Geopolitical tensions: Markets tend to price risk, not hope

Markets rarely move on hope alone. When uncertainty rises, they tend to price risk first, often before outcomes are clear. The renewed tensions in the Middle East are a reminder of that dynamic, bringing energy risk, inflation concerns and policy credibility back into focus.

In this blog we step back from forecasting events and instead look at how markets behaved during the last major rates shock. For structured credit investors, that period offers a useful guide to what matters when volatility returns.

Rates volatility returns and why structured credit held its ground

The conflict in the Middle East has reintroduced an increasingly familiar macro backdrop for markets. Energy risk premia, inflation uncertainty and renewed focus on central bank credibility have all resurfaced. While a ceasefire would clearly be positive, positioning portfolios around geopolitical developments? remains uncertain?. Experience suggests that bottom up analysis and stress testing fundamentals remain a more robust approach.

For structured credit investors, there are useful parallels with the period spanning 2022 and 2023. That episode combined aggressive monetary tightening with elevated inflation and widespread concerns around household balance sheets. Despite the severity of the shock, consumer asset backed securities, such as auto loans and credit card receivables, proved resilient compared with expectations at the time. As markets again debate the risk of renewed interest rate pressure, it is worth revisiting what that period taught us.

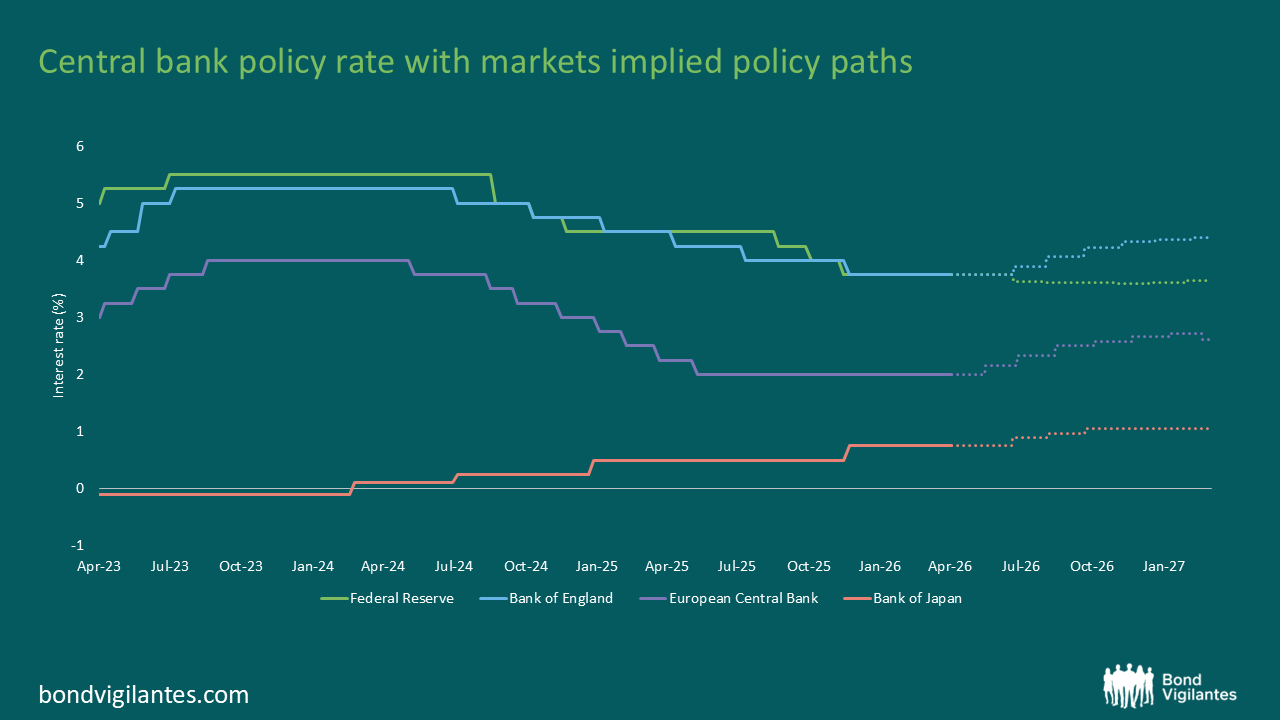

Source: Bloomberg, 30 April 2026

Why floating rate credit proved its worth when volatility hit

One of the defining features of 2022 and 2023 was the divergent experience between fixed rate and floating rate assets. Floating rate credit benefited from coupon resets that moved higher alongside policy rates, limiting drawdown risk and preserving income. Price sensitivity remained low, helping to dampen volatility relative to traditional corporate bonds.

Returns during the period were driven primarily by carry rather than capital gains, reducing reliance on spread compression or market timing. In practice, this allowed high quality ABS strategies to deliver more stable outcomes with lower correlation to government bonds and fixed rate credit.

When compared with similarly rated short dated corporate bond indices, senior ABS strategies delivered stronger cumulative returns with shallower drawdowns. This was evident across both euro and sterling share classes during the 2022 to 2023 stress period.

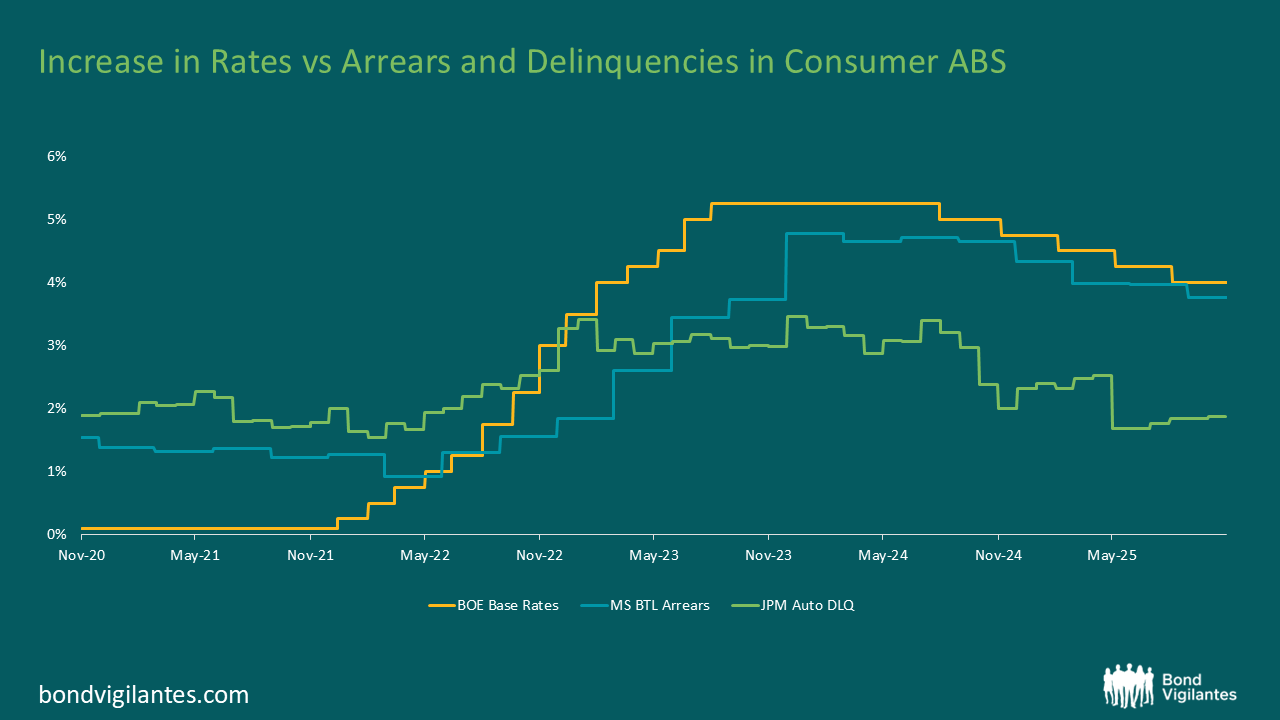

The consumer stress test that quietly worked

The rapid rise in rates placed real pressure on household cash flows. Debt servicing costs increased sharply and real incomes were squeezed. Despite this, consumer ABS fundamentals held up far better than many anticipated.

Arrears and delinquencies rose only modestly relative to the scale of the rate shock. Importantly, performance stabilised and improved as rate increases slowed, rather than continuing to deteriorate. Mortgage and auto loan pools both showed resilience through the peak of tightening.

This outcome reflected several structural factors. Household balance sheets entered the period in stronger shape, underwriting standards had incorporated meaningful rate stress tests, and borrowers prioritised debt repayment ahead of discretionary spending. These dynamics suggest that future rate shocks, if smaller and more gradual, may be more manageable, although outcomes will depend on the path of rates and household incomes.

Source: Morgan Stanley and Moody’s, JP Morgan UK Auto Delinquencies Index, October 2025

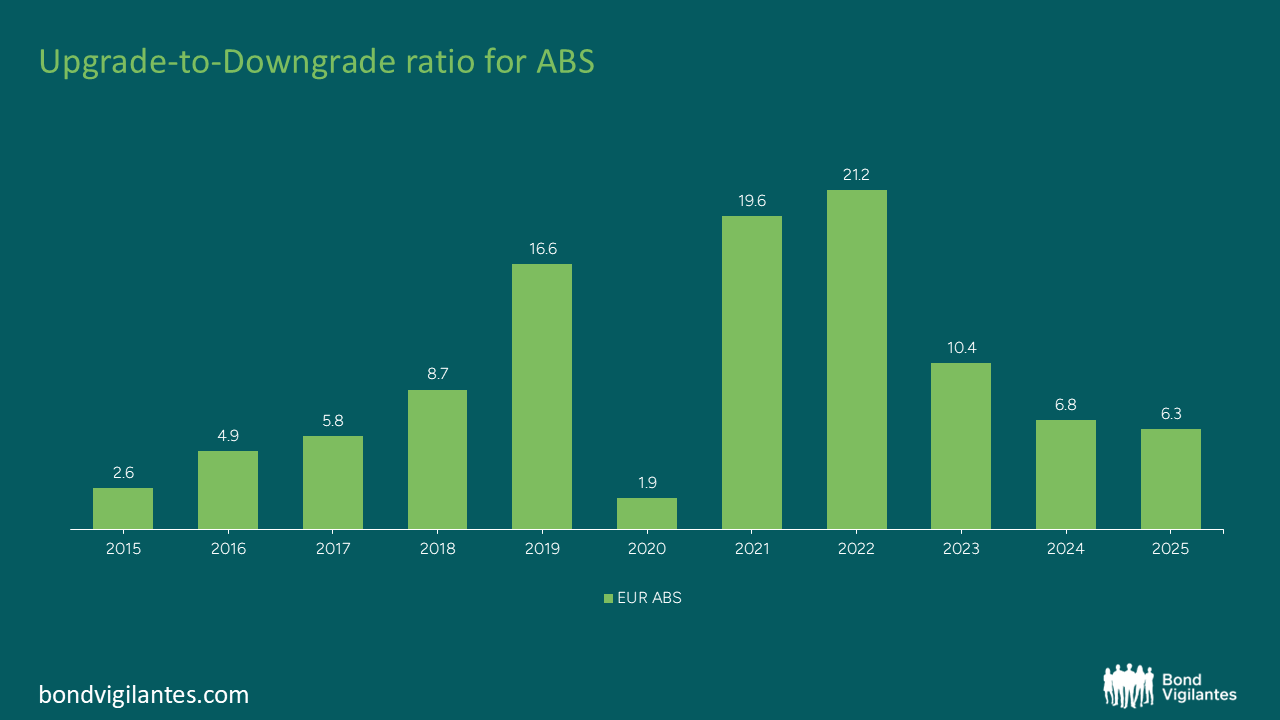

Ratings stability in uncertain environments

ABS has demonstrated a strong ratings profile, even through periods of macro stress. Over the past decade, rating upgrades have outpaced downgrades, including during the volatility of 2022 and 2023. The below chart shows this, by calculating the total number of upgrades versus the total number of downgrades over each year, with a result of 1.0 representing an equal number of each.

Bloomberg, Morgan Stanley, December 2025

ABS structures are designed to be resilient over time. As loans are repaid, risk naturally reduces, while built in protections help to shield investors from earnings volatility and balance sheet stress. This has been particularly valuable in an environment shaped by external shocks such as global conflict and trade disruptions.

The combination of resilient fundamentals and supportive ratings dynamics increases confidence that episodes of spread widening do not necessarily indicate structural deterioration and may, in some cases, create opportunities for disciplined investors.

When uncertainty rises, structure matters

Periods of geopolitical stress tend to push markets back to first principles. The experience of 2022 and 2023 showed that balance sheet strength, structural protections and income resilience are crucial for capital preservation. With inflation risks still an area of focus and ongoing debate around central bank credibility,, assets that reprice with rates and are underpinned by resilient consumer fundamentals may offer a more resilient profile.

Above all, in an uncertain rate and inflation regime, capital is protected not by forecasting skill but by structure, cash flow visibility and valuation discipline.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.