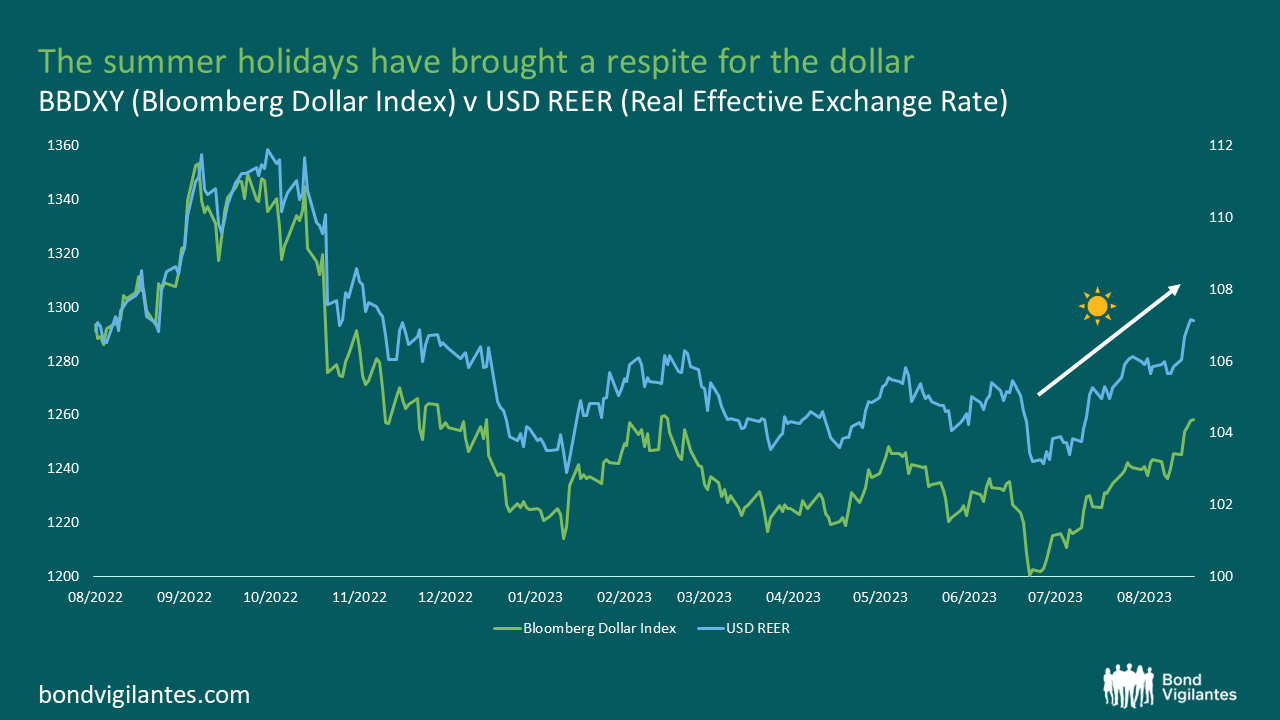

Summer’s over: Is the dollar rally packing up for school?

The kids may be back to school, but the summer weather seems to have saved itself for September here in the UK. A market that has stayed hot for a lot more of summer, however, is the US Dollar. The dollar has staged its strongest rally in over a year as the rhetoric of central banks needing to hold rates higher for longer has taken hold of markets.

Source: Bloomberg (September 2023)

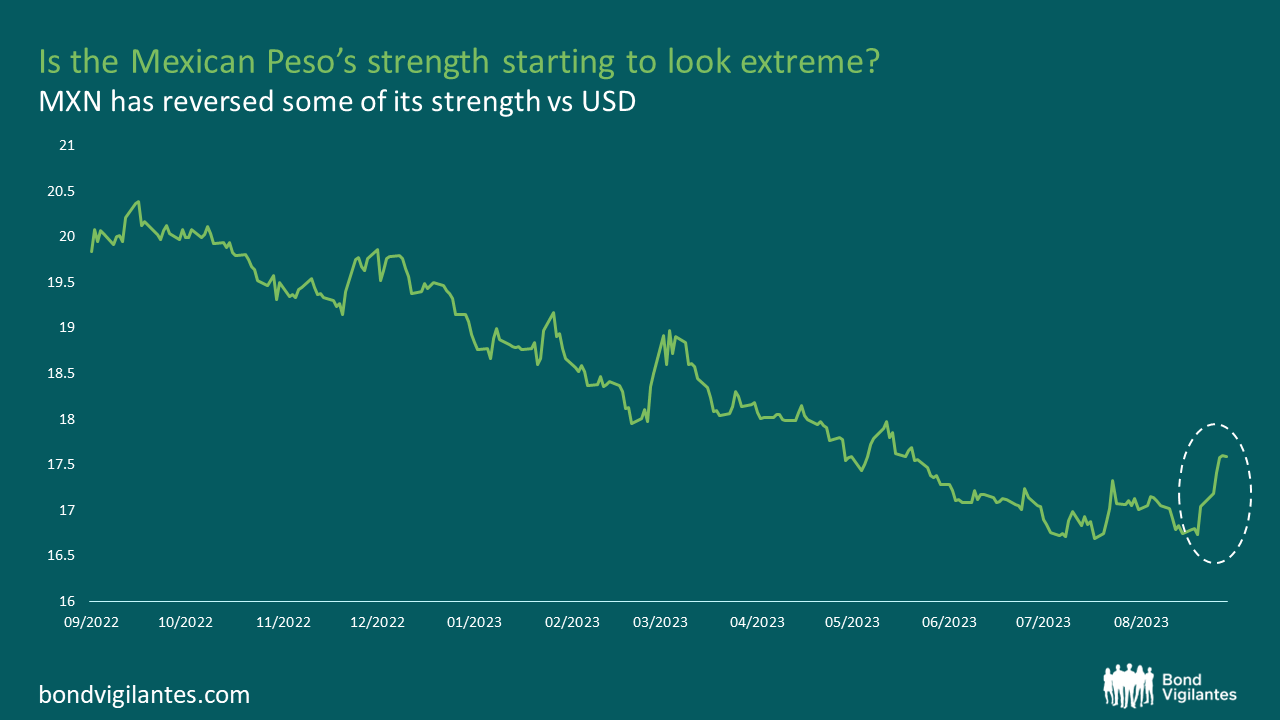

If this can be sustained, it will help the Fed’s fight against inflation by making imports cheaper in USD terms. But, it is a problem for others. A strong theme of 2023 has been the strength of carry trades – borrowing lower yielding currencies at low interest rates and investing into higher yielding currencies like the Mexican Peso (MXN) or the Brazilian Real (BRL). With emerging markets (EM) central banks having broadly hiked rates ahead of developed markets (widening yield differentials), and alongside low FX volatility, this backdrop has seen higher carry currencies perform exceptionally well, with total returns at 28.36% for the Mexican peso (MXN) and 18.27% for the Brazilian real (BRL). Even with rate differentials narrowing as developed markets (DM) central banks have caught up and hiked aggressively, low FX volatility has continued to drive up vol-adjusted carry.

Sources: LHS – BNP Paribas; RHS – Bloomberg (September 2023)

In recent weeks, however, some of these higher yielding currencies have seen their strength reverse sharply against both the dollar and the yen, with MXN in particular looking expensive on valuations. Coupled with heavy sales of the country’s local bonds, are we starting to see cracks in this year’s strongest currency trade?

Source: Bloomberg (September 2023)

Turning to the low yielders, not only have these currencies seen weakness from being on the borrowed-end of EM carry trades, those rate differential pressures have hit hard on those currencies whose central banks have continued easing – namely the Japanese yen (JPY) and the Chinese renminbi (CNY). As a result, their valuations have also become increasingly unappealing vs their DM counterparts, like the USD. On a trade-weighted basis, the JPY is now at its weakest this century. The Bank of Japan (BOJ) intervened almost a year ago in an attempt to prop up the currency, alongside some yield curve control (YCC) relaxation that was likely aimed at the currency – but valuations are even softer now.

Source: Citi, Bloomberg (September 2023)

Are we getting close to the point where the BOJ and People’s Bank of China (PBOC) may feel compelled to intervene? At the beginning of the week, BOJ Governor Ueda aired the possibility of an earlier policy shift than expected in Japan, perhaps in an effort to support the currency and stave off a similar intervention to last year. However, they have a difficult toss-up between the risk of higher yields adding increased pressure on their already-huge balance sheet (with a debt/GDP ratio of 250% and the central bank owning over half of outstanding Japanese Government Bonds (JGBs)), and continued JPY weakness. With some tightening of YCC policy in December of last year and July this year, 10 year JGB yields have crept up closer to the 1% boundary, but the BOJ have tried to slow the pace via loan operations rather than boosting the amount of their bond purchases in an effort to minimise the impact on the yen.

The PBOC have also thus far avoided using reserves, preferring to intervene via fixing (where they use fixing of the daily reference rate around which the CNY trades in a 2% band). They can also use other tools such as foreign-currency reserve ratios, or adjusting banks’ risk requirements on currency forward sales.

Should either/both of these central banks intervene via FX reserves, likely through selling US treasuries, the outlook for the USD is unclear. The sale of USD reserves to prop up their own currencies should naturally weaken the dollar and strengthen their own currencies, but this could also put more pressure on US treasury yields to rise even further. Given current dollar strength is being driven by ‘higher-for-longer’ rates in the US, further upward pressure on US yields could actually add to dollar strength. So, intervention to boost JPY and/or CNY could weaken other currencies that are heavily traded vs the dollar. If we have widening rate differentials once again between pairs such as USDEUR or USDGBP (that have both been strong this year and are heavily traded currency pairs), combined with markets continuing to delay their expectations of a Fed pivot in monetary policy, this could counterintuitively be a recipe for further dollar strength.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.