The World Cup 2022: how do the teams and previous hosts SCORE on ESG?

Qatar’s choice as a World Cup host has received a fair amount of criticism, on the back of allegations of mistreatment of foreign workers, the environmental impact of hosting a large scale sporting event in the Gulf (even in winter) and the country’s stance towards the LGBT local community and visiting fans.

How does Qatar compare to other emerging market countries?

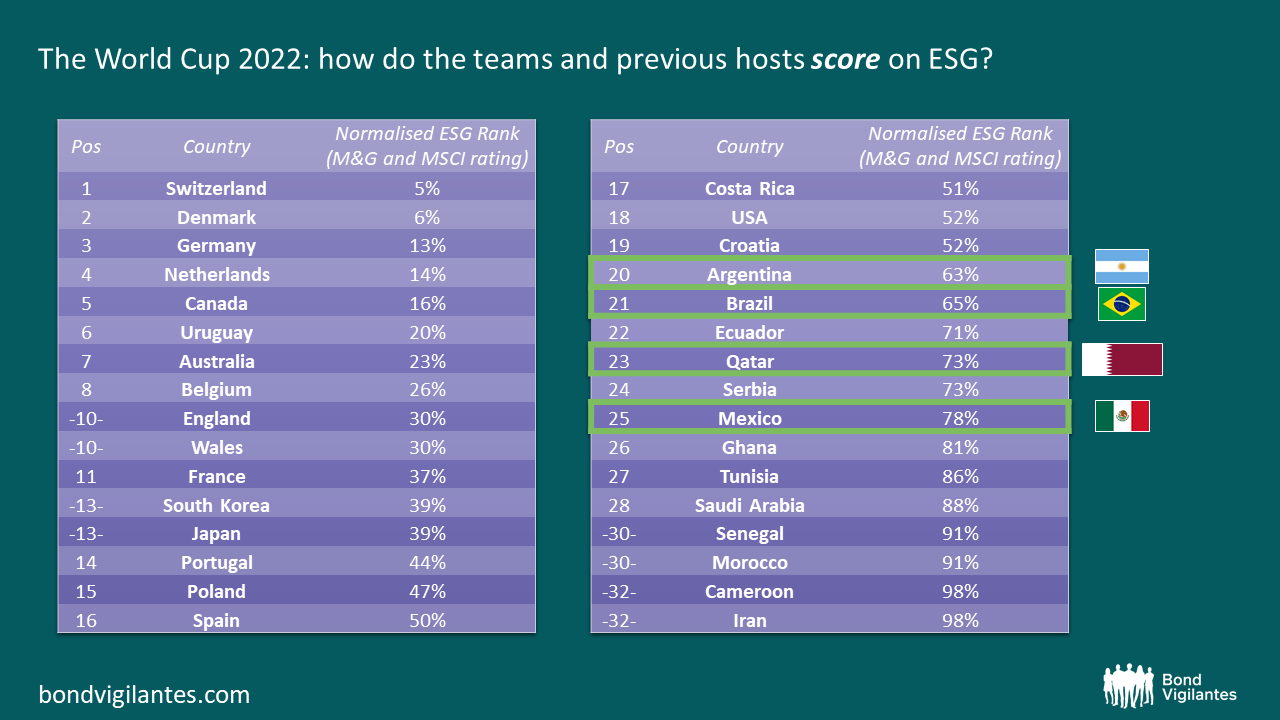

Following our tradition of World Cup themed blogs[1] we compared Qatar’s ESG scores with other 2022 World Cup participants based on our internal M&G sovereign scores, which we calculate based on a range of ESG and other risk factors, as well as MSCI’s.

Source: M&G, MSCI (November 2022). Normalised ESG rank is calculated as an equally-weighted average of normalised ESG scores based on M&G’s internal rating and MSCI data.

Most emerging market countries that we invest in typically have lower ESG scores than developed countries, as their institutions tend to be less robust and in some cases they may be more prone to higher environmental risks, to no fault of their own. Further, ESG scores tend to be correlated with a country’s income level.

Qatar’s ESG scores rank it 24th among the 32 teams playing in this year’s tournament. Its key ESG weaknesses, reflected in its sub-scores, relate to political rights, civil liberties, the treatment of migrant workers and environmental risks, much of which has dominated the build-up to the 22nd World Cup. However, Qatar’s ESG data also has several strengths relating to rule of law, solid performance in reducing poverty and income inequality, low energy security risk, and in terms of social stability.

How does Qatar compare to previous hosts?

It is worth noting, however, that Qatar’s overall ESG scores are not much weaker relative to other hosts. Qatar is not much behind Argentina (hosts in 1978) or Brazil (who hosted the tournament in 1950 and 2014). South Africa have not qualified this time around, but were the hosts in 2010 and have roughly the same ESG scores as Qatar. Russia, of course, has seen its ESG scores plummet from what were similar levels to the current hosts since its invasion of Ukraine.

Perhaps the most surprising is comparison with Mexico, which hosted the Cup in 1970 and 1986 and will co-host the next with the US and Canada in 2026. Mexico’s ESG scores are lower than Qatar’s. This is largely driven by weaker scores for corruption, rule of law and judiciary, stability and peace; although Mexico’s trend has been improving.

There are many valid criticisms of Qatar hosting the 2022 tournament, but when ESG scores are compared Qatar’s numbers are not much worse, and in some cases comparable, to other hosts. Based on this small sample of host countries, it does appear that the criticism towards Qatar’s host status is not fully backed by its overall ESG profile.

This is a good example of the grey areas we find in ESG scoring and data, and a reminder that a nuanced approach and close examination of the sub-factors that constitute E, S and G, is warranted. Whilst Qatar may have a stronger overall ESG score than some peers, some sub-scoring factors (e.g. workers’ rights) and occasionally non-ESG related factors may become more important for investor perception than the overall ESG score. Brazil experienced it in 2019 with a global outrage about the alarming rise in Amazon deforestation, despite a very decent overall ESG score compared to developing nations.

And finally…

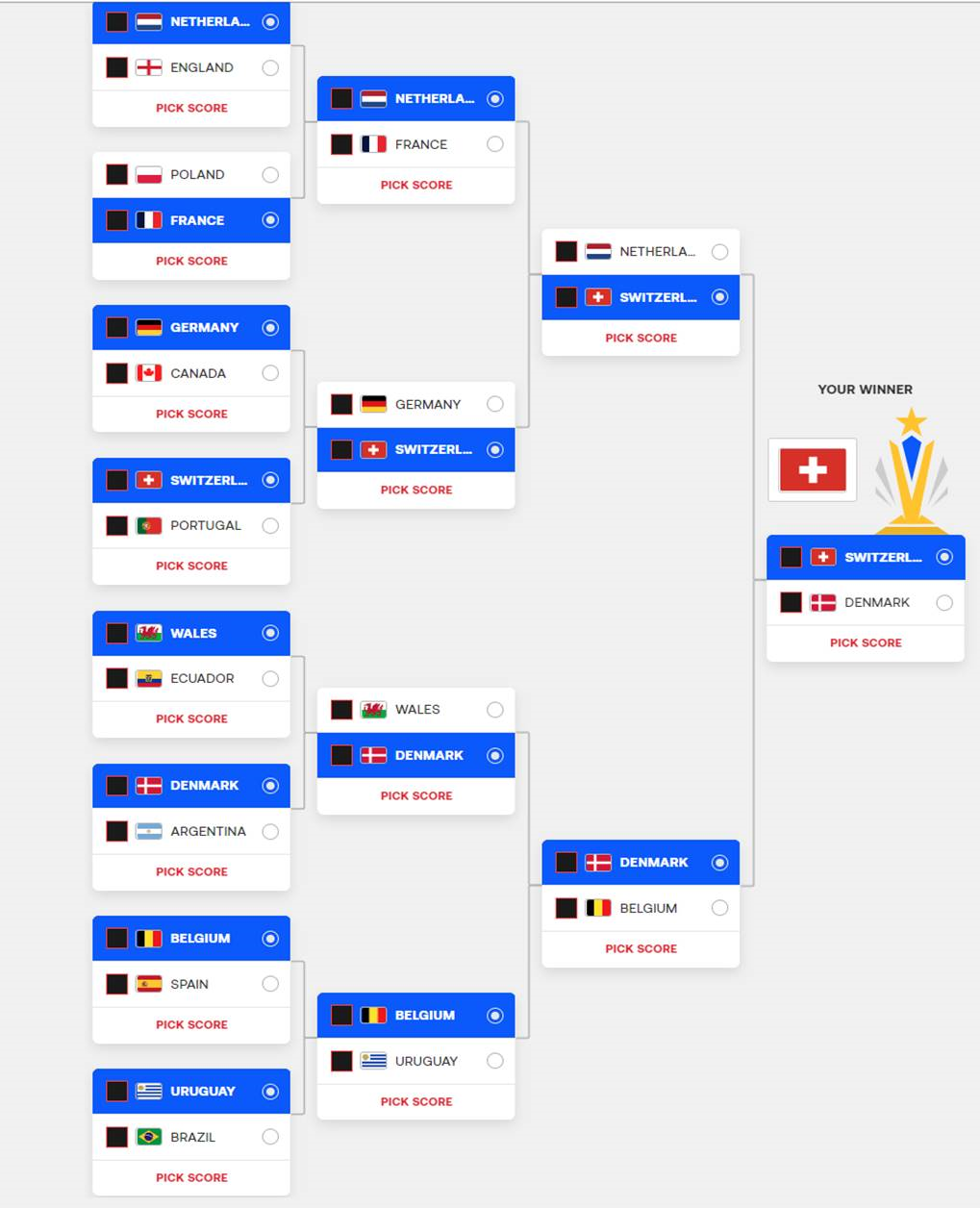

And finally, we checked to see who would win this World Cup if ESG scores decided matches. In such a final Switzerland would edge past Denmark to lift the cup!

[1] https://bondvigilantes.com/blog/2017/12/bvtv-world-cup-2018-the-dm-v-em-showdown/

https://bondvigilantes.com/blog/2014/04/world-cup-currency-trading-strategies-emerging-vs-developed-markets/

https://bondvigilantes.com/blog/2010/03/football-promotions-buffett-and-the-imf-world-cup/

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.