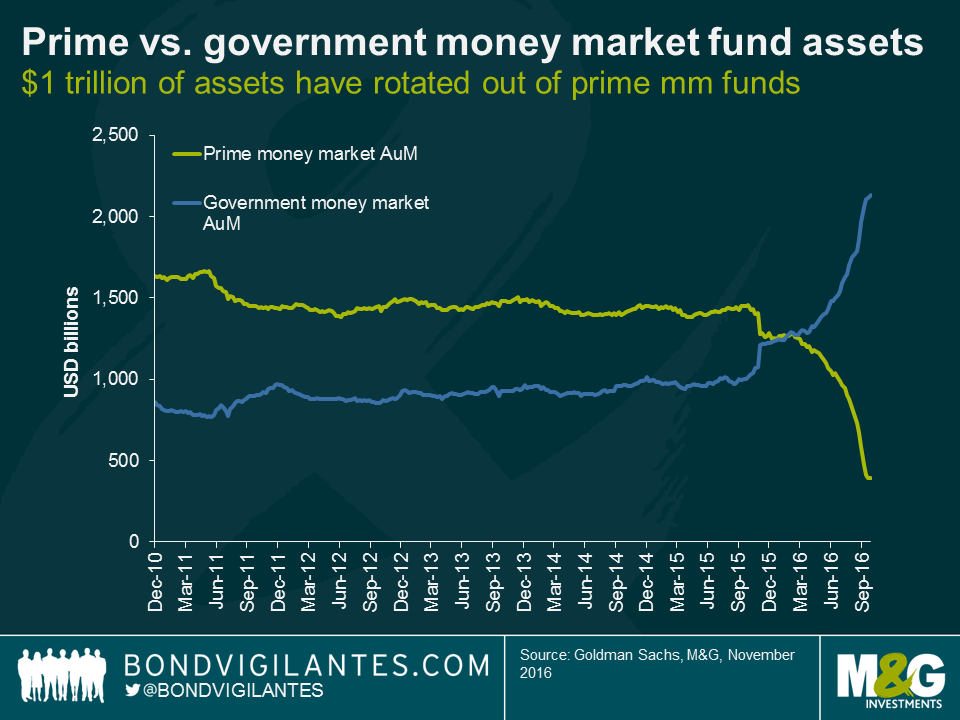

As a result of regulatory changes, money market reforms that require non-government funds to be market-to-market to protect investors came into effect in October. The rule changes were designed to make money market funds more resilient to market volatility and to provide greater protection for investors in a fund that “breaks the buck” (has securities repriced to below par). Of course, investors prefer return without risk, and these reforms mean that price volatility now explicitly sits in the non-government money market. Not surprisingly, short-dated risk-free money has dashed from prime commercial paper funds (that now have a floating net asset value) to treasury funds that do not have an explicitly variable net asset value. According to Lotfi Karoui and Marty Young at Goldman Sachs, assets held in prime money market funds have fallen by almost $1 trillion over the past year and rotated into government money market funds.

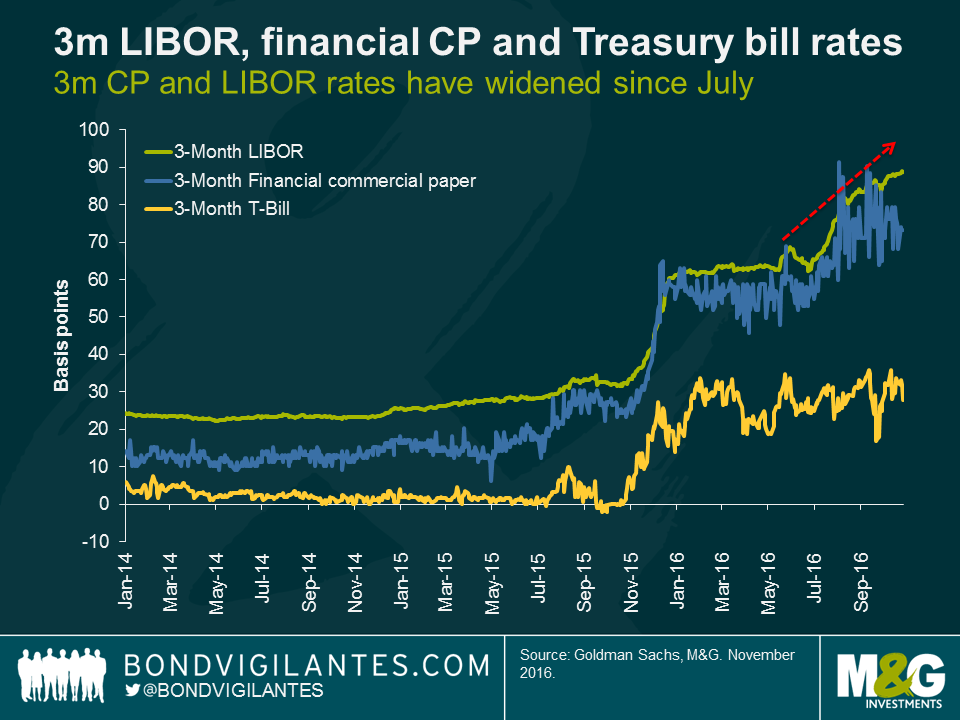

This means that despite no official headline tightening, real short-term funding costs as measured by LIBOR have increased by almost 30 basis points since June, leading to significantly higher funding costs for banks and other commercial paper issuers.

Investors always focus on conventional headlines, but it often helps to look at the real narrative. Money market reform is doing the FOMC’s job for them, which is a form of unconventional interest rate tightening. Consequently, the FOMC may be more hawkish than economists think as they are happy to accept this market tightening, which has had a similar impact on LIBOR as a traditional move in the Fed Funds rate. This effective tightening of policy means that maybe the FOMC’s views and my own are now less far apart than one might think.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox