Our demographic challenges require new economic thinking

Capital markets have experienced a major shift in sentiment over the course of the last couple of months. Fears over secular stagnation and deflation have dissipated, and investors have been willing to embrace risk assets again. Many economists have revised upwards their estimates of global economic growth, starting first with the US where the fiscal reigns are expected to be loosened in order to meet some of President Trump’s pre-election promises to voters.

Whilst there is clear short-term momentum in economies like the US and UK, where unemployment rates are low and consumption is robust, there remain long-term secular themes that investors should be aware of when they formulate long-term investment decisions. One of these themes is a shift in the focus of economic policy, driven by demographics. Unlike economic variables, demographic trends are predictable and greatly impact all of us.

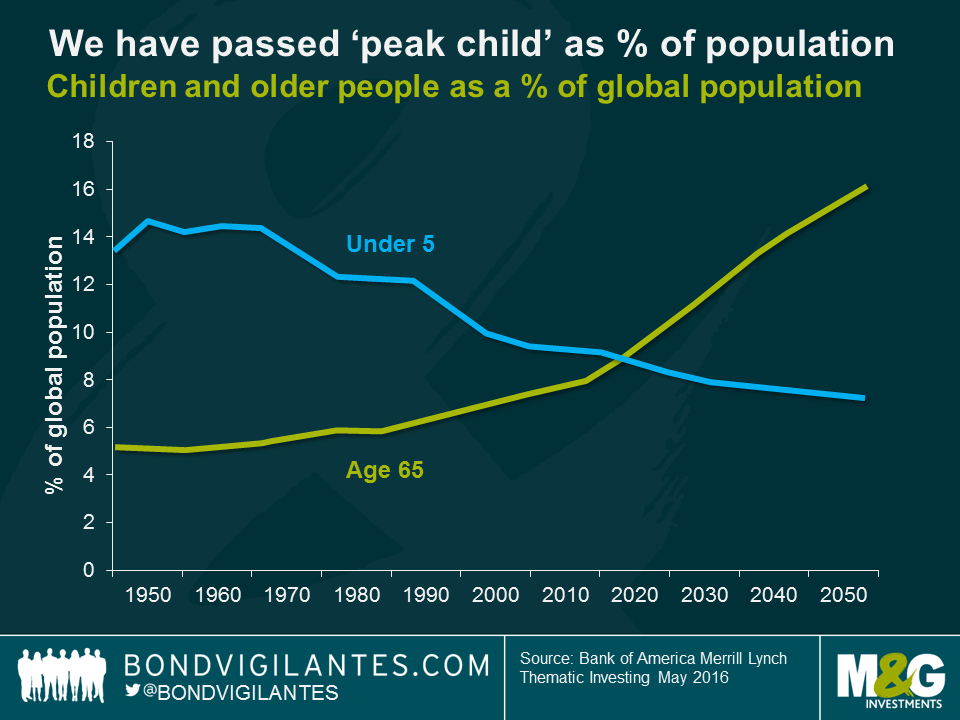

The global economy has now passed an important tipping point. For the first time in recorded history, children under the age of 5 no longer outnumber those aged 65 and above. We have arrived at “peak child”.

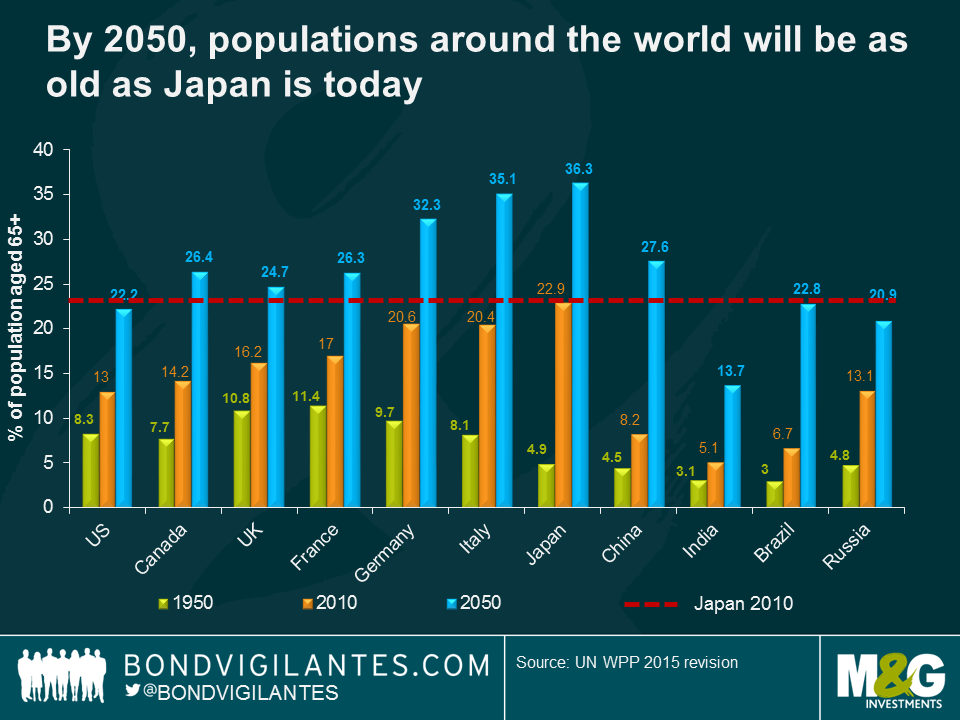

The United Nations has estimated that the global population will continue to age, and by 2050 over 15% over the global population will be aged over 65. Economists often point to the challenges that Japan faces as the population ages; by 2050, most of the G7 will have a similar demographic profile as Japan does today, as will China, Brazil and Russia. Longevity risk, the risk that people live longer than expected, could put huge pressure on our current retirement systems. Research from Merrill Lynch Bank of America suggests that age-related spending is already 40% of government spending in developed markets, and as high as 55% for the US. Rising healthcare costs could push 60% of developed market sovereigns sub-investment grade by 2050 without significant policy action.

In order to meet the challenges presented by an ageing society, we will need to work longer and think about policies and initiatives that incentivise people to work past the traditional retirement age. If these issues aren’t addressed, increasing old-age dependency ratios could have wide-ranging impacts on government finances, productivity rates, and inequality. Additionally, we need to have a think about what economic success looks like.

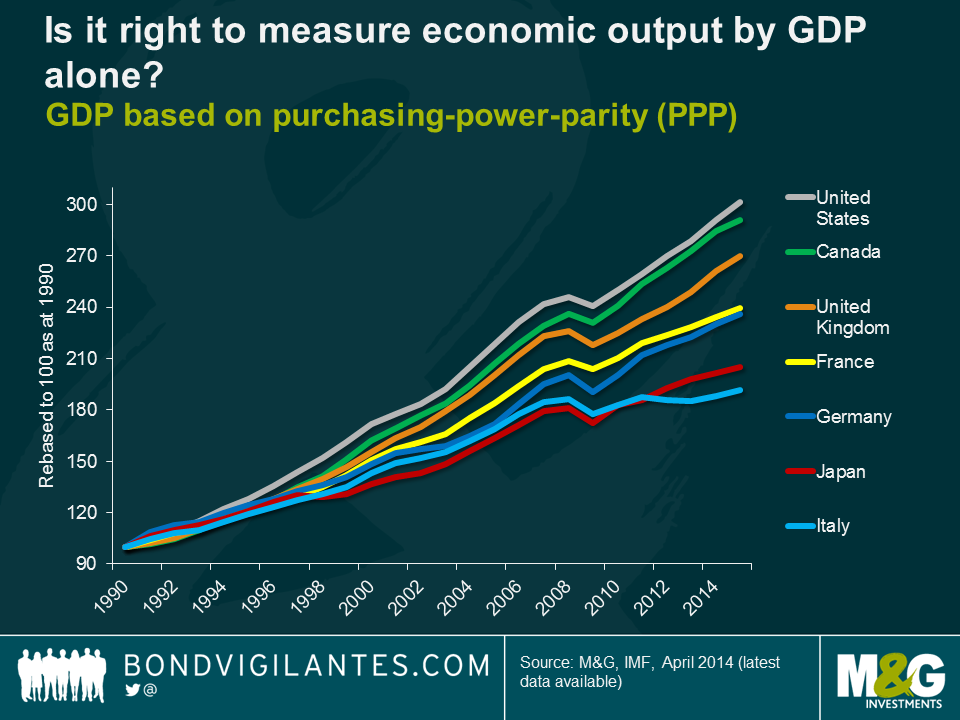

Aging populations represent a huge success for science, with medical advances extending the lifespan of the average human by decades. They also represent a huge challenge for policymakers, and our economic model needs to adapt to this shifting demographic. As Richard has pointed out previously, Gross Domestic Product (GDP) is used by policymakers and economists as a yardstick to compare the relative success of economic policy across the globe. However, using GDP as a measure of economic success is misleading. Focusing on Japan (as an economy that has experienced a high public debt/GDP ratio, private sector and household deleveraging, deflationary pressure and an aging population) we see that GDP suggests that the country is an economic laggard compared to the rest of the G7.

However, looking at GDP per the population of working age (15-64) shows that Japan has enjoyed the third best economic performance in the G7 since 1990. Consequently, Japan has enjoyed a much stronger economic performance than many perceive. Rather than experiencing “lost decades” of growth, the Japanese economy has experienced stable prices, low unemployment and low interest rates. For the average Japanese citizen, living standards have not deteriorated, and on the contrary have improved.

In a world where immigration policy reform is increasingly dominating political agendas, policymakers should recognise that GDP largely reflects a demographic profile where more workers enter the workforce, who (if everything goes to plan) will then produce, earn, and consume more than the previous quarter. Naturally, as the workforce shrinks due to ageing, the reverse will be true. However, it does not necessarily mean that an economy is underperforming if the trend rate of growth is falling to reflect a smaller workforce. The changing demographic trend that the developed and parts of the emerging world are now experiencing will increasingly act as a headwind to global GDP. China in particular, which has driven global growth post-crisis, will likely slow markedly in coming years from historic growth rates. In the future, it will be important for policymakers to look beyond GDP as a measure of economic success, in favour of alternative measures which look at economic well-being.

Whilst it is easy to focus on near-term tactical shifts in markets, it is increasingly important to focus on long-term secular trends that are re-shaping the economies that we live in. Higher rates of GDP are not necessarily the answer to face the challenge of an aging population. Individuals, companies, and governments will have to adapt to these challenges, and we may find that in the future we see a greater focus on intergenerational fairness and living standards than has historically been the case.

Of course, the effects of ageing will have far-reaching impacts on financial markets. Ageing societies will usher in an era of saving, which should provide a tailwind for companies that help people plan, invest and save for retirement.

Fixed income and dividend-paying equities will probably benefit in this environment given both asset classes provide a regular income for retirees to use.

Additionally, the structural demand for longer-dated bonds from insurers and pension funds may limit the extent to which bond yields can rise in the future.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox