Inflation Hedging for Long-Term Investors – the most important academic paper you will read this year

You would have to be living under a rock to not notice the increasing number of articles dedicated to the topic of inflation. The increase in inflationary articles has almost been as dramatic as the increase in inflation itself. Even 3 out of our last 4 blogs have been on inflation. Unsurprising really, seeing as we are bond investors. Looking elsewhere, the pundits have decided to focus on the idea of how an investor can protect a portfolio of assets from inflation. Having done a lot of research on the topic here on the M&G bond team, we would like to draw your attention to an IMF working paper entitled “Inflation Hedging for Long-Term Investors” which adds an interesting angle on the debate.

Alexander Attie and Shaun Roache tackled the subject of inflation hedging front-on, and discovered some surprising results in the process. Attie and Roache had a look at the asset classes that typically make up the core of long-term investor portfolios – cash, bonds, equities, property and commodities – and measured the sensitivity of asset class returns to inflation over a one-year horizon.

The authors found that “the ability of cash to hedge against inflation is heavily influenced by the prevailing monetary policy regime”. This is unsurprising given the success central banks have had in anchoring inflationary expectations since the 1980s. It tends to be the case that when inflationary pressures increase, the central bank will act by hiking up interest rates.

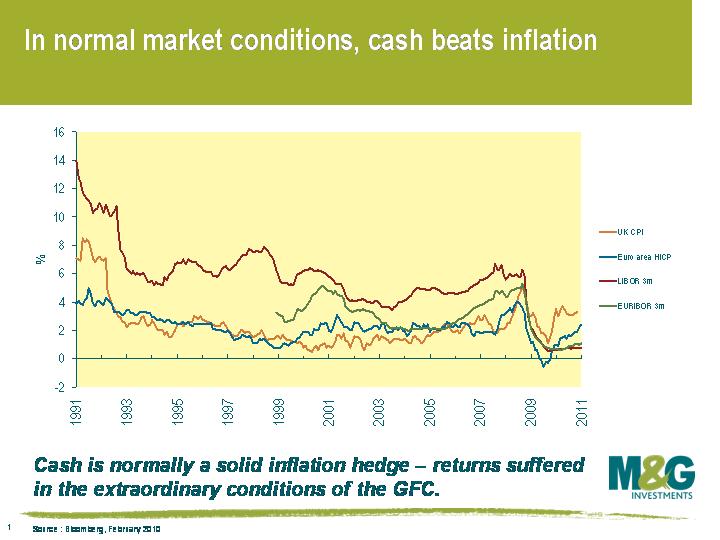

The most recent experience suggests that banks have been more willing than usual to keep rates on hold despite a pick-up in inflation. In the attached chart, we can see that inflation both in the UK and Europe has been running at a level that is higher than short term cash rates as measured by LIBOR and EURIBOR. This would indicate that whilst cash has traditionally been a partial hedge, since the financial crisis this has not been the case.

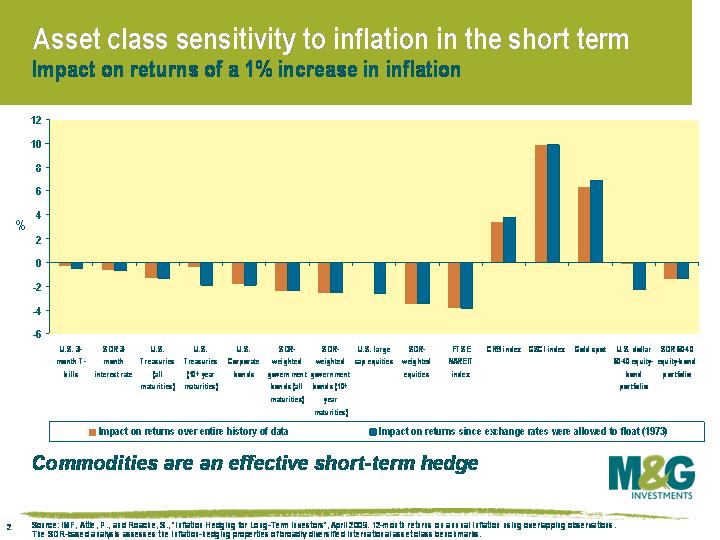

Both bonds and equities underperform if inflation increases. Looking at the analysis of returns since 1973, for a 1 percentage point increase in inflation over 12 months, the nominal annual return on a US Treasury bond benchmark fell by -1.33%. US corporate bonds fell by -1.91%. Equities experience even larger losses, with the same 1 percentage point increase in inflation leading to a fall in returns of the S&P 500 Index of -2.59%. Property, as measured by the FTSE NAREIT index does even worse, with returns falling by -3.48%.

Many investors point to the fact that commercial property rent reviews may be indexed to an inflationary measure, like RPI in the UK or HICP in Europe. However, because owners of property have generally levered their deposit through a loan, the cost of financing that loan will rise if interest rates increase to combat rising inflation. Pricing pressures on property arise when financing costs increase to material levels, causing both retail and commercial property prices to fall.

Commodities, as measured by the CRB Index, provide an effective hedge under this analysis with a 1 percentage point increase in the US CPI resulting in an increase of 3.77%. The gold spot price does particularly well, with the price increasing by 6.87%.

The attached chart shows the effects on nominal returns of various asset classes for a 1 percentage point increase in the rate of inflation over a one-year period. The results tend to be more conclusive for the post-Bretton Woods period since 1973. As you can see, all the major asset classes are assessed and all suffer after an increase in inflation, except commodities.

As Attie and Roache point out, “for long-term investors, a 12-month horizon is likely to be too short”. The lads use a long-run model to assess whether the returns exhibited in the short-run by asset classes are similar over a longer period (20 years).

In the attached chart, an elasticity of 1 indicates that the asset class provides a perfect hedge against inflation shocks and that real returns for the various indices remain unchanged.

The authors find that over a 20-year period, “cash returns do increase in response to an inflation shock, but the response is very gradual and less than full… Over time, cash begins to recover on an inflation-adjusted basis, but this process plays out over a very long period”. As discussed above, the move towards inflation targeting by central banks may mean that cash returns are more sensitive to inflation than has historically been the case.

Long-term treasury returns get whacked by inflation, as we would expect. Interestingly, these losses tend to peak around the 3 year mark of the 20-year time horizon with real return losses of nearly 2 percentage points. After this peak, yields and prices eventually stabilise and returns from treasuries improve due to higher running yields.

The authors find that the inflation shock is “likely to lead to higher long-term real yields, increasing the total return of bonds once the effects of the shock have been fully priced-in”. Additionally, the bond coupon is reinvested and bonds mature at higher yields. A bond investor doesn’t get fooled again after buying the bonds at low yields and inflation comes back.

With the risk of sounding like a one-eyed bond guy, I think I will directly quote Attie and Roache regarding equities:

“Equity returns decline in the months following an inflation shock and do not experience a meaningful recovery thereafter, leaving them as the worst performing asset class in our sample. After 1 year, equity returns are… 0.9% lower in real terms due to the inflation shock and the decline in returns bottoms out after about 3 years… [for a] 3% loss in real terms… Our findings are consistent with evidence from a range of earlier studies and add further weight to the evidence against the theoretical arguments for equities as a real asset class providing inflation protection when inflation is rising.”

The authors note that “this result does not imply that equities underperform inflation over the very long run; indeed there is ample evidence that equities outperform other traditional asset classes in real terms over long horizons”.

We think that what really matters for equity returns in an inflationary environment is the type of inflation an economy is facing. Is it demand-pull or cost-push inflation? In general, inflation is caused by demand-pull rather than cost-push factors. Demand-pull inflation is a sustained increase in the prices of goods and services resulting from high demand. No one is worried about economies overheating at the moment and thus demand-pull inflation. Arguably economies like Europe and the UK are facing cost-push inflation with the main cause being rising taxes and imported inflation. In an environment of cost-push inflation like the early 1970s, equity returns tend to suffer.

And whilst commodities do very well over the short-term, they tend to suffer over the long-term as the effects of inflation causes commodity prices to fall gradually over time. Commodity prices begin to fall, normally after a period of 2 years. Some reasons put forward for this relationship is that prices fall as supply comes on-stream, or demand for commodities is reduced because of higher interest rates or a business cycle slowdown.

Attie and Roache conclude that these findings have major implications for long-term investors, particularly if those investors have strong views about the path of inflation. In the words of the authors, “This is particularly true for “non-consensus” views in which investors may expect inflation surprises, whether positive or negative”.

Again, on equities I will leave it to the lads to express their conclusion:

Our results suggest that for investors who do not take tactical portfolio positions, the rationale for holding equities should be based on a very long-term horizon to ensure that the effects of inflation cycles average out. Investors with the scope to tilt their portfolios could underweight equities relative to their strategic benchmark in anticipation of higher inflation, but it may be more efficient to use other assets given their stronger and more consistent reactions”.

The paper is fairly damning for those who think they can inflation-hedge an investment portfolio: “among traditional asset classes, inflation hedges are imperfect at best and unlikely to work at worst”.

So what can investors do about protecting themselves from inflation?

Index-linked bonds (both government and corporate) are the only “traditional” asset class that will protect investors from inflation provided they hold the bond to maturity. As a buy and hold strategy, linkers work great. Because both the coupon payments and principal are adjusted in line with movements in a price index, an investor will be fully hedged against inflation (again – provided they hold the bond to maturity). Be warned – government linkers tend to be long duration securities, with the average UK and European linker having a duration of 15 and 8 years respectively. So investors have a lot of interest-rate risk in owning these bonds. Corporate linkers tend to have a shorter duration profile and it is important to have some short duration linkers in a portfolio as well. Don’t forget that there are also trading costs and there will be some price volatility as investors expectations for inflation change.

Inflation derivatives like swaps and options will also do the job, but it should be noted the markets for these derivatives are in infancy and considerably less liquid.

All in all, a very interesting paper that the pundits should try and get their heads around. It is one thing to look at a long-run chart of returns of the various asset classes through history, quite another to try and protect a portfolio of investments from future inflation.

Disclaimer – I don’t want to be accused of stealth marketing because that is not what the bondvigilantes blog is about, so here is a blog that Jim wrote about the launch of a couple of funds that aim at protecting investors from inflation. For what it is worth, we don’t think inflation is an issue over the medium term but think it will be sticky in 2011. Check out our views on inflation here.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

18 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox