Deflation spreading in Europe

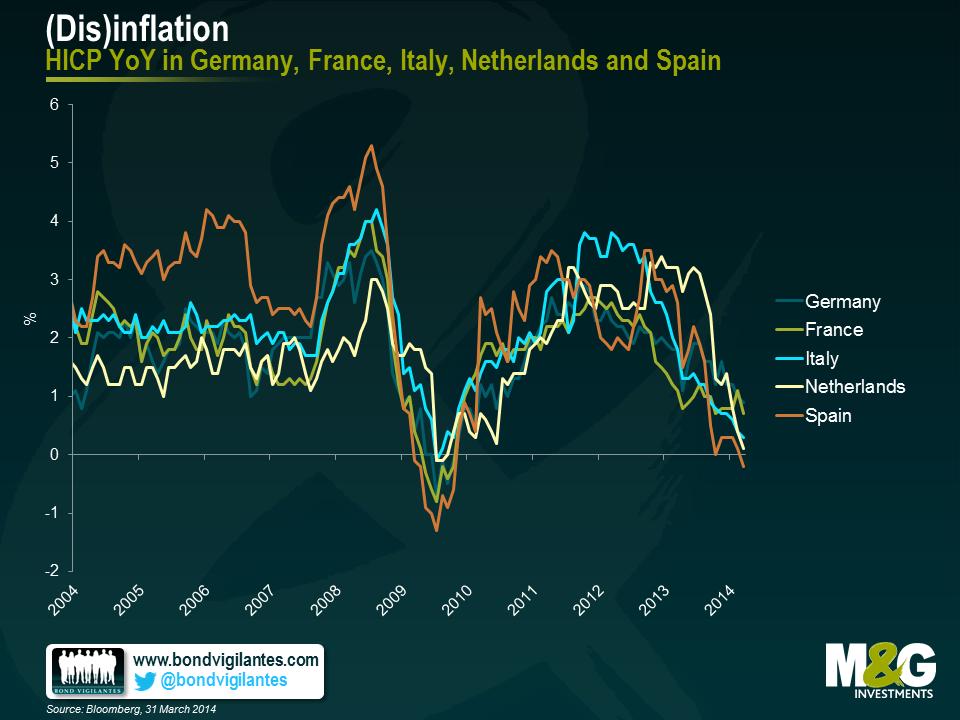

The ECB has already demonstrated an unusually, and perhaps worryingly, high tolerance of low inflation readings, with no additional action having been taken despite Eurozone HICP at 0.5% year-on-year as inflation continues to fall in many countries.

Why might this be? One reason might be that while it is very concerned about deflation, at this point in time the ECB does not have a clear idea of what the right tool is to relieve disinflationary pressure, or how to implement it. Another reason might be that it is not particularly concerned about the threat of disinflation and so is happy to wait for the numbers to rise.

With regards to the latter of these possibilities, Mario Draghi discussed the low inflation numbers in January in Davos as being part of a relative price adjustment between European economies, and as being an improvement in competitiveness. One implication from this argument has to be that the lowest inflation numbers are being seen only in the periphery, and that as a result the much needed price adjustment between periphery and core is starting to take place. The other implication from this argument is that the ECB is happy to let this adjustment happen.

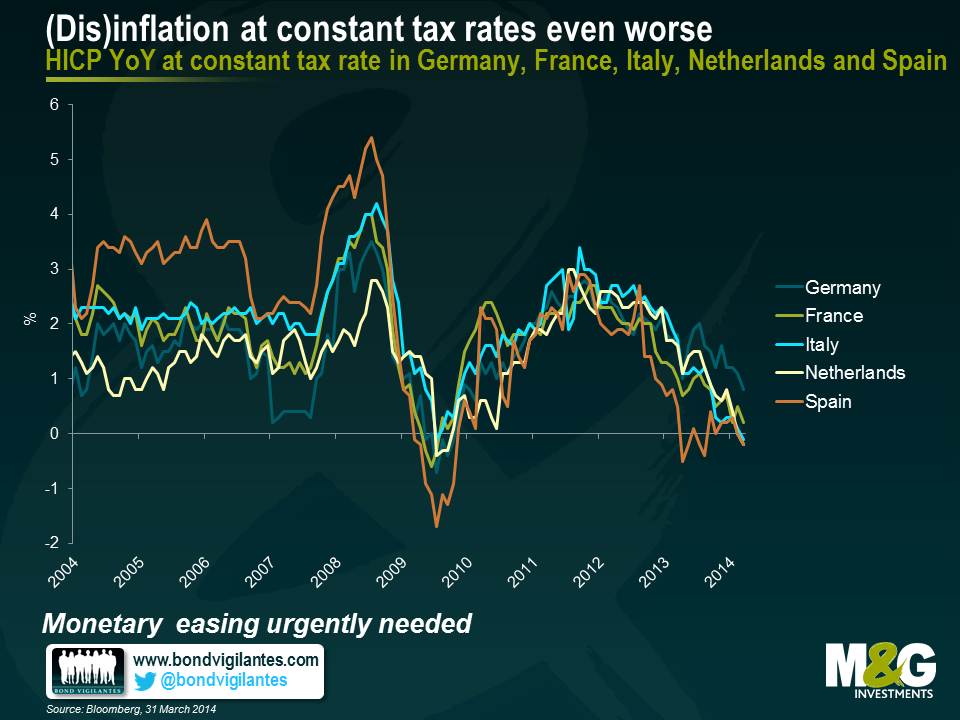

The chart below, however, shows inflation in Germany, France, the Netherlands, Spain and Italy (which together make up around 80% of Eurozone GDP) in terms of constant tax rates on a headline basis. This is important because fiscal reforms can have significant impacts on inflation numbers, when perhaps these should be stripped out as being temporary and artificial. The most obvious example of this would be a country implementing a hike in VAT, in which case inflation will jump upwards for a period until the base effect is removed some time later. This chart, alarmingly, shows that Spain, Italy and the Netherlands are now all experiencing deflation on a constant tax basis. It also shows that France is close to the precipice, with inflation on this basis at 0.2% year on year.

A further concern from the above two charts ties in to the ECB’s argument that the low inflation numbers in the periphery are a temporary phenomenon on a path to important and desirable internal adjustments to competitiveness. This argument might hold if the periphery is seeing low inflation, while the core is seeing stable, on-target or slightly above-target inflation that brings Eurozone inflation as a whole, to close to but below 2%. However, both the above charts show that the trend of disinflation is affecting more than just the periphery in isolation, and this calls Draghi’s competitiveness argument into serious question. The ECB might be well advised to get ahead of this worrying trend and act soon.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

18 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox