US long rates: is the giant anaconda about to turn?

The long-end of the US Treasury market has often been described as a giant anaconda: it draws little attention as it sleeps most of the time, but the minute it wakes up, everybody around shakes. US 30-year bonds don’t bite, but their moves can be as poisonous as they basically determine millions of mortgage rates, as well as the price that governments and companies around the world pay for debt. Is this market about to spring higher in yield?

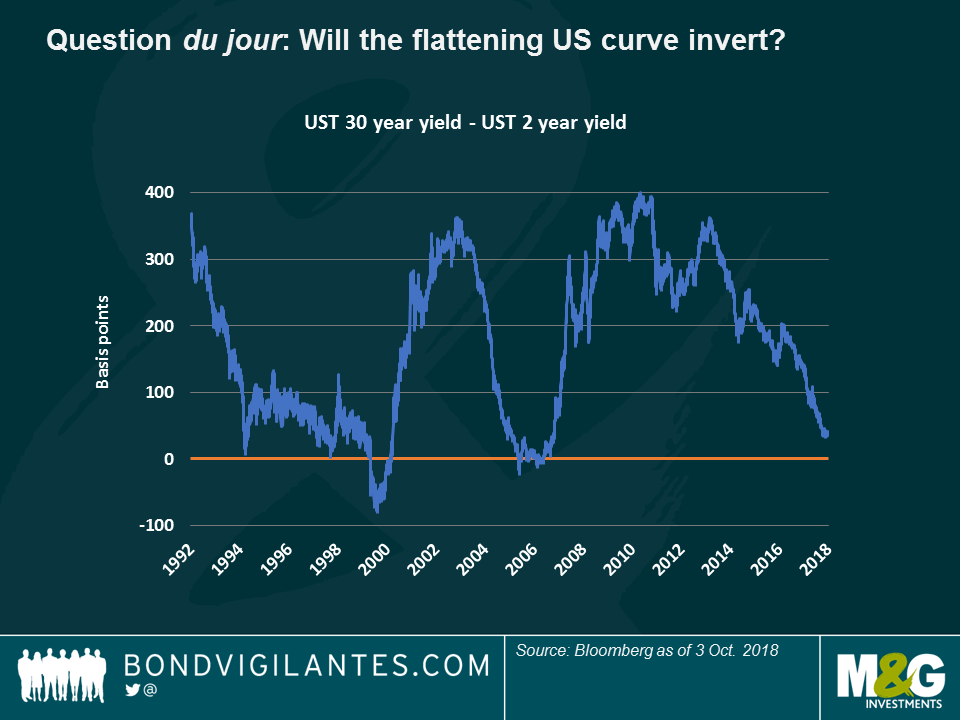

Until now, 30-year Treasury yields have generally made investors smile – a 600 bps rally over the past 30 years has made money relatively cheap, the term premium has collapsed, flattening the yield curve to levels not seen since the 2007-08 financial crisis, as seen on the chart below:

Investors are now watching this flattening with angst, fearing that it may signal a looming recession: when previous flattenings turned into an inversion in 2000 and 2006, a recession surely followed.

I don’t think this is the case now; more so, I believe we may see quite the opposite. This is because:

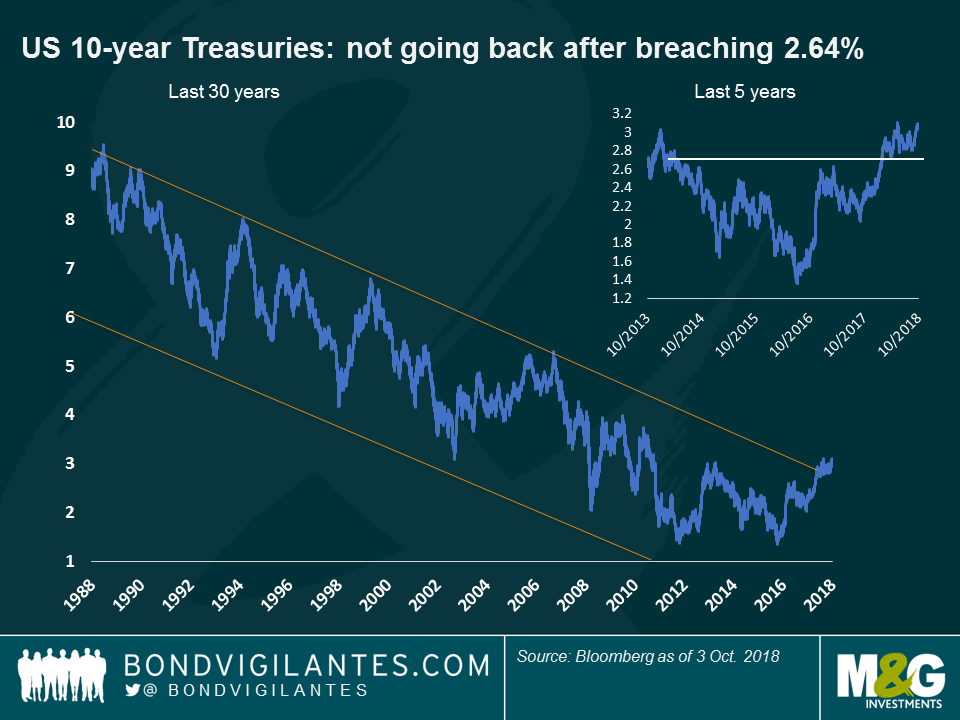

Technical reasons: 30-year Treasury yields could replicate what we saw in 10-year Treasuries earlier this year, and which I blogged about shortly before the market turned: after four years trying to surpass the 2.64% level, the 10-year yield finally breached through this level in February on the back of strong hourly wage data – finally a sign of inflation after a decade of dormant prices. This was a significant break of both the short and long term trends.

Could we be seeing a similar pattern in 30-year yields, which by nature are a bit slower to move than the more volatile 10-year market? As the chart below shows, 30-year Treasuries have also enjoyed a three decade-long bull run and have traded within a range between 2% to 3.25% over the past four years.

I believe this level could be breached soon: apart from an improving fundamental outlook (see below), the corporate tax changes from earlier this year encouraged underfunded pension funds to acquire long-dated fixed income securities by mid-September. Afterwards, demand for the asset class might drop, lifting yields.

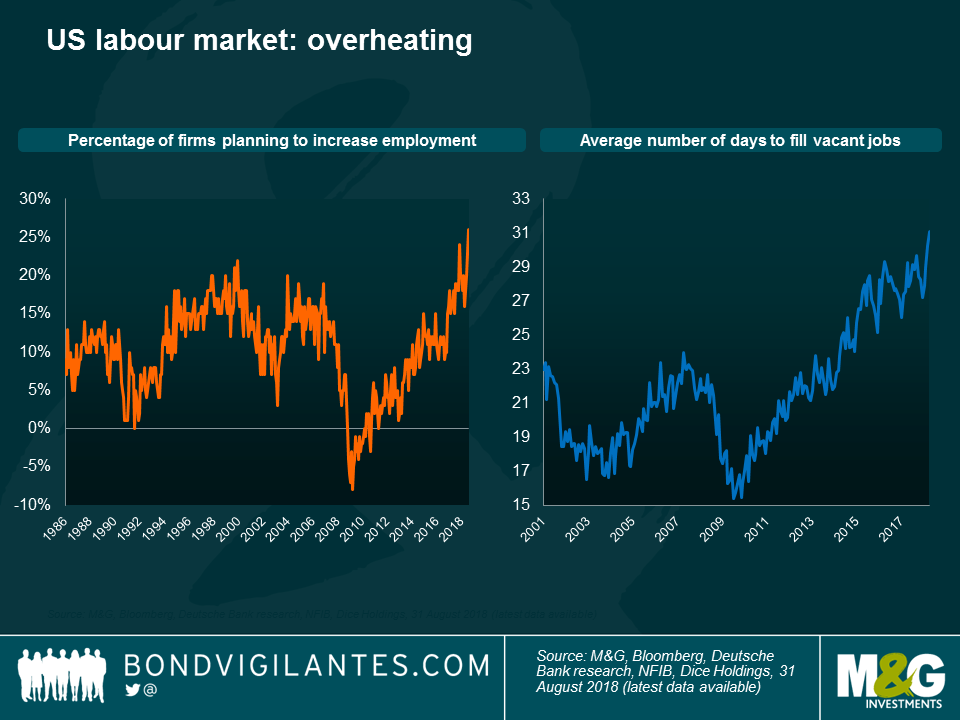

Fundamental reasons: More lasting than potential triggers or technicalities, I believe long US rates may rise as a natural reflection of a robust economy. While not growing at a spectacular pace, the US economy is producing positive data, which may generate more inflation soon – generally a precursor of higher yields. Let’s see what the job market is telling us.

The chart shows that US companies have increased their hiring plans, at the same that it takes them more time to find talent. We all know that a tight job market generally feeds into inflation and ultimately, higher rates. Anecdotally, tech giant Amazon just announced a wage rise for its employees, a clear sign that the market is tight – if anyone knows the outlook for the economy and how tight the labour markets are, then Amazon should. Maybe Amazon provides another clue to the waking Anaconda of rising rates.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

18 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox