No major surprises in President Xi’s speech

Going into the Congress meeting, investors had been looking for signals to gauge if and how China’s zero covid policy will be relaxed, as well as whether there would be any near-term policy adjustments to the housing sector. Beyond the near term, investors were also focused on President’s Xi Work Report which set out the vision for 2035, as well as the composition of the upcoming Politburo to determine if execution and coordination could be improved with a new economic team in place.

President Xi’s opening speech at the CCP Congress meeting suggested that there will not likely be major policy changes in the near term. During the speech, President Xi stressed that the Party’s policy on COVID had helped save lives and yielded “significant positive results” in coordinating epidemic prevention and control.

On the economic front, the President called for “an upgrade of growth quality and reasonable growth of the economy”, which is a similar theme highlighted during the previous CCP Congress meeting. The pursuit of high-quality development and the need to ensure the resilience of its domestic economy amid growing geopolitical tensions dovetailed with the emphasis on core areas such as technology innovation and green development.

All in all, while there were no major surprises in President Xi’s speech, the continued importance assigned to economic development signals that the government will continue to balance policies that support growth with other social goals, such as improving the income distribution. We take comfort from the reaffirmation of growth as the party’s first priority and expect to see more measures to support its economic activity. The IMF has lowered its average growth forecast for China in 2023-25 to 4.5% from 5.2% 12 months ago. This is below the 4.7% growth rate needed to meet the aim of doubling GDP per capita by 2035 from 2020.

Notably, there appears to be less emphasis on supply-side reforms. The phrase “housing is for living” was also not mentioned during the speech (although the statement remained in the full work report). According to a Reuters count, in the full work report, the use of the word “reform” declined to 48 mentions from 68 five years ago. This may portend less disruptive regulatory and policy actions that have weighed on various sectors such as technology and property in recent years. If followed through, the shift towards policy pragmatism will help to reduce investment uncertainty caused by reform measures in the past five years.

What does this mean for China fixed income assets and the benchmark 10-year bond yield?

While we expect government policies to remain supportive of growth (especially as China’s Dynamic Zero-COVID strategy continues to constrain economic activity), there is a limitation to the role of monetary policy in achieving that. The monetary policy divergence in China versus the world has also come under increasing focus.

As such, we expect fiscal and credit policies to take dominance in terms of supporting growth, rather than to further monetary policy accommodation. Increased bond issuances by local governments to support growth could also lead to some supply pressure. Nevertheless, given the ample liquidity onshore, we expect periods of selling of government bonds to be limited.

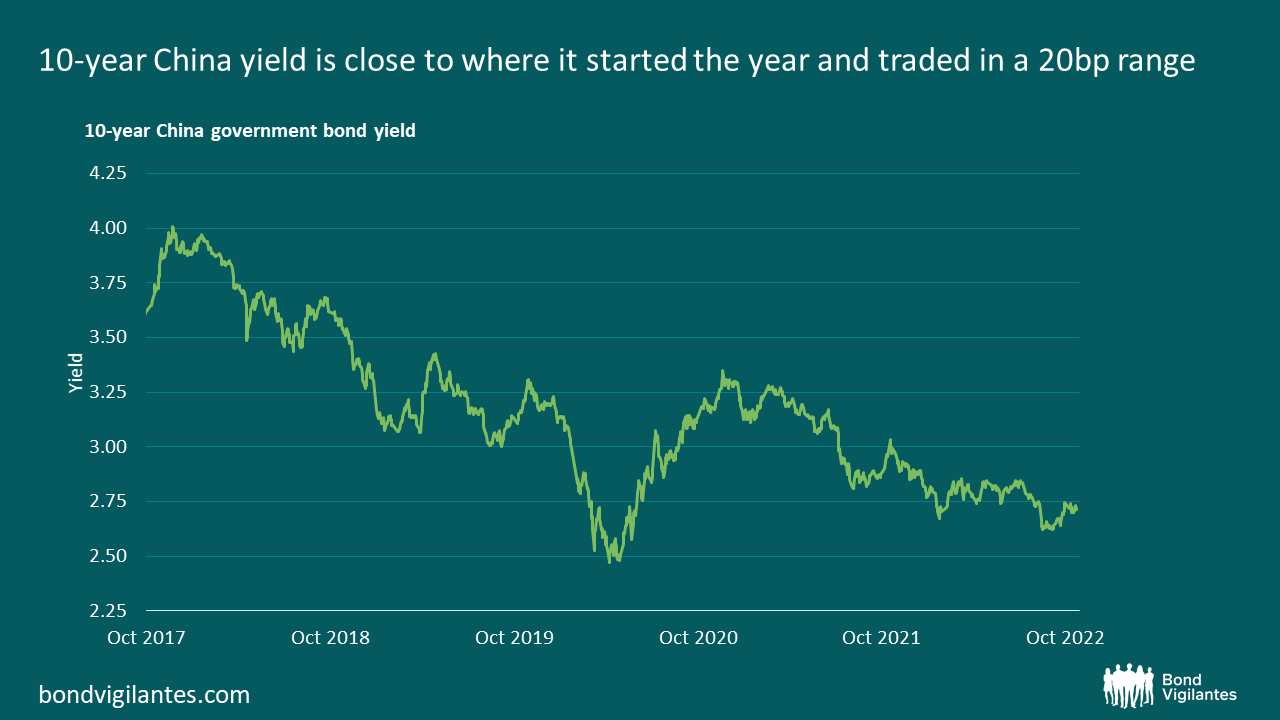

Overall, we think that for global investors, the case for allocating towards China government bonds has been strengthened this year. Globally, China government bonds have outperformed given the difficult environment for bonds. The 10-year China government bond is close to where it started the year at 2.75% and traded in a range of 20bps. In contrast 10-year US Treasury and 10-year German Bund have sold off by 250bps, and the sharp spike in volatility since July has led to declining liquidity. While the Chinese Yuan has depreciated against the US Dollar by around 11% year-to-date, it has outperformed other major currencies in this broad US Dollar move.

Source: M&G, Bloomberg (24 October 2022).

Nevertheless, we think the near term valuation for China government bonds is poor and we see room for the 10-year China government bond to go to 3%.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.