Cross currency basis – what is it? And what are the implications?

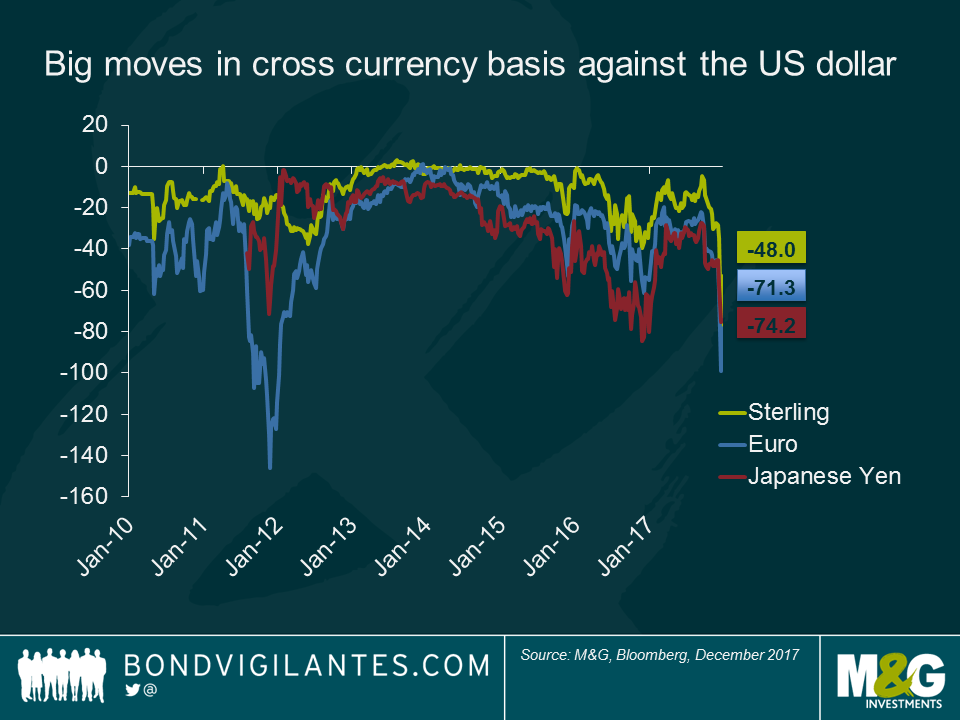

Towards the end of this year, a December spike in the cross currency basis for major currencies against the dollar grabbed the market’s attention. But what is cross currency basis (“the basis”)?

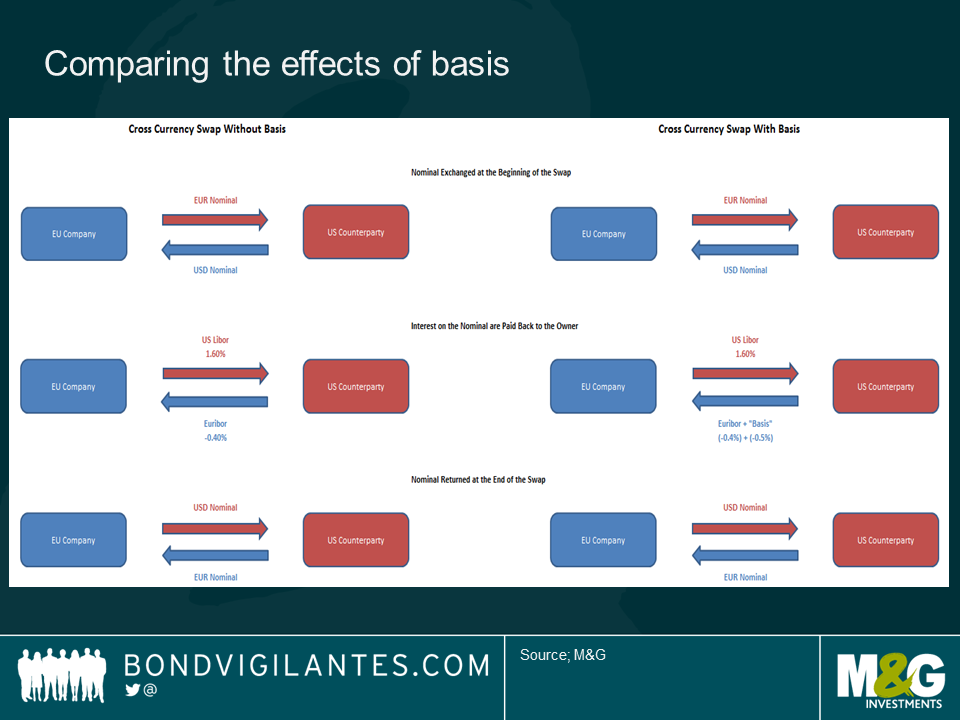

Consider a European company taking a one year loan from its domestic local bank to fund its US operations abroad. In order to hedge the currency risk, the company enters into a one year EUR/USD currency swap with a market counterparty. The European company swaps a certain amount of Euros for US Dollars at today’s spot rate, agreeing to swap the funds back at the same rate in one year’s time. Because the European company doesn’t technically own the US Dollars, it will need to pay back US Libor as interest and by reciprocity, receive Euribor from its counterpart. This is how it should work in theory (i.e. according to covered interest rate parity).

In practice, however, whenever there’s a higher demand for the dollar, the counterparty lending the dollar will ask for a price premium. It is this amount which is referred to as the “cross currency basis”. In other words, the European company will pay out US Libor and will receive Euribor plus the cross currency basis (quoted as a negative figure).

Let’s look at an example: If today US Libor is 1.6% and Euribor is -0.4%, the theoretical cost of the EUR/USD currency swap to the European company is 2% (i.e. it pays out 1.6% on the dollar interest, but also pays out 0.4% on the Euro interest because Euribor today is negative). If, due to a dollar shortage, the counterparty quotes a “basis” of -50 bps, then the cost of this swap to the European company would increase to 2.5% (1.6% Dollar interest + 0.4% Euro interest + 0.5% currency basis).

In general, the cross currency basis is a measure of dollar shortage in the market. The more negative the basis becomes, the more severe the shortage. For dollar-funded investors, negative basis can work in their favour when they hedge currency exposures. In order to hedge foreign currency exposure, the dollar-funded investors lend out dollar today and receive it back in the future, earning additional cross currency basis spread on top of the yield of their foreign investments. In fact, for years the Reserve Bank of Australia has been swapping its other foreign currency reserves against the Japanese Yen in order to enhance returns. After taking the basis into account, negative yielding short-term Japanese government bonds actually yield higher than many short-term government bonds in other currencies.

For foreign investors, however, the basis could increase their hedging cost of investing in the dollar assets. In order to hedge dollar exposure, foreign investors borrow dollar today and return it back in the future. The basis is the additional hedging cost added to the interest differential of the two currencies.

Cross currency basis is an important part of currency management in a global portfolio. Given that the Fed is now well ahead of the ECB and other central banks in its monetary tightening cycle, it is likely that the dollar shortage could heighten in the coming year, and the basis could become more negative. Portfolio managers should be mindful of the hedging cost when taking foreign currency positions.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox