Has China become the new risk-free rate?

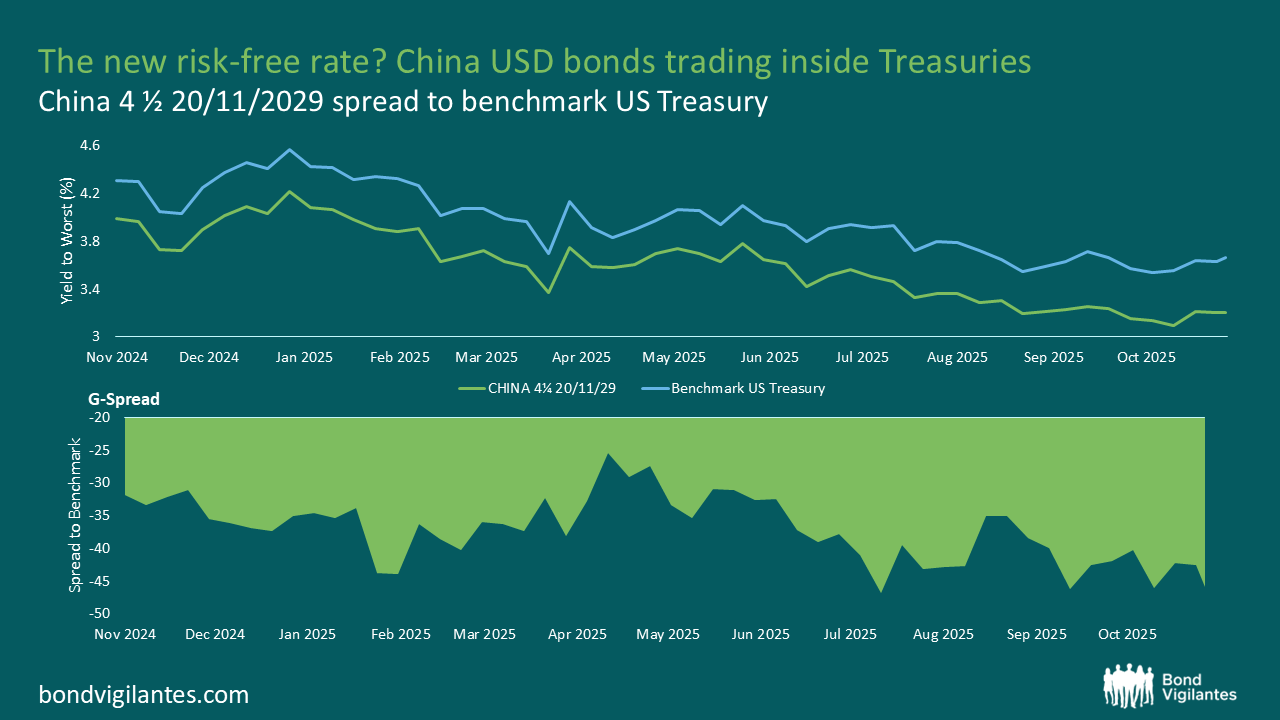

On 5th November China issued $4 billion worth of US dollar (USD)-denominated bonds split across two equal tranches. The orderbook was $161 billion at one point, but ended near $118 billion when final pricing was announced. The 3-year $2 billion tranche priced at US Treasury + 0bp (aka flat to UST) and the 5-year $2 billion tranche priced at US Treasury +2bp. The following morning, bonds traded up significantly and were quoted more than 30bp inside UST (specifically: China 28s -33.5bp | China 30s -37.5bp).

This is unusual. Looking at other high-credit quality sovereign issuers in US Dollar, South Korea 30s (AA-rated) trade at T+5bp, Abu Dhabi 30s (AA-rated) trade at T+10bp, or Qatar 30s (AA-rated) trade T+18bp. China is A+ rated so, on paper, its creditworthiness is assessed as weaker than South Korea or Qatar, and in this case AA-rated USA. So, what’s so special about China? “Has it become the new risk-free rate” asked one of my colleagues?

A natural tendency would be to think that China’s stability has become a new safe haven considering the year-to-date deterioration of the US institutions and creditworthiness. The new US administration, the weaker US dollar, the threat to Fed independence, the ongoing government shut-down and the constant tariff noise may be an easy cocktail of answers as to why China trades inside the US. However, the argument does not stand.

In November 2024, China issued $750 million of 5-year USD denominated bonds at T+3bp and they have been trading 30bp or more inside the Treasuries since then. Therefore, the perceived weakening US exceptionalism is hardly an explanation because mid-November last year very few investors would have anticipated the events that unfolded since the US Presidential election.

Source: Bloomberg (10 November 2025).

As often with bond trading, when the fundamental picture is failing to explain bond trends or moves, the technical picture may bring some colour.

Firstly, China has little external debt in USD so there is scarcity of bonds on offer. In contrast, Chinese banks are flush with US dollar deposits, so there is demand for USD assets. The alternatives to USD-denominated Chinese government bonds are not attractive because state-owned enterprise US dollar debt in China is rather expensive, and credit spreads in other IG names are close to their all-time tights. Secondly, there’s a (complex) tax rebate system that some onshore bank clients benefit from on bond income. The orderbook statistics showed that Asia accounted for 53% of last week’s book by geography type and banks for 33% by investor type. The supply/demand imbalance, coupled with the tax rebate means you get strong technicals for the newly issued dollar bonds. In addition, central banks, sovereign wealth funds and institutions – which tend to closely hold bonds – accounted for 26% of the orderbook. This should have helped secondary market trading. All of which led to robust performance and trading well inside the UST curve.

China recently unveiled plans to sell up to €4 billion of euro-denominated bonds later this month, but the above technical picture does not seem to apply to China’s Euro-denominated curve. China euro 5-year bonds, using CHINA 0 ¼ 11/25/30, have been trading between +20 and +40bps over the equivalent German Bund. China has not made it yet to the new risk-free rate.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.