A dozen things I’m finding interesting in bond markets. Includes weasels.

1. On the face of it, long term US Treasury yields are looking fair value, having traded on the dear side since the middle of 2014. Below is a chart you will have seen before on the blog as I’ve been using it for some time. It shows the relationship between the Fed’s long term expectations of short term interest rates (taken, with a pinch of salt, from the FOMC’s dot plots) and the bond market’s expectation of the 10 year US Treasury yield in 10 years’ time. In both cases, we are ignoring the immediate economic ups and downs, and even the possibility of an eight year Trump presidency.

Since the US election, the Treasury market has moved to price in a term premium of over 50 basis points and is arguably “cheap” compared to the median FOMC member’s long term Fed Funds expectation. Are there reasons why this simple model could be wrong? Of course there are. The term premium might not be sufficient, perhaps because of the “Chinese demand” factor I discuss below; and the FOMC and markets might significantly revise their expectations of the long term Fed Funds rate higher. After all, it’s come down from a median of 4.25% in 2012. If Trump is serious about a 4%+ real GDP target then it will head back there.

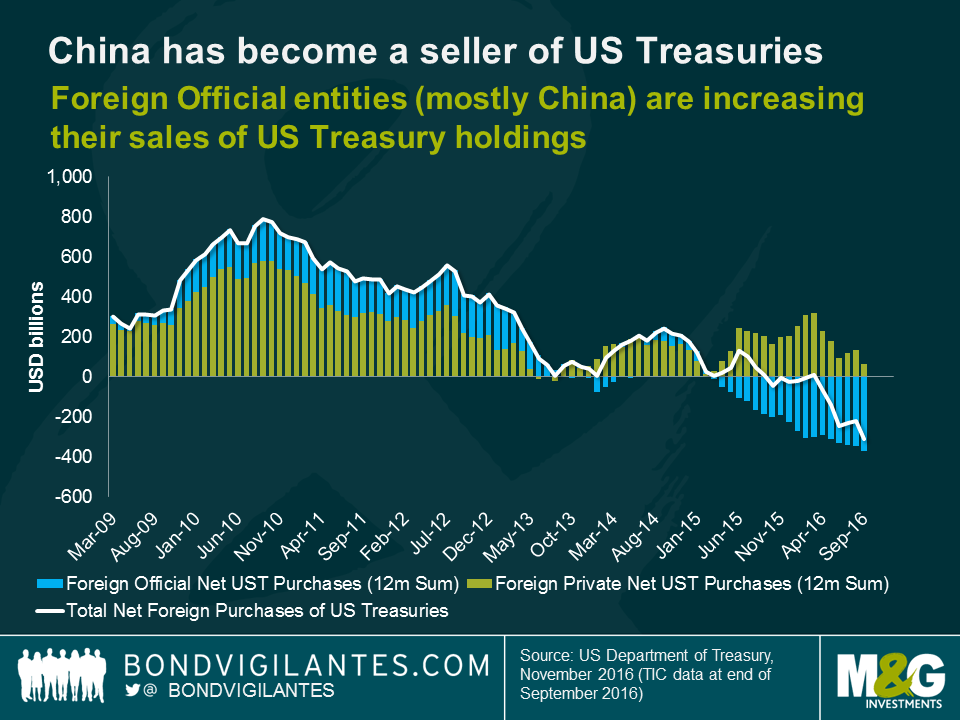

2. China joined the World Trade Organisation (WTO) at the end of 2001. Since then it’s accumulated, at peak, $4 trillion of foreign exchange reserves as a result of its trade earnings. Much of this ended up in the US Treasury market – China owns 20% of the market, with Japan owning another 20%. One estimate suggests that China’s purchases alone resulted in the 10 year Treasury yield trading 50 basis points lower than it otherwise would. However, the chart below shows that since the Chinese slowdown began in 2012, they have moved from being net buyers of US Treasuries, to net sellers. Additionally, since the start of 2016 foreigners as a whole have become net sellers of Treasuries. What was once a powerful tailwind for the Treasury market for the decade prior to 2016 has become a headwind. Perhaps a higher term premium is therefore appropriate.

3. Another headwind for US Treasuries is the cost for foreigners if they buy and hedge American bonds. Negative rates and ultra-low bond yields in Europe and Japan have left investors struggling to achieve yield targets (for example insurance company guarantees). On the face of it, a 2.5% 10 year US Treasury yield looks attractive if the alternative is a 0.5% yield on a 10 year German bund. Unfortunately, the weight of capital attempting to buy Treasuries out of Europe (and Japan) and then hedge the foreign exchange risk means that the “fx basis” (the supply and demand overlay to the fair value hedging cost assumption based on relative interest rates) is high. For Japanese investors the basis is -50 basis points and for Europeans it’s -35 basis points. This means that for a hedged investor in Japan the yield on the 10 year US Treasury is actually 0.55% and for Europeans it’s 0.46%. Whilst the negative basis isn’t as big as it was around the end of 2016 (-90 basis points for Japan and -60 basis points for Europe), it still doesn’t make sense for European investors to add to US Treasury positions in the hope of gaining a yield pick-up. Japanese investors now do achieve a premium once more, following the narrowing of its basis.

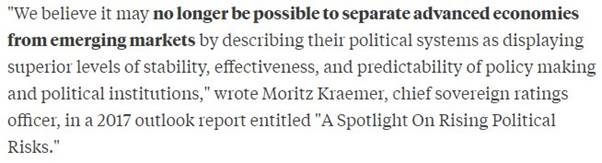

4. I didn’t spot this at the time (December), but Tracy Alloway of Bloomberg reminded me yesterday of S&P’s 2017 outlook piece by the excellent Moritz Kraemer. This quote from the document is chilling, if perhaps overdoing the collapse in the democratic and legal institutions that historically gave developed economies a ratings advantage over the emerging market nations.

5. I love a good “driverless cars” story. 94% of car accidents are caused by driver error. 32,000 lives are lost as a result in the US every year. 1 in 5 organ donations result from car accidents. If driverless cars are (presumably) better at driving than humans, then the shortage of donor organs is going to rise significantly. Another good “driving” story: for every 1% rise in unemployment US, 5000 fewer Americans die, as downturns keep especially dangerous drivers off the road. There is an obvious point that lower economic activity means that people drive (and can afford to drive) less. But the biggest decline in driving when growth slows, comes from the worst drivers. You can read some of theories in the article.

6. This National Institute of Economic and Social Research (NIESR) paper by Dr Monique Ebell is worth a read to understand the impacts on UK trade if we leave the single market. Dr Ebell estimates that the long term impact will be a fall in UK trade of up to 30%. The UK could experience an increase in trade with some countries – if the UK got a Free Trade Agreement with all of the BRICs then trade would rise by 2%, and an FTA with the Anglo-American economies would boost trade by just under 3%. Unfortunately, neither increase would make much of a dent in the drop in EU trade of 35%. Ouch.

7. The collapse in Trade Union membership continues, despite the rise in populism and rising anger at the weak income growth in the working and middle-classes in the developed world. Only 10.7% of Americans are union members, down from 11.1% two years ago, and 20% in the 1980s. The number of union members in the manufacturing industry has fallen by over 50% since 2000. Whilst I can see US wage growth hitting an annual rate of 3% later this year, it’s hard to see this becoming a sustained rise, especially in light of a relatively low participation rate in the US (compared with pre-GFC levels).

8. Duncan Weldon’s blog about The Second World War is good. Do we focus too much on the victory in battle, and not enough about how the UK won the peace?

9. China economist Michael Pettis is ace. Not only is he popping up at every economics conference I attend, anywhere in the world, but he’s popping out of my radio on a Sunday morning talking not about Chinese state-owned enterprises, but about the Chinese punk music scene. He asserted on BBC Radio 6 Music’s Mary-Anne Hobbs show that in a cultural history of the 21st century, Chinese alternative music of a decade ago will be one of the most significant movements. I’m sceptical, but UK readers can make up their own minds and “listen again” through the link above.

10. My favourite book to come out of the Great Financial Crisis was “This Time is Different” by Carmen Reinhart and Ken Rogoff. The authors demonstrated that nations which saw public debt to GDP ratios near 100% experienced significant growth slowdowns. There was some great economic history in a very readable book. I have started wondering though, in a world where growth has been sub-par for most of the developed world, whether this book was responsible for an “austerity meme” which has caused big damage to the global economy (and the subsequent political instability). We know that Keynesian responses to a demand shortfall work (discuss…) – so did this book result in the opposite happening in the UK under Osborne, or in Europe where Germany is running budget surpluses? How important was it in helping to create the low growth world that we’re now in?

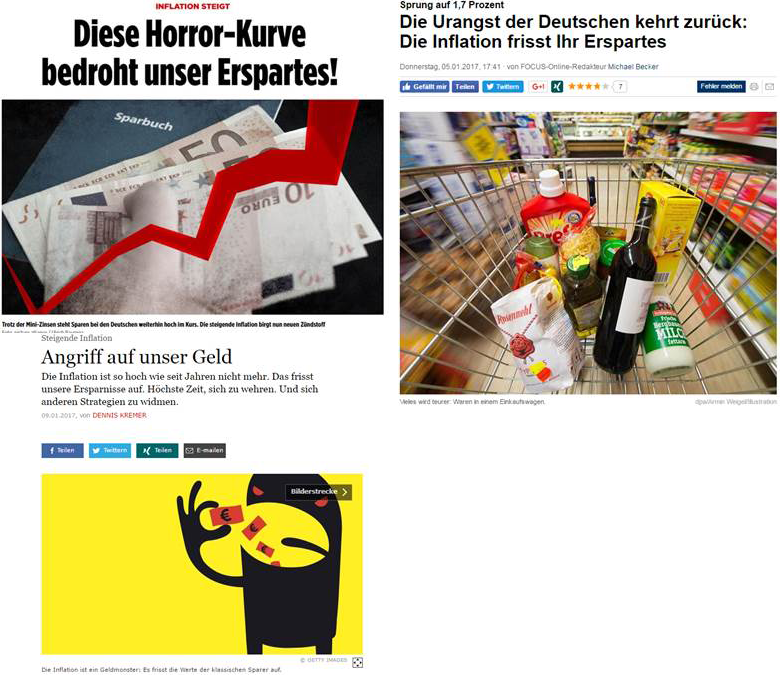

11. Talking of Germany, here are some newspaper articles from the past few weeks (Bild, Focus, FAZ) about German inflation edging back towards 2%. They are worried…

12. Finally, I’m in no way blaming our new(ish) CEO Anne Richards for the death of the weasel in the Cern Large Hadron Collider. It looks as if Anne left Cern before the stone marten was slayed with accelerating particles. Anyway, the stuffed Cern weasel is now available to be gawped at in Rotterdam if you want to see it. I am however staying away from all large electrical devices in M&G HQ for the foreseeable future. This included my Bloomberg terminal for two days last week when a vicious papercut and battlefield dressing (a plaster) meant that I was unable to get past fingerprint authentication…I had a great two days.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox