Please note the content on this website is for Investment Professionals only and should be shared responsibly. No other persons should rely on the information contained within this website.

The start of each year is the time to reflect, look back and – importantly – try to focus on the year ahead. This is presumably a result of the welcome pause from work over the Christmas festivities, and the move towards longer days. This time of reflection is best typified by New Year’s resolutions. These behaviour changes generally involve giving something up!

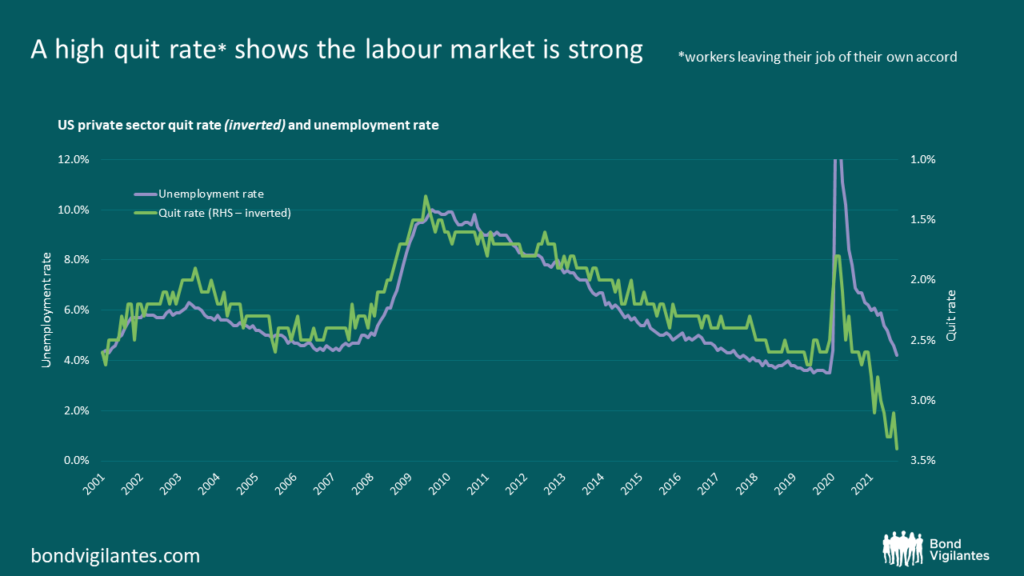

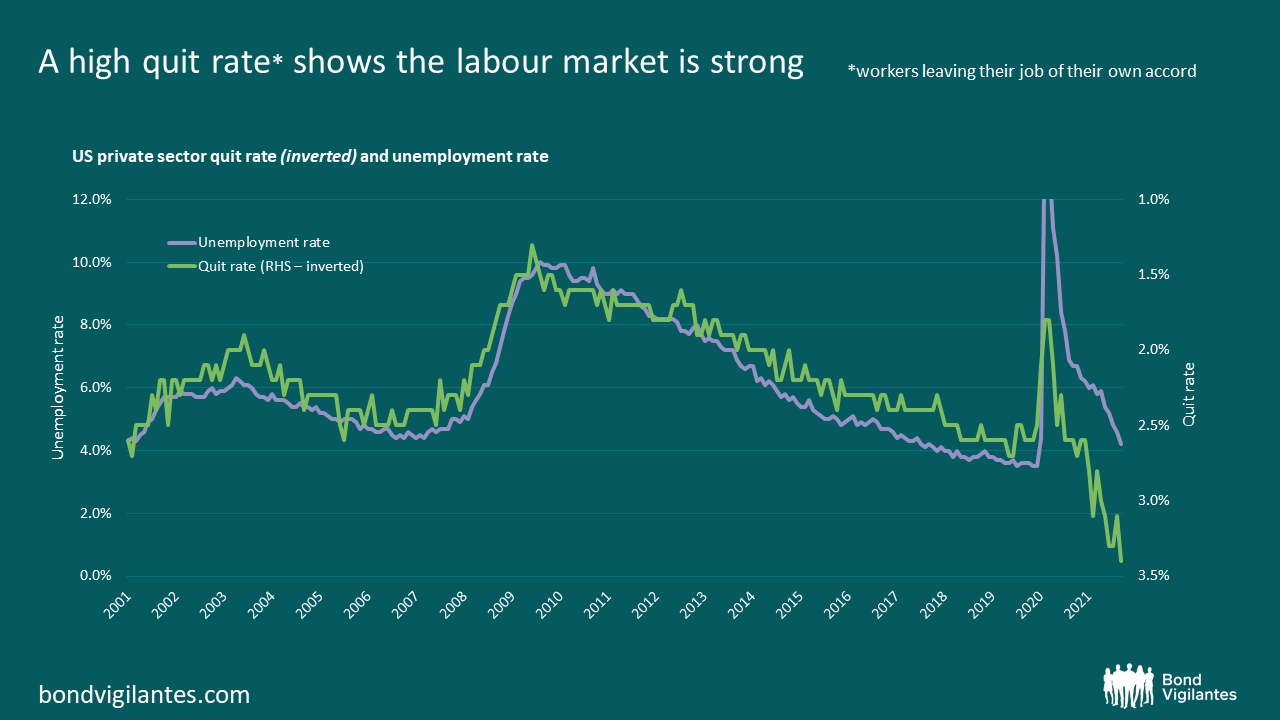

The quit rate in the US labour market – the rate at which workers give up their jobs – has been rising since well before the end of 2021. This can be seen in one of the first economic releases of 2022: the US quit rate for November was at a record 3.4% in the private sector. This jobs market indicator is something we have constantly focused on over the years.

The chart below shows the quit rate and the unemployment rate: as you would expect they are highly correlated. People quit their job when the labour market is strong and vice versa. The Fed is focused on the macro headline unemployment data. I think we should be taking more notice of the microeconomic “man on the street” data. The importance of understanding these numbers is that when we reach the objective of full employment then we will see a potentially highly inflationary bottleneck.

The quit rate is not just about people quitting jobs temporarily for a better job. It is also a function of people quitting for good, most notably retiring. This significant issue was raised by the Fed itself in looking at labour force participation. The combination of a high quit rate and depressed labour force participation due to retirement point towards the conclusion that we are closer to the goal of full employment than to the one set out by the Fed of unemployment returning to its pre-pandemic level.

Central banks themselves have one thing they all want to quit this year: Quantitative Easing. Their balance sheets have swollen on a diet of monetary excess. The first central bank to try to stop putting on the excess pounds is the Bank of England; the Fed and the ECB will be next. This is, however, likely to be only the first stage of the monetary diet: the next stage will be the new fad of Quantative Tightening.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

By

Guest contributor – Vladimir Jovkovic (Credit Analyst, M&G Credit Analysis team)

Share this highlighted text:

Get Bond Vigilantes updates straight to your inbox

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.