A BrAIve New World for High Yield

As the world grapples with how AI will shape and change our lives going forward from the mundane, like automated homes or more clever apps, to more existential threats (opportunities?) leading to job and possibly sector obsolescence and related, broader social implications, it’s definitely well accepted that the demand for AI computing power is enormous and growing.

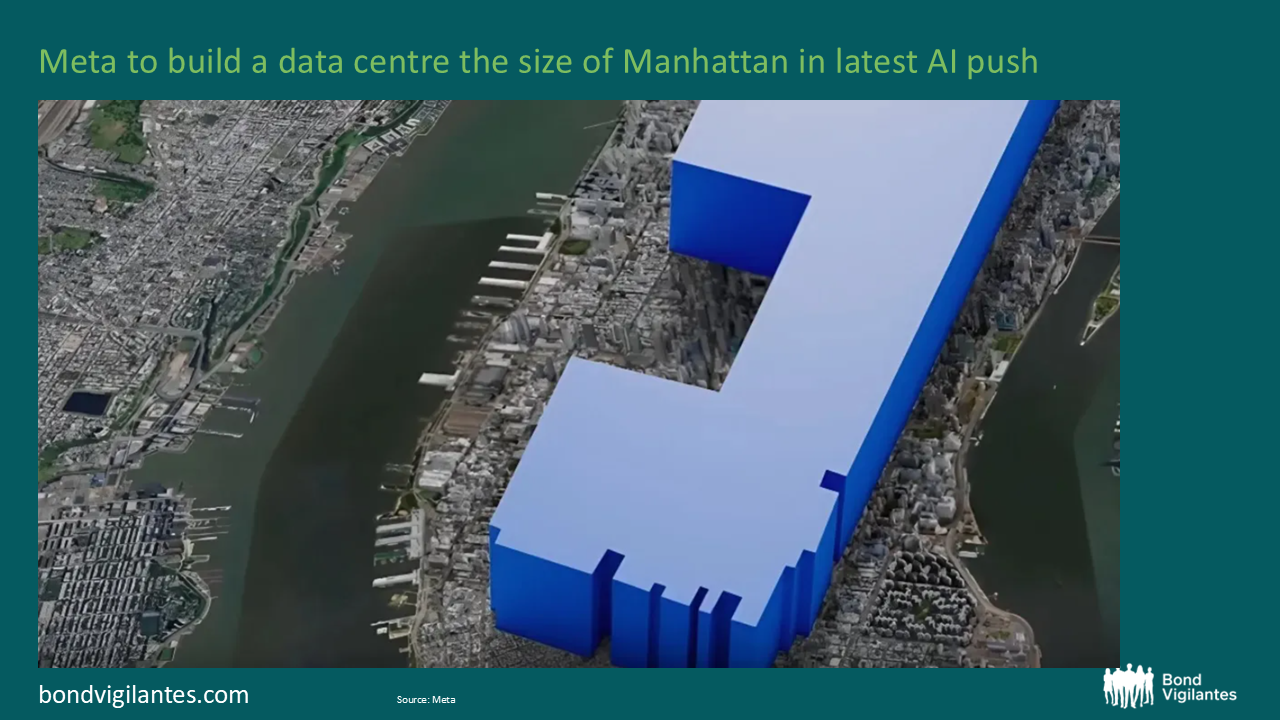

Estimates vary, but they are all astronomical, ranging from $5 trillion to $7 trillion in capital investment needed to fund the global data centre and AI buildout, including adding 122 GW of power capacity between now and 2030 (according to JP Morgan). This scale of investment will require involvement from virtually all sources of funding, including public capital markets, private credit, governments and asset-backed securitisation funding.

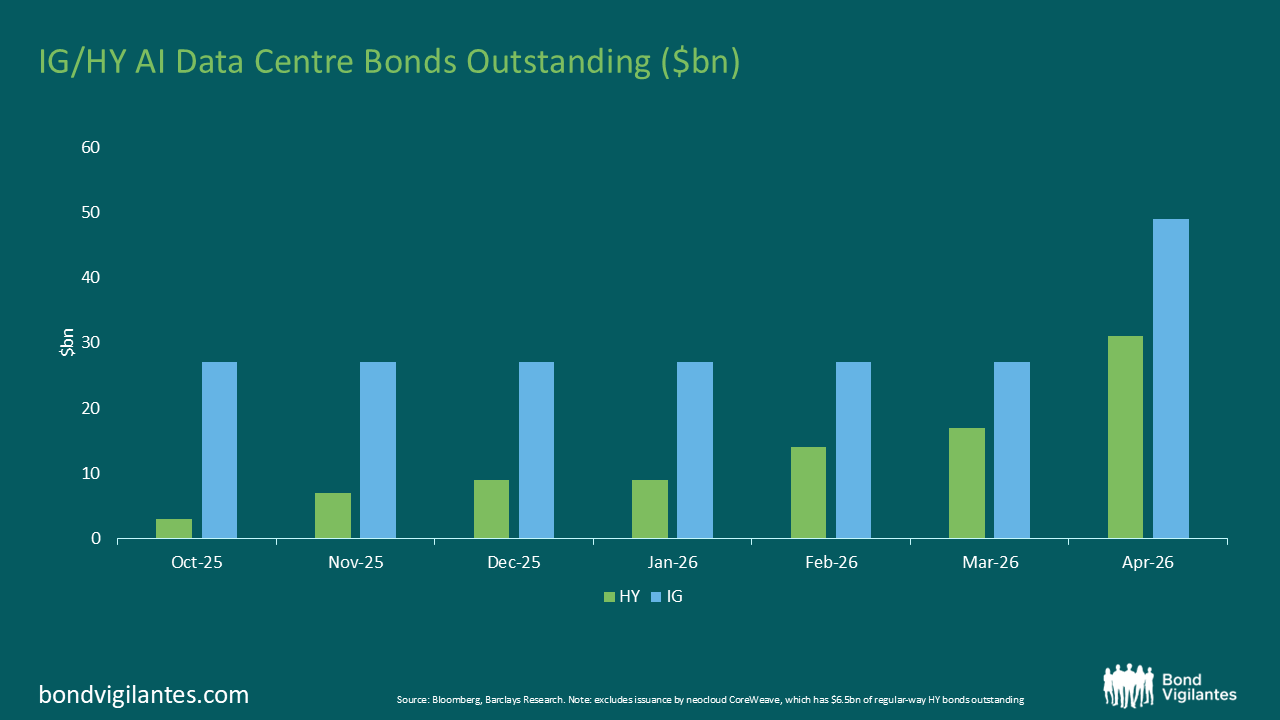

While not nearly on the same scale as investment grade markets, high yield markets have been playing, and will continue to play, a role in this buildout financing mostly via the funding of data centres. This has important implications for the asset class. In very short order, AI related and data centre issuance has exploded from effectively nothing just over a year ago to nearly $40 billion today, with close to $30 billion issued since the start of the year.

This sheer quantum of issuance is huge and effectively amounts to an entirely new subsector created nearly overnight within the high yield market. The vast majority of this issuance is index eligible and currently represents approximately 1.6% of the Global High Yield Bond Index (and 2.6% of the U.S. High Yield Bond Index). What’s more, from estimates we’ve seen, expectations are for total high yield, AI related issuance to reach $100 billion to $120 billion over the next few years.

Should this manifest, it would represent close to 4% to 5% of the global index and 6% to 7% of the U.S. index, of similar scale as long existing and well established retail and capital goods subsectors. This scale, coupled with mostly above index level yields, makes it difficult, if not impossible, for active managers that are benchmark-aware to ignore. It will be imperative to understand the broader narrative as well as the idiosyncratic characteristics of the individual issuers. As stated, this is effectively a new sector to the market and participants, such as analysts, strategists and fund managers, need to, if they haven’t already done so, get up to speed quickly.

At the time of writing there are now 15 high yield data centre bonds totalling $39 billion (including neocloud provider CoreWeave). High yield data centre bond issuance has coalesced around similar, project-finance-like features but with important variations.

Source: Bloomberg, Barclays Research. Note: excludes issuance by neocloud CoreWeave, which has $6.5bn of regular-way HY bonds outstanding

Generally, bonds are being issued with five-year non call two-year structures and mostly amortising. By definition these issuers will have more leverage than traditional IG issuers but some will have financial backstops from the likes of Google, while others will not. Most will have high-quality tenants like Nvidia, and hyperscalers like Amazon, Microsoft and Meta, while others will have a variety of tenants. Some are single asset facilities while others are multi-site and multijurisdictional. Some will be well advanced in their construction timeline while others will have yet to have broken ground. Some will have contracted power supply including back up power, and some are still negotiating power supply agreements… you get the idea. And that’s leaving aside the complexities around lease terms, cost overrun provisions, covenants etc.

There are already rumblings in the high yield market surrounding concerns that the explosion in issuance has bubble-like characteristics similar to that of telecoms in the early 2000s or energy in 2015 to 2017, when investor enthusiasm outweighed a sober assessment of risk. These same critics also worry about the potential for overbuild or overcapacity, i.e. the massive demand fails to materialise, or that despite the strong tenant base, these contracts have yet to be tested.

Conversely, proponents of the nascent space point to the undeniable demand for more compute capacity and expectations that any individual project disruptions or failures would be tolerated by their well-heeled tenants who, with strong demand for capacity, would support any centres that came into difficulty; and if not, demand is so great, other well capitalised tenants would simply step in. Further, regardless of long term dynamics, there is massive demand now and any project that is up and running, or close to, has a first mover advantage and any capacity concerns etc. are for projects well down the development pipeline.

Further, some view this as an attractive ‘yield to call’ play, inferring that as these projects are up and running and generating more cash, the issuer will have the capacity to refinance their high coupon, high yield issues at more attractive terms, arguably creating a potential short term opportunity for high yield investors.

Ultimately, being completely short the space due to uncertainties requires a high degree of conviction that the sector is mispriced and even vulnerable. Conversely, going overweight the sector is an acceptance of a broader narrative that has only recently manifested itself. All of which highlights that careful credit work on individual issuers and a broader understanding of these dynamics is paramount.

Bottom line, balancing this supply, index and yield dynamic versus fully understanding the fundamental, technical and issuer risks and rewards is a real challenge for high yield markets. And with all things AI related, we need to understand if this dynamic potentially represents – and if so, how to adapt to – to paraphrase Aldous Huxley, a Brave New World.

Source: Meta

NB Microsoft Word spell check did not recognise the words hyperscaler or neocloud, a testament to how new this landscape is that even Microsoft has not yet updated its vocabulary to account for them.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.