Auf Wiedersehen, “black zero”?

Summary: After 16 – yes, sixteen! – years, Chancellor Merkel’s term in office is eventually drawing to a close. Market participants seem to be paying surprisingly little attention to the upcoming federal elections taking place in Europe’s biggest economy in less than two weeks though. This could however backfire as, judging by the latest opinion polls, a change in German politics is looming ahead.

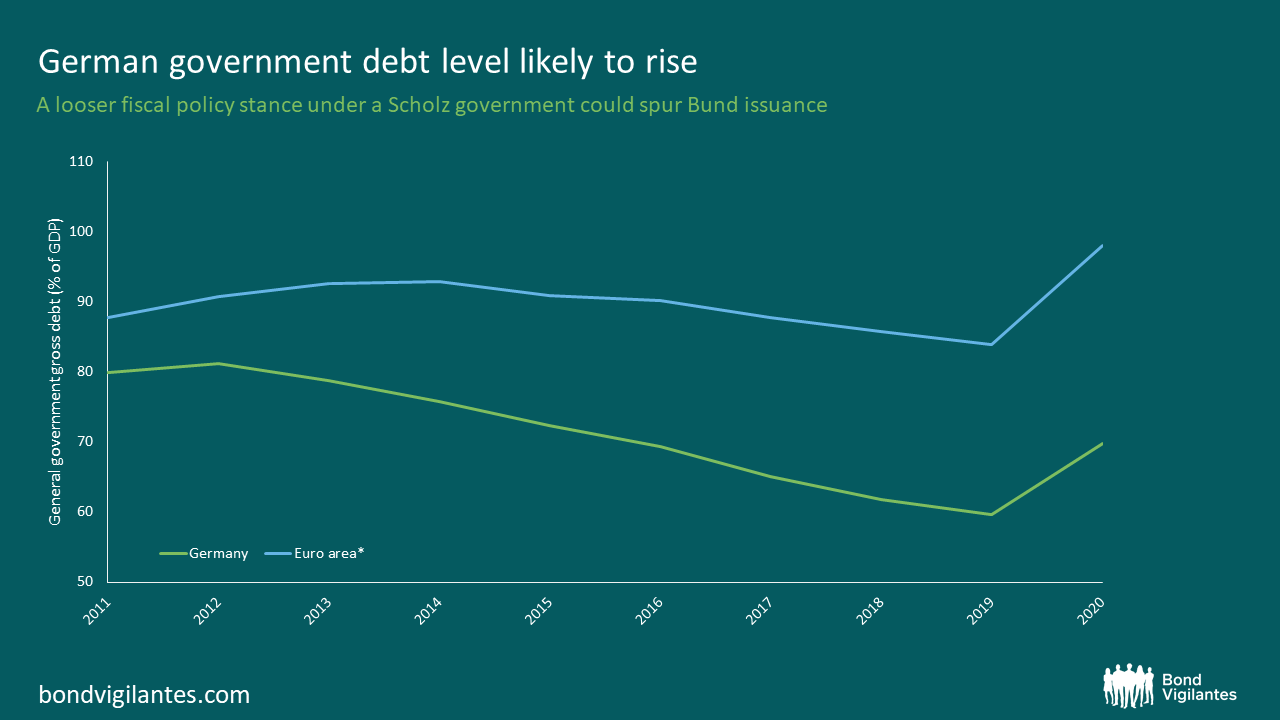

The days of the famous – or infamous, depending on who you ask – “Schwarze Null” (black zero, Germany’s commitment to balance its budget) might be numbered, just like those of Angela Merkel’s chancellorship. If Olaf Scholz, the Social Democratic Party’s candidate for Chancellor of Germany and current front-runner in opinion polls, replaces Angela Merkel after the elections, this would have a meaningful impact on Germany’s fiscal policy stance. The election manifesto of the Social Democrats leaves little doubt that Scholz’s party considers fiscal austerity entirely the wrong approach in the post-Covid environment. But would a Scholz government immediately end Germany’s love affair with austerity and bring the country’s public debt level of around 70% closer to the Euro area average of nearly 100%?

Source: M&G, Eurostat. *19 countries (from 2015).

Well, not so fast. The German constitution imposes strict rules in this regard, limiting annual federal net new debt issuance to a measly 0.35% of GDP. And a Scholz government wouldn’t have the necessary two-thirds majority in both chambers of parliament to get rid of the so-called “Schuldenbremse” (debt brake) altogether. But the German constitution leaves a bit of wiggle room to get around the 0.35% limit in the event of natural disasters or other extraordinary emergency situations. And I think it is fair to say that, within the German constitutional framework, the Social Democrats may try to exhaust all possibilities to raise debt levels to fund public spending. Bond investors should thus brace themselves for heightened levels of German government bond issuance, which may put upward pressure on Bund yields.

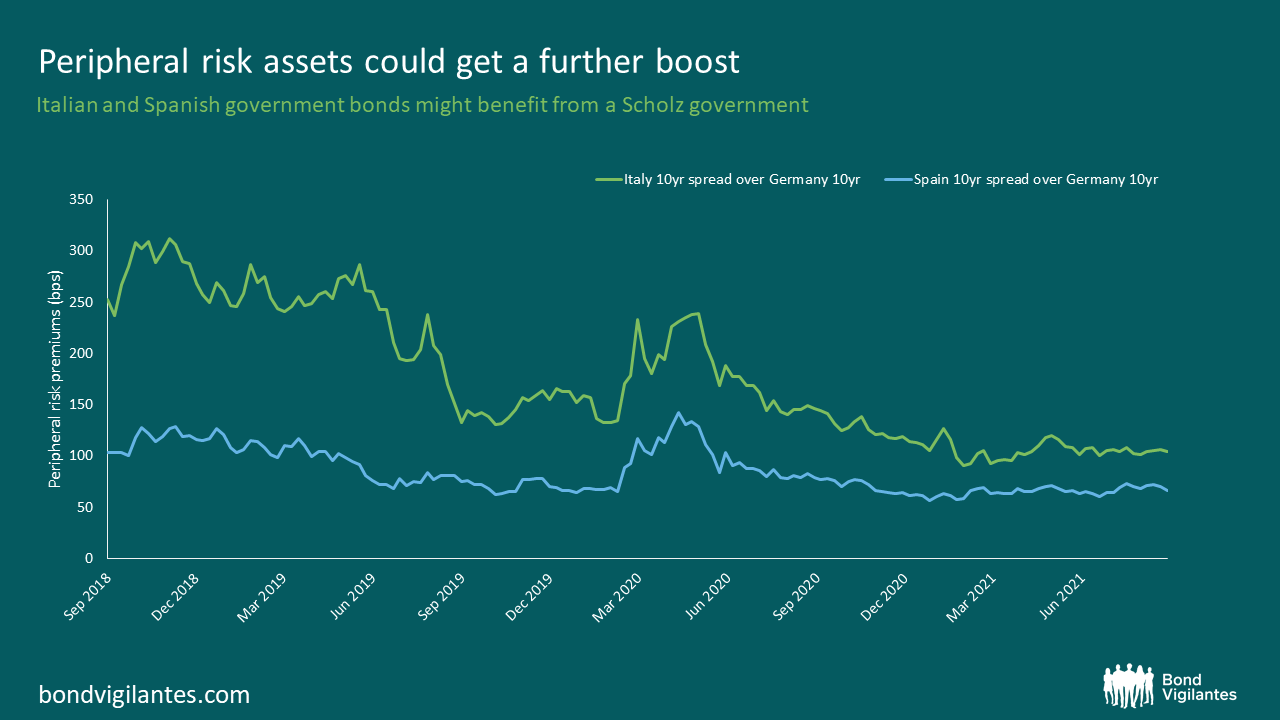

After softening Germany’s stance on domestic fiscal discipline, a Scholz government would likely be rather lenient towards public finances elsewhere in Europe too. We should also expect further steps towards European fiscal integration. The election manifesto of the Social Democrats downright swoons over the EU Recovery Fund, praising it as a seminal milestone towards European solidarity. Hence, a Scholz government would likely be very supportive of any future pan-European projects combining joint debt raising with public investments tilted towards structurally weak areas. This could give a further boost to peripheral European risk assets, such as Italian and Spanish government bonds.

Source: M&G, Bloomberg (9 September 2021).

It should be noted, however, that at current yield levels – at the 10-year point, Italian and Spanish government bonds are trading only 105 bps and 65 bps, respectively, wider than German Bunds – a large portion of the compression trade has already played out. Advances in European fiscal integration under a Scholz government might cause some further tightening but a complete disappearance of peripheral risk premiums, last seen before the Global Financial Crisis, is a highly unlikely scenario.

Another aspect that becomes abundantly clear in the election manifesto of the Social Democrats is the party’s strong commitment to sustainability goals, and climate neutrality in particular. In fact, the word “Klima” (climate) is mentioned a whopping 67 times in the text or, on average, once a page! Large-scale public investment programmes targeted at green infrastructure and technological innovation are likely to be launched in order to help promote the socio-ecological transformation of the German economy, especially if the Social Democrats form a coalition government involving the Green Party. Undoubtedly, such a profound government-backed push towards sustainability would produce winners and losers within corporate Germany. It is our job as active investors to assess which companies would be well-positioned to thrive in this rapidly shifting environment and which would struggle or might even be put out of business entirely.

German politics in general might lack the thrill and glamour present in other European countries. Under Angela Merkel, things have been steady as she goes for a very long time. But investors ignore the upcoming elections at their peril as material changes in fiscal policy, European integration and sustainable industry transformation may well be right around the corner.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox