Are consumers running out of steam?

Consumption is a major driver of the US economy, accounting for about 70% of real GDP. Today, consumer spending has become even more crucial, as it is nearly the sole factor behind recent economic growth in the US. Recent macroeconomic data indicates that most areas outside of consumption are unlikely to rebound in the near future, placing even greater pressure on consumer spending to keep the economy afloat.

Given this context, investors are now faced with a critical question: how long can consumers continue to sustain economic growth? Are they still in a strong position, or are they beginning to run out of steam, thereby increasing the risk of a slowdown?

To answer this question, we need to examine where consumers obtain the money they spend. There are three main sources:

1) Income: This is the money received from employment and is arguably the most sustainable source of spending. The post-COVID economic boom has been largely supported by income rather than borrowing, which partially explains why economies have been more resilient. Although income growth has been remarkably strong in recent years, it is now declining sharply and is likely to return to pre-COVID levels relatively soon due to the softening labour market. Consequently, income growth may soon be insufficient to maintain elevated levels of consumption and economic growth.

Source: Bloomberg, Atlanta Fed, 31 January 2025. Ticker: WGTROVER Index

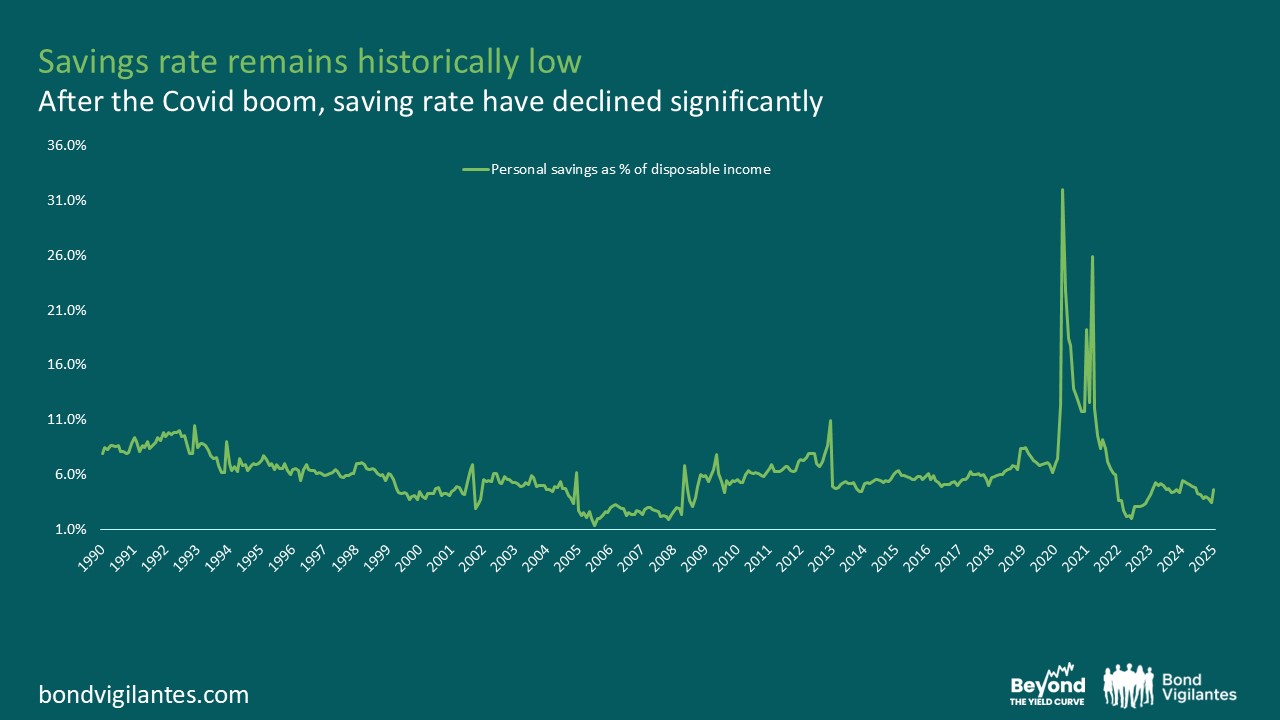

2) Savings: Savings provide a buffer that allows consumers to sustain their spending. The massive injection of liquidity during the COVID period, coupled with the inability to spend due to restrictions, resulted in a significant increase in the saving rate. However, as restrictions were lifted and economies returned to normal, the excess savings accumulated during COVID have been depleted, and the saving rate is currently near all-time lows. This suggests there is very limited room to sustain future spending through savings.

Source: Bloomberg, 31 January 2025. Ticker: PIDSDPS Index

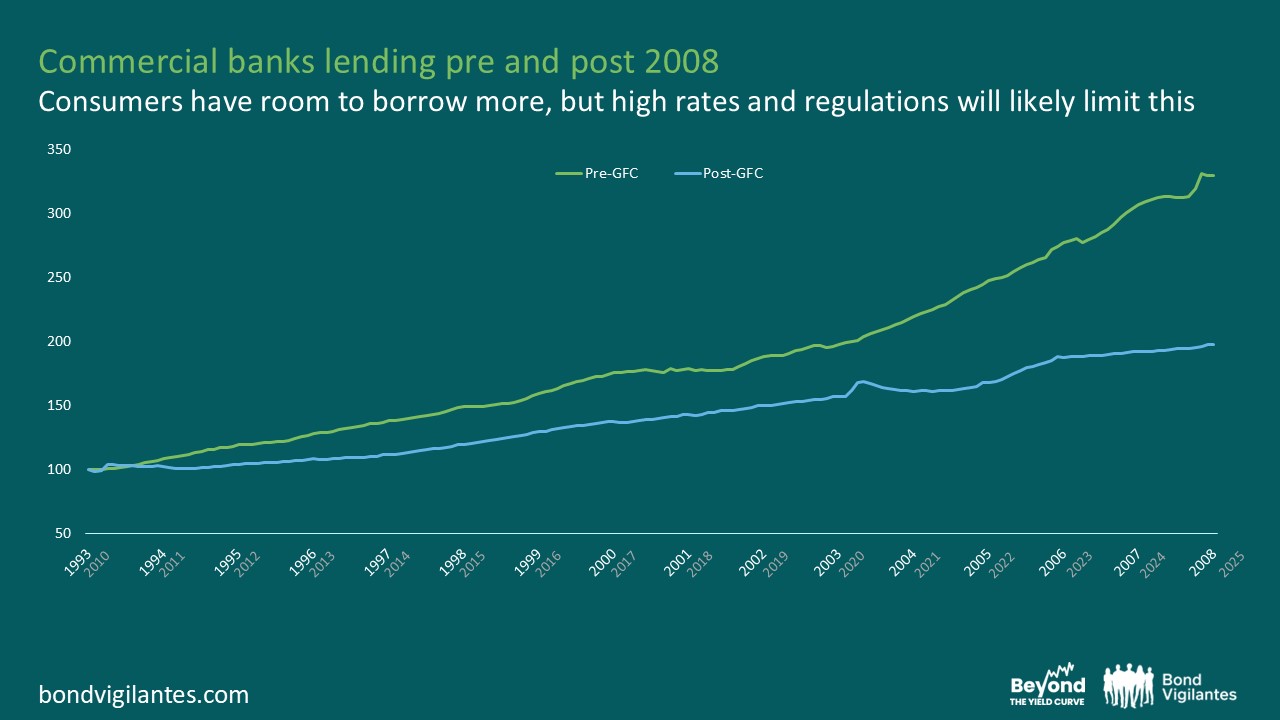

3) Borrowing: The final source of spending is borrowing, where consumers take out loans from banks. While borrowing can be a powerful tool to drive economic growth, it is also the most sensitive to changes in interest rates, especially for those with variable-rate debt. Unlike the pre-2008 economy, the post-GFC economy has been characterized by relatively modest borrowing, partly due to constraints placed on banks. This trend has not changed with COVID, and lending remains relatively limited. Although there is potential for increased borrowing, high interest rates are likely to deter significant increases in borrowing to sustain spending.

Source: Bloomberg, 31 January 2025. Ticker: ALBNLOAN Index

In summary, the key engine behind the US economy—consumption—might soon be running out of steam. Lower income growth coupled with low saving rates may push people towards borrowing to maintain their spending. However, high interest rates and a regulated banking system are likely to discourage significant increases in borrowing, thereby limiting the ability to sustain spending and, consequently, current levels of economic growth.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.