inflation

The inflation spark that could become a deflation shock?

By Robert Burrows

27 February 2026

As you may have already heard, I’m going to be leaving M&G later this year, after over 27 years here, most recently as the Chief Investment Officer for Fixed Income. I’m off to do a Master’s in the History of Art, and so I’ll be back in full-time education, studying modernism in Germany between the two World Wars. For those of you who have followed this blog over the years, you’ll know that this is a period we’ve looked at with great interest from an economic perspective, being the famous hyper-inflation years of the Weimar Republic. For me it will now be about the Bauhaus movement, Christopher Isherwood’s Berlin (think Cabaret), Fritz Lang’s Metropolis, and the paintings of Otto Dix.

I’ve loved my time in bond markets here at M&G, and I’d like to thank everyone I’ve worked with over the years for making it such a great place to work, and in particular Theo Zemek for hiring me in the first place. At M&G Theo launched the UK’s very first corporate bond mutual fund, and also challenged the idea that fixed income was a boring asset class. Hopefully over the 16 years since I started Bond Vigilantes we’ve helped to continually dispel that idea too, as we’ve written about the strains in the US mortgage market well ahead of the Global Financial Crisis, navigated through the Eurozone debt crisis, the pandemic and subsequent inflation boom, and the Trussonomics induced LDI problems. I hope you have also enjoyed the more light-hearted blogs. I enjoyed counting the shrinking number of monster feet in packets of Pickled Onion Monster Munch (others at nearby desks disagree) for perhaps the first commentary on the shrinkflation trend, and it was always the more esoteric academic research that interested me most – what, for example, was the impact of the dragon Smaug hoarding so much gold (the money supply) on the economy of Middle Earth in The Hobbit? Some blogs got me into trouble, and in a way gave me a foretaste of the new online culture that has developed in recent years. I’d suggest that you steer clear of writing about the economic impact of devolution, and especially avoid discussing a future without physical cash if you want a quiet life!

I would like to thank M&G for the entrepreneurial environment that allows us to just get on with producing the blog, without having to go through days of editing and sanitisation – the blogs genuinely come from the fund managers, analysts, dealers and specialists and reflect what they find interesting. Their grammatical incompetence did drive me up the wall sometimes, but we don’t pay them for that, thankfully. For me, when I consider my blog ‘highlights reel’ I would say that three come to mind. Firstly I was the first person to write about the possibility that the world’s central banks would eventually write-off their vast Quantitative Easing period holdings of government bonds rather than selling them back into the market. Secondly, one of our best-read blogs came out just as UK gilt yields starting spiking in the wake of the September 2022 ‘fiscal event’ that triggered issues in the LDI pension market. And thirdly, I can’t think of many places other than M&G that would have let me film myself drive around Tokyo in a Super Mario costume talking about the Japanese economy.

Finally a word on the Fixed Income team: it continues to go from strength to strength. Back in 1997 there were just 4 of us, in a corner of a small office in Minster Court in the City of London (a gothic building that stood in for Cruella de Vil’s house in the 101 Dalmations film). Today we have over £130 billion of bonds under management, a team of over 40 credit analysts, and bond investment teams not just in London, but in Chicago, Singapore and Paris. I’m sure that the team’s investment philosophy and expertise will see it continue to be incredibly successful in future and I’m looking forward to seeing how the exciting bench of talent we have here develops. Good luck everyone, and thanks for being part of an incredible investment culture at M&G, as well as being such good human beings too! I’d also like to say thank you to all the clients who have supported me and the team over my three decades here, as well as the journalists who have picked up on, and challenged, our ideas. The blog, of course, carries on!

I’ll be around for a while to come, if you want to buy me an alcohol-free pint of Guinness for example, or chat about the Tour de France, Nottingham Forest, or even bond markets. I’m going to end with my biggest passion, music, and give you the definitive list of the 5 best bands in the world ever. Bonds, football, bikes and bands – that’s what blogs were made for.

Love, Jim x

P.S. A couple of bonus blog. I can’t watch this one without shuddering at the stupidity and danger. Who built that thing? Why did they let us do it?

And here’s our biggest budget production, a documentary about the UK’s First World War debts, filmed at the Imperial War Museum in London.

Join Jim for his annual review of a busy 2023 for fixed income markets, which has put bonds back in fashion again. There is a lot to cover – central bank decisions, the credit environment and the everything rally into the end of the year. What can we expect for 2024? Jim looks at the prospect of government bond issuance, economic slowdowns and the busiest election year in history!

Uncle Jim’s World of Bonds is a regular podcast by Jim Leaviss, Chief Investment Officer Fixed Income at M&G Investments. According to Jim, there is nothing more fascinating than a fixed-income instrument. Nothing. Listen to Jim transport you to a world of convexity, basis points, covenants and debt-to-GDP.

There is nothing more fascinating than a fixed income instrument. Nothing. Listen to Jim transport you to a world of convexity, basis points, covenants and debt-to-gdp.

For professional investors only. No advice here. No mention of funds or products. Personal thoughts, not that of any employer.

Man I go on a bit. The stuff about The Pogues is at 38 minutes if you can’t face the rest.

In this week’s podcast episode, Jim dives into the dynamic world of finance, economics and trends that are shaping our financial future. From paying homage to the late Charlie Munger, Warren Buffett’s right-hand man and a titan of value investing, to dissecting the latest shifts in the bond market and the intriguing twists in Federal Reserve policies.

Uncle Jim’s World of Bonds is a regular podcast by Jim Leaviss, Chief Investment Officer Fixed Income at M&G Investments. According to Jim, there is nothing more fascinating than a fixed-income instrument. Nothing. Listen to Jim transport you to a world of convexity, basis points, covenants and debt-to-GDP.

There is nothing more fascinating than a fixed income instrument. Nothing. Listen to Jim transport you to a world of convexity, basis points, covenants and debt-to-gdp.

For professional investors only. No advice here. No mention of funds or products. Personal thoughts, not that of any employer.

Also Noah Smith on productivity

Dave Covey is M&G’s Head of Credit Research, and his specialist subject is financial credit. I caught up with him in this podcast, spending 30 minutes talking about the valuation of bank bonds (why are they so wide compared with traditional credit?). We also took a look at the ‘accidents’ in the financial system so far in 2023 (for example the Credit Suisse AT1 blow-up, and Silicon Valley Bank’s collapse).

I hope you enjoy listening to it.

There is nothing more fascinating than a fixed income instrument. Nothing. Listen to Jim transport you to a world of convexity, basis points, covenants and debt-to-gdp.

For professional investors only. No advice here. No mention of funds or products. Personal thoughts, not that of any employer.

Banking analyst Dave Covey talks CS AT1s, BoA’s US Treasury bond holdings, CRE lending and so much more.

We recently held our annual Bond Vigilantes Day, here at our offices in London. With fixed income markets trading at yields many investors may have never seen in their careers, the timing for the event was pretty interesting – although valuations have become even more compelling since (!).

You can watch the video presentations from our fixed income team below. I hope you find them useful.

Scroll down to find:

Loathe as I am to give the oxygen of publicity to rival podcasts talking about the bond markets, I can make an exception for those where I am the surprise guest. So I commend the A Long Time in Finance podcast run by Neil Collins and Jonathan Ford. Not only do they have high production values – they use microphones rather than shout at the iPhone like I do on Uncle Jim’s World of Bonds – but they also have cover art designed by Charles Peattie, who does the brilliant Alex cartoon in the Daily Telegraph.

Last week, Neil and I (Jonathan had overslept) talked about the horrors of the bond markets in recent months, and the problems around increasingly high levels of government borrowing. You can listen below.

The long view of finance, markets and money as seen by two veteran City editors, Neil Collins and Jonathan Ford, presented in partnership with The Library of Mistakes.

Hosted on Acast. See acast.com/privacy for more information.

It’s more than a decade since an American investor described the UK’s gilts market as resting “on a bed of nitroglycerine”. But with government bonds facing a plethora of troubles right now, from surging issuance driven both by current deficits and monetary policy, to persistent inflation, it’s time to turn again to UK investor and self styled “bond vigilante, Jim Leaviss of M&G to ask if there has ever been a worse time to hold a gilt.

Presented by Neil Collins, with the somewhat tardy participation of Jonathan Ford.

With Jim Leaviss.

Produced and edited by Nick Hilton for Podot.

In association with Briefcase.News

Hosted on Acast. See acast.com/privacy for more information.

Source: Spotify

And if you haven’t been listening to Uncle Jim’s World of Bonds, links to all episodes are on the Bond Vigilantes website: Uncle Jim’s World of Bonds

If you don’t get the books you want on Christmas Day, and you’ve already seen Love Actually, I recommend taking a listen to these ‘A Long Time in Finance’ podcasts by Jonathan Ford and Neil Collins.

The two I’ve linked below (Spotify, but also on Apple Podcasts) cover the history of the UK’s national debt, and are absolutely fascinating – although I would say that as I feature in the second episode, talking about the recent experiences of government borrowing in the QE era, and the prospects of lots more bond issuance in the years to come, on top of QT, Quantitative Tightening, where the central banks start selling their QE bonds back to the market.

I also enjoyed their podcasts on the collapse of Northern Rock. Give them a listen.

Part One

Part Two

I chatted with Alan Blinder last week about his brilliant new book on US economic history. Alan was Vice Chair of the Federal Reserve from 1994 to 1996, and also served on Bill Clinton’s Council of Economic Advisers, where he faced off against ‘real’ bond vigilantes. He’s now an economics professor at Princeton University. In our interview we discussed the developments in US economic policy from JFK’s ‘New Economics’, through monetarism and Volker, and to QE and the present day. I wholeheartedly recommend the book to anyone at all interested in economic history – this is a ‘must read’ for bond investors.

I’ve not written a blog for ages, but since we’ve just relaunched the Bond Vigilantes website with a lovely new look and feel, I can’t resist. Also there’s lots of stuff going on, including a really important bond market dynamic that I want to discuss here.

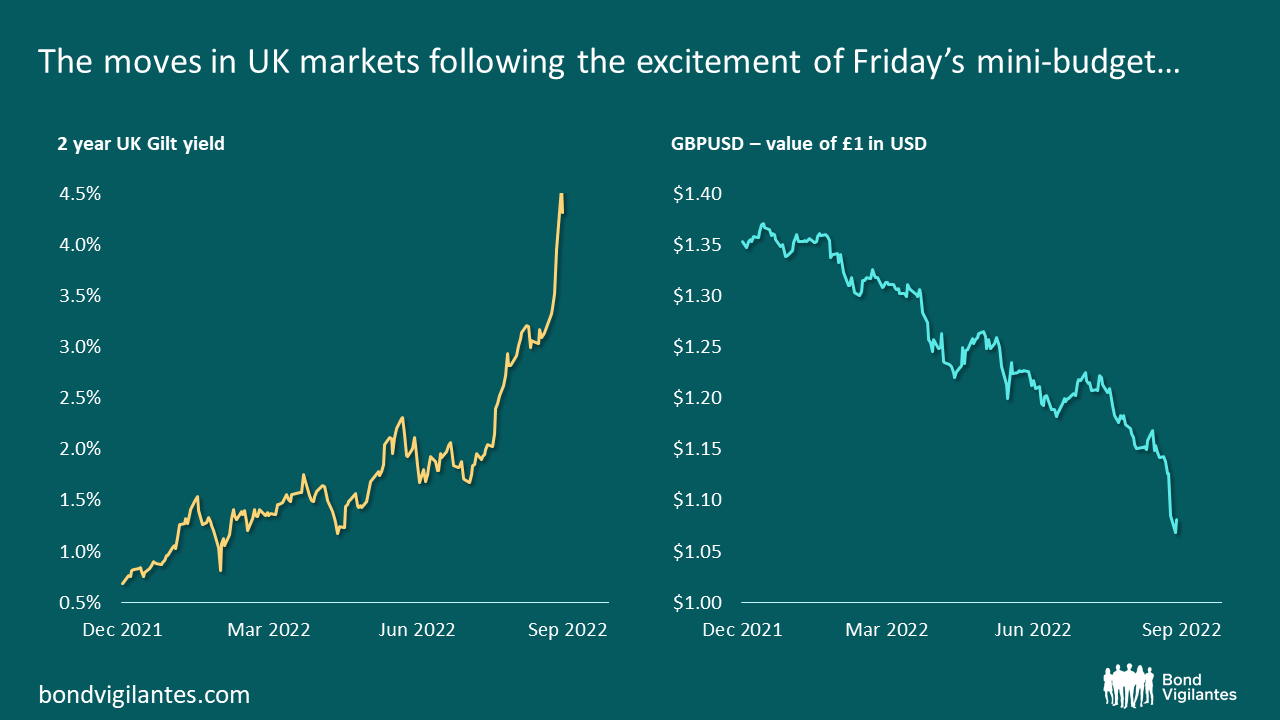

In all the excitement about last Friday’s mini-Budget sending sterling down to a record low against the US dollar, and sending gilt yields rocketing (2 year gilt yields rose by 1% over two days), there’s a dangerous technical factor lurking in UK bond markets that we mustn’t ignore. Toby Nangle, formerly a multi-asset fund manager, identified it in an excellent Financial Times article in July this year.

The piece points out that there are £1.5 trillion of assets held by UK pensions that have been hedged in so-called LDI trades. LDI (Liability Driven Investment) helps to match pension funds’ liabilities (future payments to pensioners) with the schemes’ assets. In a simple model this matching could be done by buying gilts of similar durations to the liabilities – if you owe your retired employees a collective £1 million in 2046, then you could buy a gilt maturing in that year. Or if you buy a quality corporate bond with a higher yield (a lower price) you can assign less capital to that liability, and use the extra cash to invest in a growth asset like equity, property, or private assets. Going further, you could use interest rate swaps or inflation swaps to match your duration liabilities. This means that you only have to put up some initial margin for the trade, and pay or receive collateral as market yields change (think of it like a contract for difference on a yield). If yields fall you would receive margin, and if yields rise the pension fund must pay margin to the counterparty. Using swaps gives the pension scheme far more capital to assign to those more interesting asset classes with high potential returns rather than having it tied up in boring gilts.

As Toby points out, the rise in gilt yields over the past year or so has been beneficial for many underfunded pension schemes – the value of future liabilities has fallen, so underfunded schemes become less underfunded. But a sudden rise in gilts has significant implications for pension funds using swaps to hedge liabilities. Collateral calls for margin payments will be large given the scale of the move in long dated bond yields, so this means that many schemes may have to raise cash by selling physical assets elsewhere in their portfolios – and in the dash for higher yields and higher returns, some of these will be in less liquid asset classes, perhaps leading to spread widening and discounts from expected value on sale. To quote Toby, ‘while rising yields are good news for pension scheme funding levels, they look a likely catalyst for a further liquidation of risky assets’.

Whilst this is a dynamic specific to pension funds using swaps, there’s a wider collateral implication from the recent turmoil in UK assets – and I’ve no real idea of its scale. Most UK based investors, and especially bond investors, buy overseas assets and hedge away the currency risk. The sterling corporate bond market has shrunk dramatically relative to other global capital markets, thanks mainly to the continued growth of the euro-denominated credit markets over the past years, and many issuers no longer borrow in pounds. UK corporate bond investors will therefore routinely look globally for the most attractive credit yields in either euros or dollars once hedging costs or gains are considered. Like interest rate and inflation swaps though, hedging is done via the use of derivatives – often foreign exchange forward contracts.

As an example, I might buy a bond issued in euros by Telefonica. To eliminate the risk that the euro falls in value and thus wipes out the additional return I anticipated, or more, I sell euros of a similar value to the bond I bought in the forward FX market, and buy sterling. Fund investors are therefore exposed only to the pound rather than to FX movements. Like other derivatives though, changes in price of the underlying asset lead to collateral movements. Given the 20% fall in the pound against the US dollar this year, and the recent sharp falls in the past week, if you had bought a dollar bond and hedged it, the dollars that you have effectively sold ‘short’ against sterling as the hedge have rallied, and the counterparty to the FX hedge will call for a collateral payment. Whilst most funds will hold some cash and extremely liquid government bonds against such moves, the size of the recent turmoil probably means that many investors will be having to liquidate credit and other less liquid assets in order to meet these collateral calls.

Whilst inflation, central banks, and *cough* government fiscal decisions will determine the overall direction of bond yields over coming months, don’t discount the technical dynamics too. The dash for collateral could be a big factor in the short term for the UK.

With COP26 underway in Glasgow, I caught up on Friday with Fund Manager Randeep Somel who works on climate solutions strategies and has been following the conference. I asked him what progress is being made and what the implications might be for markets. How much debt will governments need to issue to achieve their targets and could the trillions of green investment needed lead to Greenflation in an already inflationary economy? And could we see a market-based solution to emissions in the form of a global carbon taxation framework? We discussed whether COP26 has been a success, the roles of the US, China and Russia and the biggest challenges that remain.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.