The reflation trade and the US labour market – some hurdles to overcome

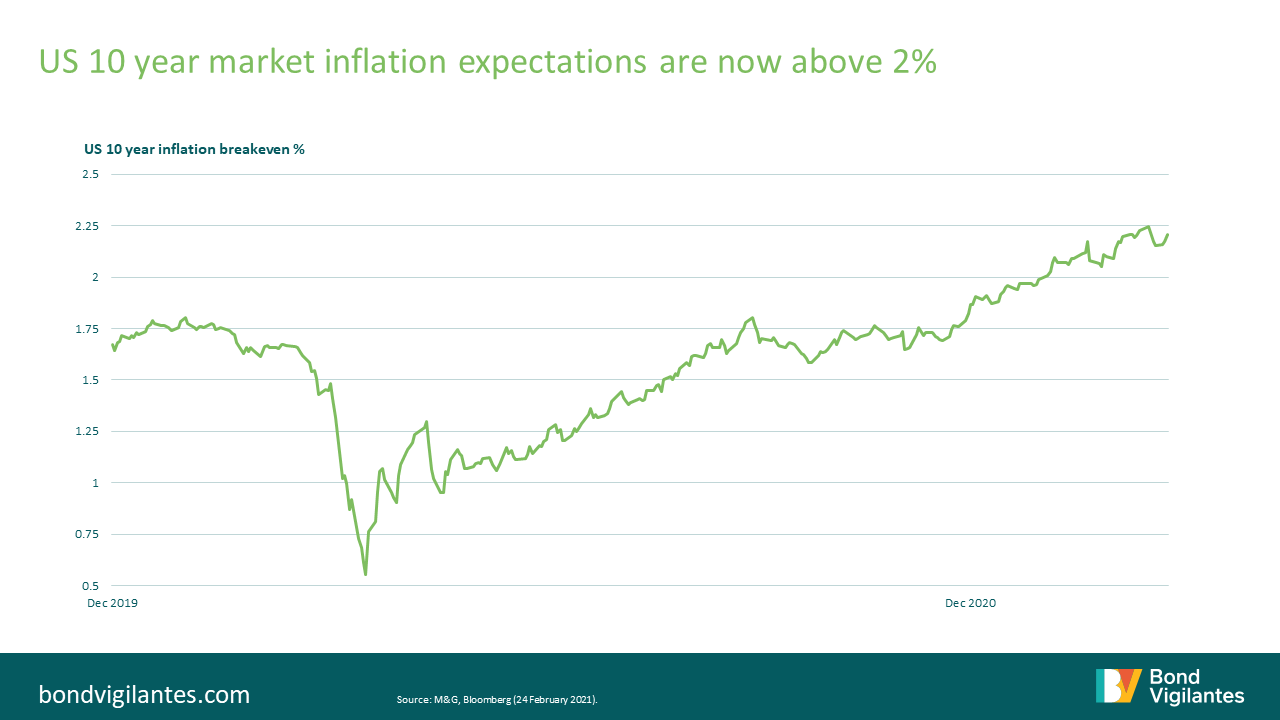

Summary: The reflation trade is the talk of the town globally, with the beginning of vaccine deployment in developed markets having created a small but shimmering light at the end of a dark Covid-19 tunnel. In the US, an unprecedented amount of proposed fiscal stimulus has spurred this further since the Democrats’ ‘Blue Sweep’ in January. US 10 year breakevens are currently pricing in above 2% inflation (see chart below) from their lows of 0.5% in March 2020 – but are these levels achievable after years of low inflation and, more importantly, can they be sustained?

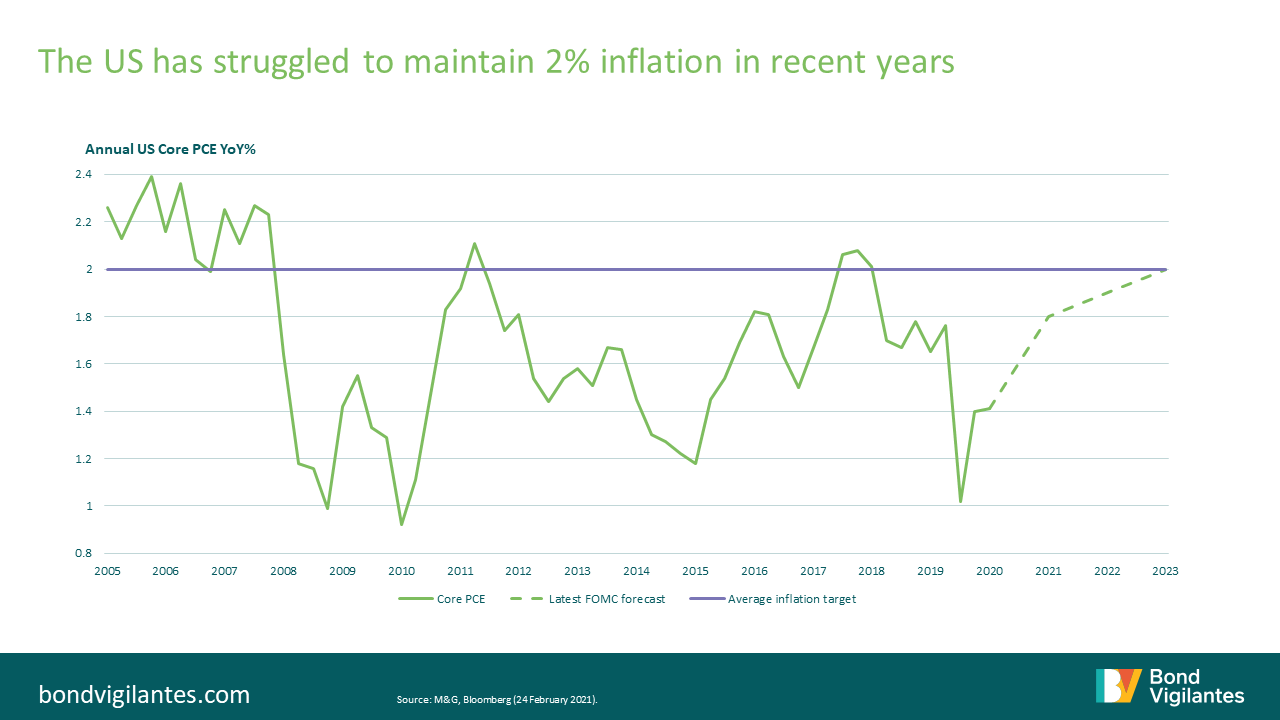

Economic theory dictates that, for inflation to be sustained near the 2% level, we need to see an economy with near-full employment levels. We nearly managed this in 2018 (see chart below), when core PCE inflation (YoY%) breached the 2% mark in the US, but this wasn’t sustained as the Fed tapered too early.

FOMC projections anticipate that Biden’s aggressive fiscal stimulus package will enable the economy to reach 2% PCE inflation by 2023. They also expect the US unemployment rate to have gone down to 3.7% by 2023, which we can assume would be near full employment (assuming 3-4% frictional unemployment). However, despite these projections having been revised to the upside since September, it seems labour markets may not be recovering as quickly as expected.

Hurdle 1: The US labour market

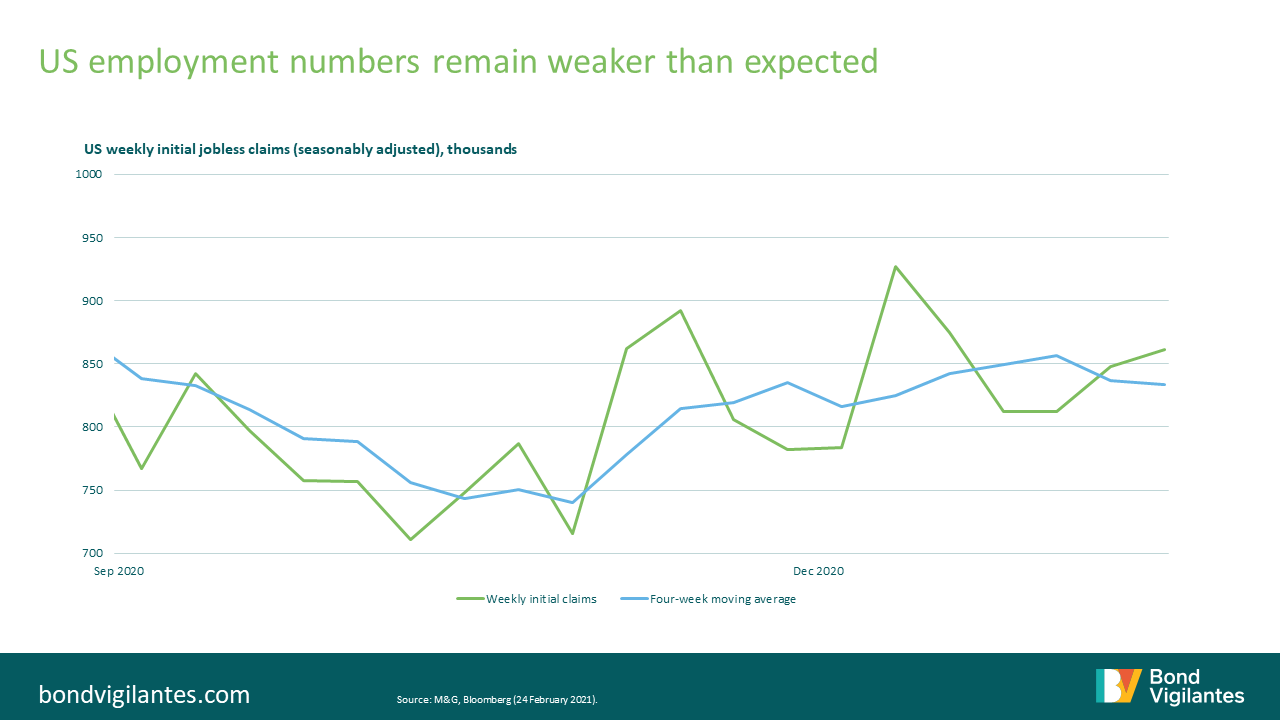

US initial jobless claims (released weekly, making it one of the timeliest indicators of the economy), indicate that current employment readings continue to be weaker than expected (see chart below). For the week of 13th February, initial jobless claims hit a four week high of 861k vs an expectation of 773k, with the previous week hitting 848k vs an expectation of 793k. The four-week average has been rangebound between 814k and 857k since December, raising questions over the current speed of the recovery of the labour market. It is also hard to quantify risks such as whether furloughed/laid-off workers will be able to retrain easily into new industries, and the risk of hysteresis, which indicates a more permanent change in the workforce as those unemployed for long periods of time lose skills and struggle to become employable, even after the end of recessions. This also raises the concern of inequality: how many permanent scars will remain in US labour markets after a year of increased unemployment and poverty, even if overall inflation data prints positively?

Hurdle 2: The Fed

Another key hurdle to the reflation trade will be the actions of the Fed. As the short end of the breakeven curve begins to price 5 year inflation near 2.5%, these moves may begin to plateau with focus shifting to real yields. Should the Fed continue to retain an exceptionally dovish stance, real yields will likely remain rangebound as reflation projections become fully priced in, but any hawkish whispers could push real yields higher. Another thing to consider is whether central banks will intervene to put a stop to rising nominal yields. Despite the current sell-off suggesting optimism in the recovery and inflation, it could also hinder the rebound by boosting the cost of financing the massive debt burdens built up globally during the pandemic.

Hurdle 3: Consumer spending

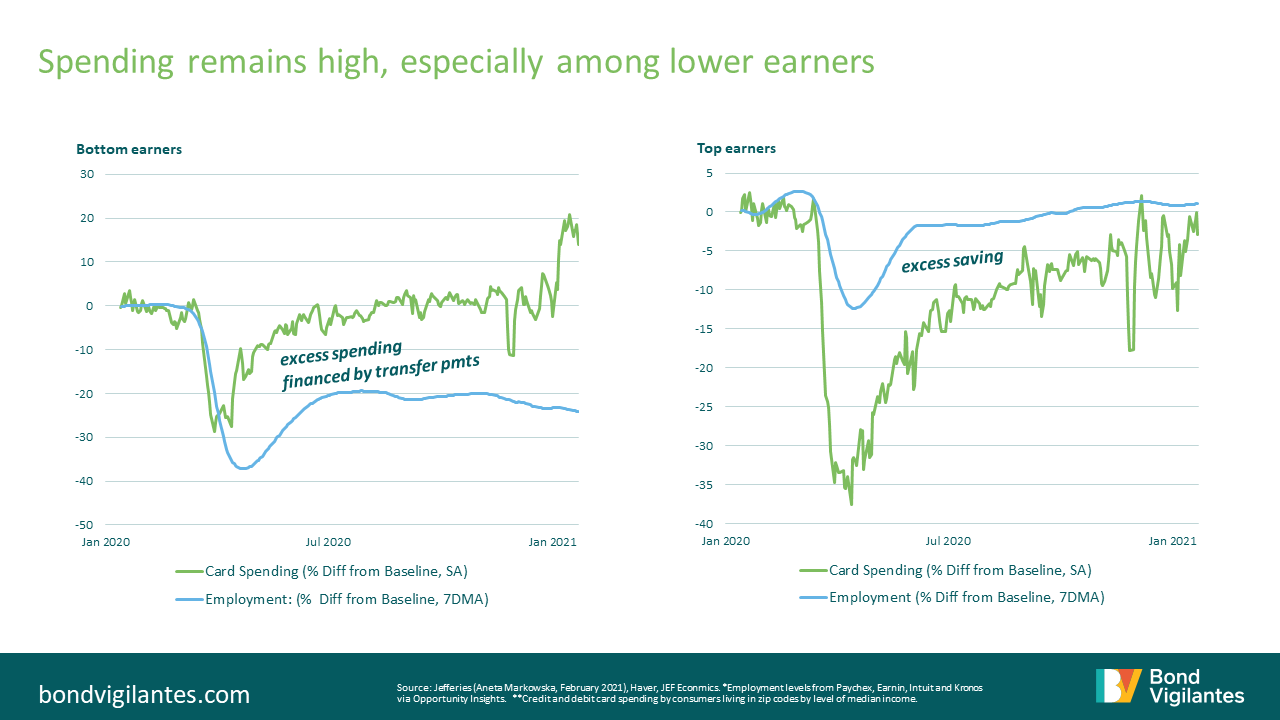

It is also important to question the effectiveness of the Democrats’ proposed $1.9 trillion of fiscal stimulus in the US, which will include $300 billion of stimulus cheques worth $1,400. Markets are expecting this package to help spur a consumption boom but, with high levels of savings building up in the US and globally, the question is whether these cheques and other benefits will be spent or saved. Looking at the charts below, it looks like the short answer is that the money will indeed be spent. Comparing employment and spending between different income brackets shows that, despite much higher levels of unemployment among the bottom earners in the US, transfer payments are currently being spent in the economy. This suggests that further fiscal stimulus cheques are likely also to be spent rather than saved by this demographic, helping to spur demand, consumption and thus growth and inflation.

The top income bracket seems to be where the pent up savings are. So, in the short term, growth should be driven by the spending of stimulus cheques but, in the mid term, by the higher earners deploying their savings once service sectors re-open. What will determine the timing of service sectors re-opening is undoubtedly vaccine deployment in the US. Therefore, if these fiscal packages are large enough to bridge the gap between spending by the bottom and top earners in the US, we could see a smooth consumption boom and closing of the output gap. This seems increasingly likely now that vaccination efforts are gathering pace in the US, helped by an already sophisticated flu-vaccine infrastructure, alongside the fact that the stimulus package has more than doubled from the original figure proposed of $934 billion. However, if these cheques run out before we get to the point that vaccine deployment has allowed service sectors to re-open, we may see some volatility in consumption trends. As mentioned, it is also important not to ignore unemployment numbers among the bottom earners, where a reversal in current hiring freezes will also need to be seen in order to generate a smooth transition and avoid an increase in inequality.

Inflation could still make a comeback

Despite these hurdles, inflationary forces that we are seeing in the market could be enough to offset these potential hinderances to the underlying inflation prints. Firstly, the recovery of unemployment numbers may not be as important as traditional economic theory dictates. The Phillips Curve relationship has arguably loosened significantly in recent decades, especially during periods of stagflation such as the 1970s and the booming 1990s. Inflation projections are also aided by very low starting points, with developed market inflation having printed below target for a number of years as a result of global trends such as technological advances and globalisation. It would take quite a large shock to the system to stall such trends – which a global pandemic undoubtedly offers. Talking of low starting points, we also saw numerous markets (Japan, for example) pricing in negative breakevens in the midst of the pandemic: this meant that, on a pure valuation basis, it became very cheap for investors to add inflation insurance into their funds.

We can also look at metrics such as the velocity of money. This hit record lows throughout 2020, offsetting inflationary pressure, but we are starting to see this trend reverse. Record levels of monetary policy intervention, coupled with record fiscal stimulus and pent up demand in the economy, could definitely spur this reversal further. Finally, it is important to realise that, for real yields and breakevens, it is not actual inflation that drives markets but expected inflation. We are likely to see a Fed that states that this year is ‘transitory’ and that underlying inflation prints are too noisy to take seriously for another couple of years. Consequently, if markets continue to be optimistic about vaccine efforts and positive economic data, a short-term output gap may not be cause for concern.

Conclusion

To conclude, we think it’s fair to say that the US reflation trade has got legs in the short term, largely thanks to unprecedented fiscal stimulus coupled with continued dovish central bank action. But, once the noise dies down and the facts become clearer, perhaps those legs aren’t as long as markets currently think. If the underlying inflation prints do materialise, how much will rely upon the speed of the labour market recovery, and will it be at the cost of higher inequality for those at the bottom of the income distribution?

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox