European corporate hybrids – the centaurs of the bond world

Guest contributor – Vladimir Jovkovic (Credit Analyst, M&G Credit Analysis team)

By now we are all well aware of the economic problems that Greece faces. Certainly we have mentioned Greece a few times on this very blog. But let’s not forget that the Greeks have given the world many, many wonderful things. Democracy. The musings of Socrates (“I am not an Athenian or a Greek, but a citizen of the world”). Zorba’s dance. And centaurs!

In Greek mythology, the centaurs are a race of creatures composed of part human and part horse. Why is this relevant? Well, corporate hybrids are the centaurs of the bond world.

Corporate hybrids are bonds issued by companies that have features of both debt and equity capital, hence the term `hybrid’. Many readers would be familiar with the original hybrid security: preferred stock, representing ownership in a company (like equity) but having fixed payments (like bonds). Another example of a hybrid security is the convertible, however, here we are referring to non-dilutive corporate bonds which rating agencies assign equity credit to, and hence are different to both prefs and converts.

Like traditional bonds, these hybrid securities have fixed coupons and can be redeemed for fixed amounts. Like equity, they are subordinated to other types of debt and issuers can choose not pay coupons under certain circumstances without triggering an event of default. Issuers also have the ability to call the bonds before maturity, which itself is typically 60 years or more and often perpetual. In some ways they are similar to tier 1 bank bonds. Like tier 1 debt, hybrid securities are deeply subordinated instruments and the extent of subordination is usually captured within the terms governing the particular security.

That said, there are differences between tier 1 and hybrid debt. For example, tier 1 debt mandatory triggers are tied to regulatory requirements and therefore have elements of standardisation, whilst corporate hybrids are more variable according to how much equity credit they are assigned by rating agencies. In addition, whilst banks require constant access to the market to finance themselves, corporate hybrids are often issued as one offs linked to individual events such as acquisitions or pension funding.

Why do corporations issue corporate hybrids in the first place? Corporate hybrids give issuers increased financing flexibility, for example with respect to interest payments and repayment maturity, whilst controlling overall cost of capital. Hybrids are sufficiently debt-like that a company’s interest payments to note holders are tax deductible. Additionally, hybrids are sufficiently equity-like that the company’s financial ratios are improved.

There are other reasons why it may be in a company’s interest to issue hybrid debt. For example, a company with pressure on its credit rating may issue hybrid debt as it is a way to obtain equity credit without issuing equity. In an acquisition scenario, the acquirer can use hybrids as a means of financing whilst reducing the impact on credit ratings. The benefit in this scenario is that by issuing hybrids the company can potentially avoid diluting existing shareholders through executing a rights issue.

From an investor’s perspective, hybrids potentially have a higher implied rate of return compared to typical corporate bonds, and offer risk diversification benefits. So these instruments can be an attractive proposition for investors and issuers alike.

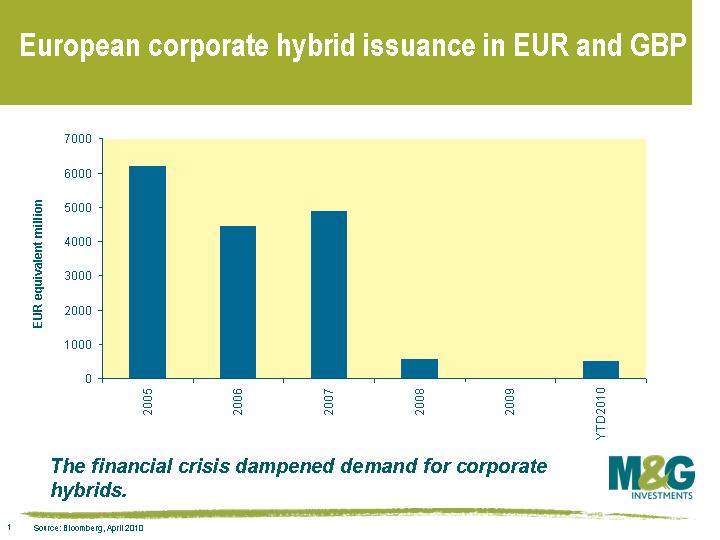

Despite their potential attractiveness, the hybrid market almost shut down as the financial crisis unfolded but is showing some signs of recovery. The current cohort of European hybrid issuers largely belongs to the 2005-7 vintages; these were all issued into a strong corporate bond market. 2008 and 2009 saw virtually no new hybrid issues as the financial crisis unfolded, but this did not spell an end to the instruments, as seen in this chart. Indeed the most recent issue was made by the Dutch grid operator TenneT in February 2010.

Despite their potential attractiveness, the hybrid market almost shut down as the financial crisis unfolded but is showing some signs of recovery. The current cohort of European hybrid issuers largely belongs to the 2005-7 vintages; these were all issued into a strong corporate bond market. 2008 and 2009 saw virtually no new hybrid issues as the financial crisis unfolded, but this did not spell an end to the instruments, as seen in this chart. Indeed the most recent issue was made by the Dutch grid operator TenneT in February 2010.

Given their complex nature it is important that investors understand the risks involved in investing in these types of securities by undertaking a thorough fundamental analysis of the company and the particular structural features of the hybrid security itself. For example, the replacement language, the call feature, the step-up rate, how the deferral trigger is defined and whether interest payments will be cumulative or not. Adding further difficulty to analysing these securities is the fact that the European market is very diverse; the rating agencies all use different methodologies, and the methodologies themselves are continuously evolving.

While the Greek god Perses (the god of destruction) is currently running amok in the Greek government bond market, we believe that the centaurs of the bond world, hybrid corporates, can potentially be a good source of alpha for bond investors providing they do their homework.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

18 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox