Is China really a currency manipulator?

Last night, the US Treasury designated China as a currency manipulator. This has occurred a few times in the past, most recently in 1994. Though China has been on the Treasury’s watch list for some time (alongside several other countries), given that the most recent Treasury report published in May did not name China a manipulator, it begs the question, what has changed between then and now?

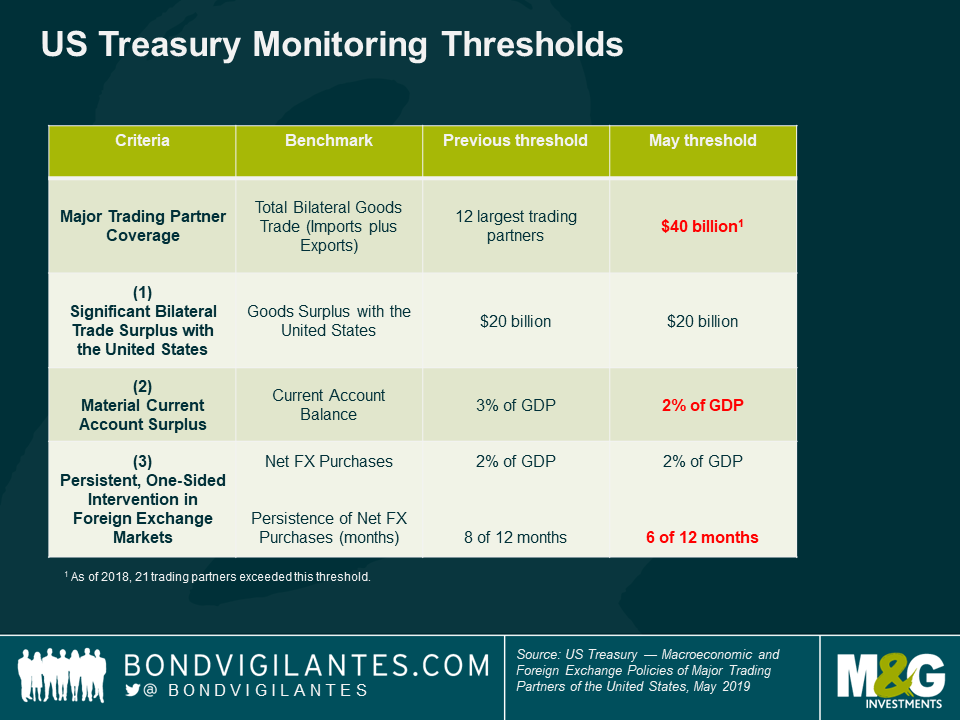

The criteria is based on the chart below. One of the issues with the criteria is that it focuses on the largest bilateral trade deficits in nominal terms. Arguably, this reduces the need to monitor bilateral imbalances for economies that are much smaller in size, where the surplus may be large (as a percentage of the economy) but small in nominal terms. One example is Israel, a small economy that posted a larger surplus, as a percentage of its GDP, than several other countries on the monitoring list (see our prior blog) This also means that a small open economy like Thailand would fall just below the $20 billion arbitrary threshold, but India, a larger closed economy would just exceed the threshold.

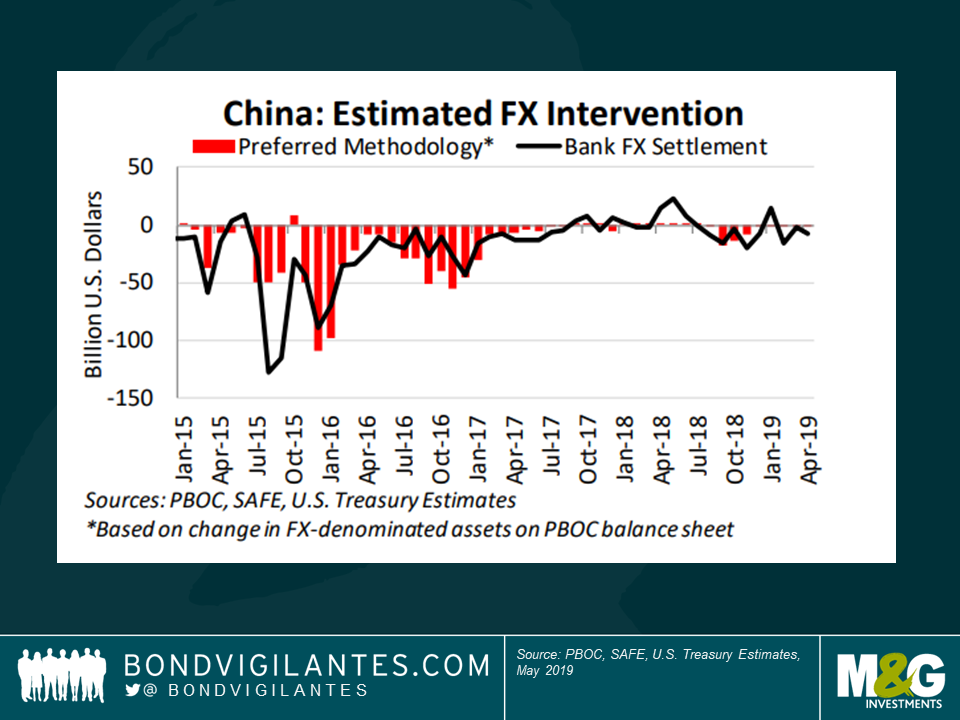

According to the Treasury’s most recent estimates below (China does not publish that data), China has not materially intervened in the currency for a large part of the last year. If anything, it was selling USD reserves to prevent a faster depreciation in 2015-2016, when it further tightened capital controls. Based on PBoC data, we do not believe it has materially intervened to weaken its currency since then. The Renminbi has however now crossed the 7 rubicon.

The US Treasury believes that China’s reserves are ‘above standard measures of reserve adequacy’. That may be true for a country that has capital controls, but as China aims to gradually open up its capital account, the level does not seem to be excessive. Reserves have been relatively stable since 2017 at $3.1 trillion, so the IMF’s calculations below are still valid.

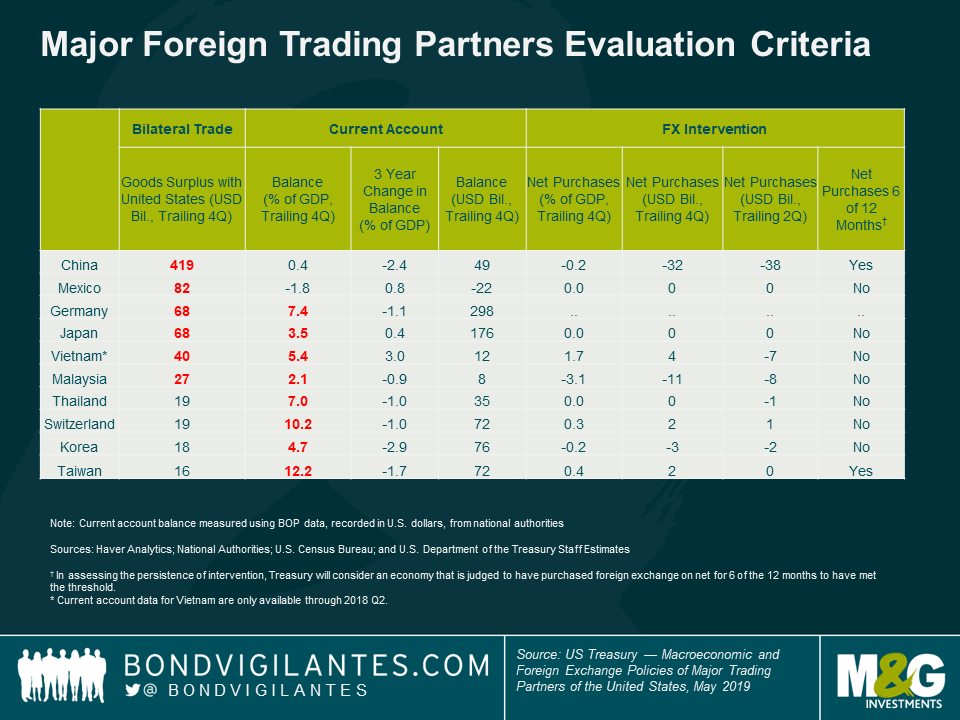

From the criteria described above, it appears that nothing is likely to have changed since May, except that the trade war between both countries has intensified. China has been running large bilateral trade surpluses with the US for some time and the US allegations of protectionism and state subsidies are warranted, but nothing new.

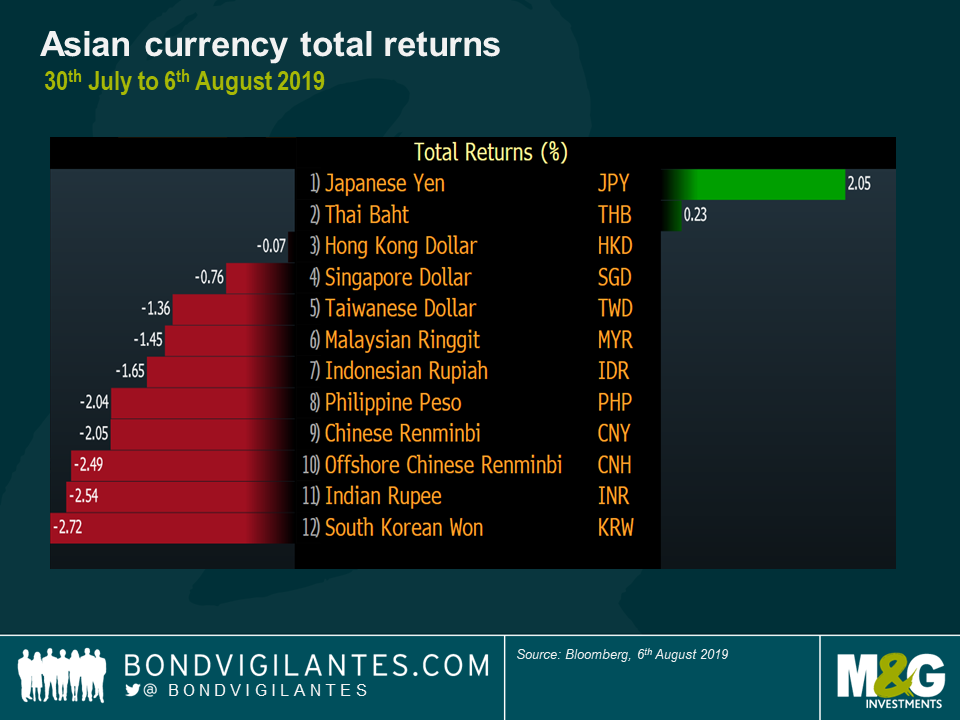

Following the recent US announcement that they will impose 10% tariffs on an additional $300 billion of Chinese goods, the PBoC allowed the Renminbi to depreciate past the closely-watched 7 level, but the depreciation was roughly in line with other Asian currencies. If anything, the Renminbi had, until recently, depreciated less than neighbouring currencies, which is something that the PBoC monitors closely when setting its daily fixing.

The bottom line? The data alone does not justify why China was designated a manipulator now, as opposed to May or October, when the next Treasury report is set to be published. The trade war continues to escalate and the timing is much more related to that, than what the data indicates. This is not over. Stay tuned.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox