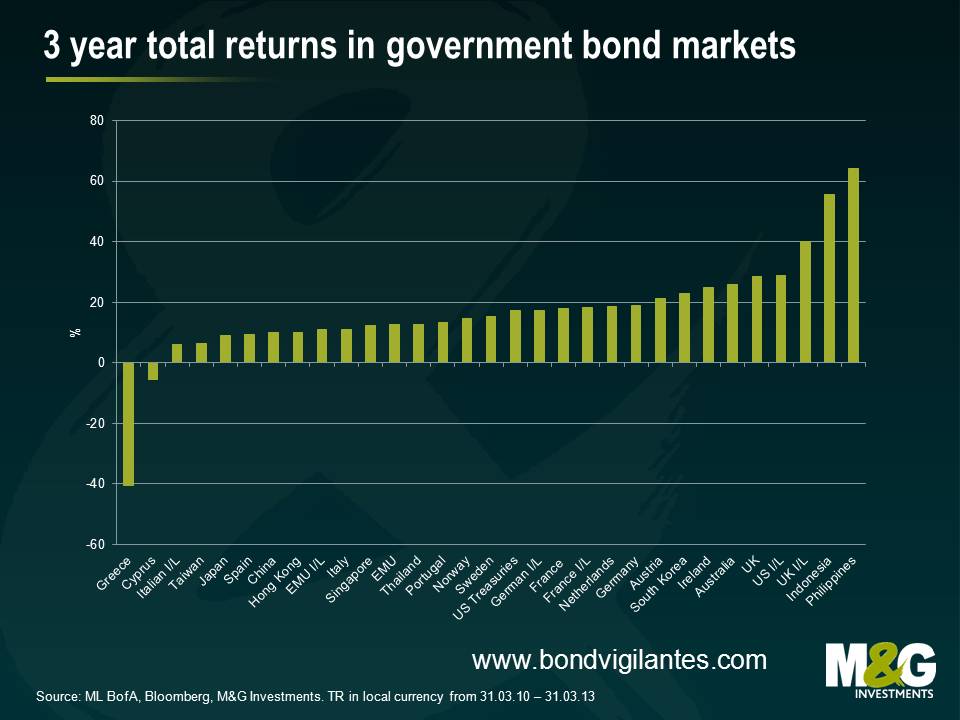

20/20 hindsight – looking at three year government bond market returns

Investors in government bonds – historically seen as a low volatile and safe asset class – have had to get to grips with assessing credit risk as well as duration risk in their portfolios. It is simply no longer the case that investors can safely lend to a government without first assessing the government’s willingness and ability to pay back the borrowed sum. This has had a large impact on government bond market returns over the past three years, the results of which are shown below.

Given the fall in yields in developed bond markets, it is unsurprising to see long duration assets like UK index-linked gilts and government bonds performing very well. For example, a broad based measure of the UK index-linked market has generated a 40% total return for investors since the end of March 2010. This is despite the UK losing its prized AAA credit rating this year. Even more surprising is the fact that the big buyer in the gilt market – the Bank of England – has not spent a single penny on a UK index-linked gilt. To date, all £332bn of government bond purchases have been in the gilt market. One investor that did buy index-linked gilts was the Bank’s £3bn pension fund, which had a 95% allocation to index-linked gilts and corporates as at February 2012.

Looking elsewhere, those that were willing to take some credit risk were handsomely rewarded in European government bond markets. For example, investors in Irish debt generated a return of 25% over the past three years. This compares favourably to Europe’s true “risk-free” asset, German government bunds, which generated a total return of 19%. That said, it was not all smooth sailing for peripheral bond investors. Just ask investors in Greek debt, who suffered a 40% loss. Investors in Cypriot government debt fared somewhat better, losing 6% over the three years. Unfortunately for investors seeking protection from Italian inflation, Italian index-linked government bonds generated a return of only 6%. This was below the increase in Italian inflation of 9% over the three year period and is the result of investors becoming more pessimistic about the Italian growth outlook.

Overall, the gold medal for government bond 3 year returns goes to the Philippines with equity-like performance of 64%. The bond market has benefited from purchases by foreign investors, largely due to its relatively strong fundamentals. The combination of a relatively high yield, strong growth and low inflation has been a magnet for government bond investors.

This analysis isn’t much of a guide for what is going to happen over the next three years. Going back to March 2010, I can’t remember many forecasting that Ireland would outperform Germany in government bond markets or that UK linkers would outperform their Italian equivalents by over 30% . So should we be worried about what the consensus is saying now? Isn’t 20/20 hindsight a wonderful thing.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox