The decline of covenants in the European leveraged loan market

Guest contributor – Chris Mansfield (Investment Graduate, M&G)

The sustained demand for high yield bonds and European leveraged loans over the past few years, combined with improving corporate fundamentals, has led to strong performance from both asset classes. The large amount of capital available for issuers of higher yielding assets has placed the bargaining power squarely in the hands of the borrowers, and they’ve exercised this power unreservedly on the covenants offered with new deals. In 2014, James wrote about the deterioration in high yield bond covenants. Since then, little has changed in this market; spreads have just grown tighter. The European loan market, by contrast, has seen some dramatic changes to standard covenant packages over the last five years.

Back in the aftermath of the crisis, the average European leveraged loan deal came with four maintenance covenants. In rough descending order of importance, these were: leverage, interest cover, debt service cover, and capital expenditure. Respectively, these covenants: limited the ratio of net debt to EBITDA (and often enforced a reduction over time); imposed a maximum ratio of interest costs to operating income; enacted a maximum ratio of current debt obligations to cash flow; and limited capital expenditure as a proportion of cash flow or cash-like earnings.

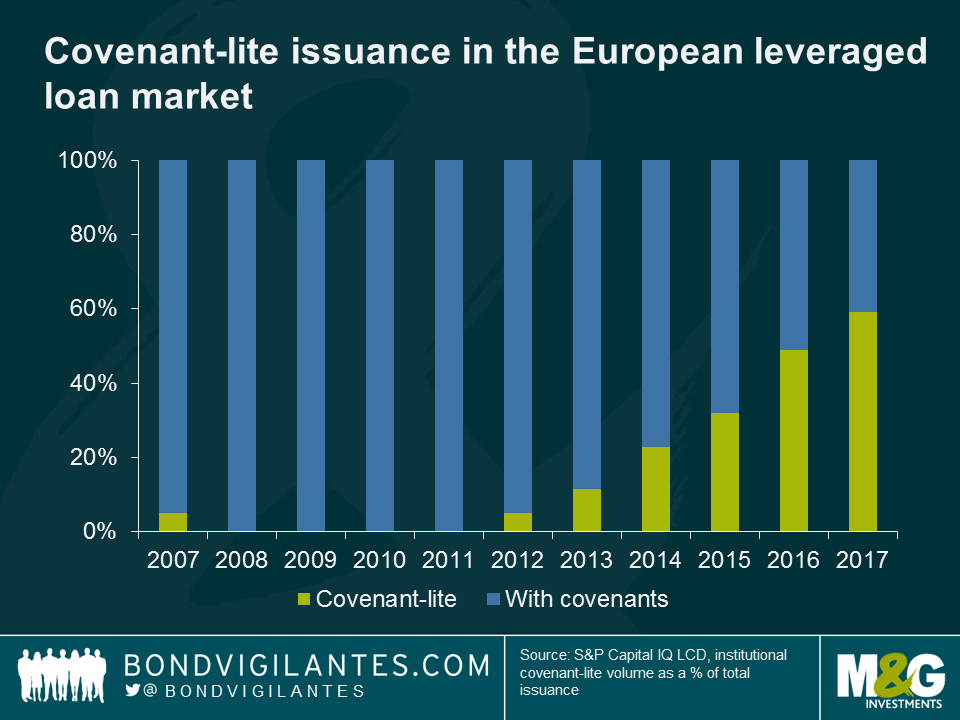

Since then, and over the last five years in particular, the maintenance covenant package initially dropped to typically just leverage, and now ‘cov-lite’ is a common term used to describe loan deals with no maintenance covenants at all (NB incurrence covenants still remain present). As shown below, the proportion of leverage loan deals that are cov-lite has been growing steadily.

Of the deals that aren’t cov-lite, there is almost always only one maintenance covenant – leverage. And whilst it’s still present, its power has depleted. Historically, the headroom (distance between current pro forma leverage and the leverage ratio in the covenant) was around 25%; this is now more like 40%. The leverage ratio used to ratchet down over time, forcing the company to de-lever; today the ratio profile typically remains flat. Lastly, the documentation typically allows ‘adjusted EBITDA’ and even ‘net debt’ to be redefined, all combining to mean that the typical leverage covenant today is a weak shadow of its former self.

In the loans market the demise of maintenance covenants limits the power lenders have to stop the issuer aggressively reducing its creditworthiness whilst pursuing some (presumably shareholder-value-enhancing) strategy, raising downside risk. The result is that any macro factors that impact corporate fundamentals could see a sharper sell-off, hurting investor wealth, and potentially a corresponding decrease in recovery rates, compared with a European loans market where maintenance covenants remained unwavering. The corollary is that full due diligence and credit research is more important now than ever.

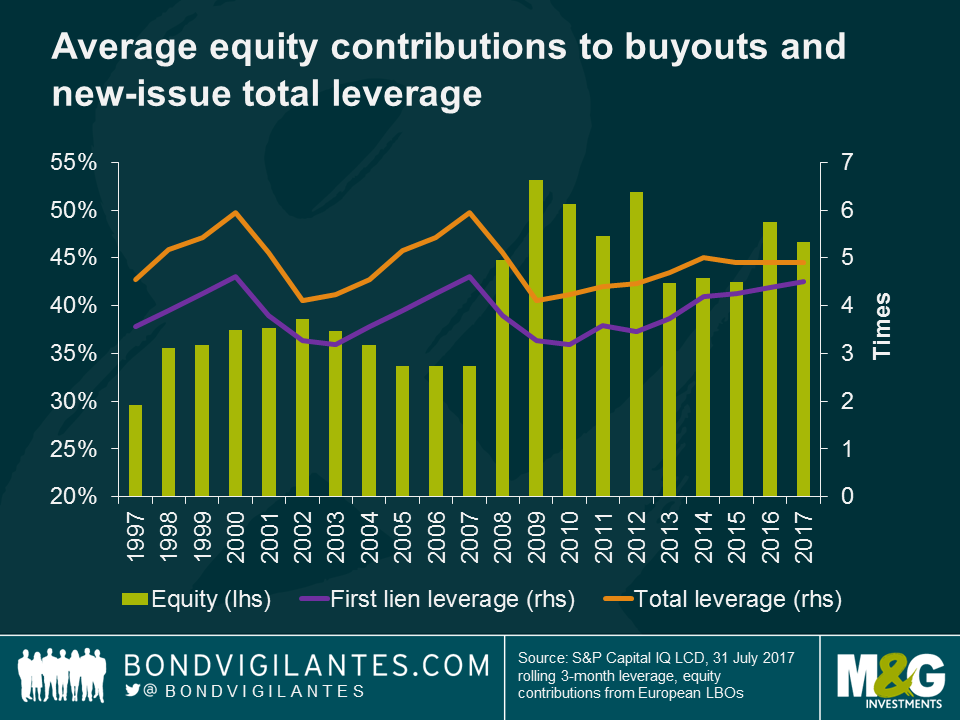

That said, there have been some more positive trends. The average leverage on new leveraged loan deals remains below the pre-crisis peak and is expected to stabilise at the current levels, and the average equity contribution in buyouts is now closer to 50% (and growing) than the c.40% seen in 2013-2015. These act as positive forces on recovery rates, possibly counteracting the above comment.

A question for investors is whether the overall terms on offer provide adequate compensation for the heightened risk resultant from covenant demise. They may well do given the context of other asset classes, but it’s unarguable that this decline in lender protection is unwelcome. So what should investors make of it?

Demanding a higher risk premium as compensation seems an obvious solution, notwithstanding the fact that spreads in the loan market have remained broadly flat in recent years amidst tightening in other markets. However, given the need of investors to deploy cash when inflows are strong, voicing disdain in either market – by declining to participate – is a difficult game to win. Some sort of unionisation of investors to ignite pushback would likely be the most effective solution.

The issue that stops investors from pursuing this strategy is that each individual would rather everyone else bore the effort. Additionally, investors may miss out on investment opportunities during such a pushback. Aggregate this desire across all investors and combine with the need to invest inflows, and you have one tricky problem to solve. Perhaps only a downturn will empower investors to demand the protection of the past.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

18 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox