The Great Compression of peripheral to core European risk premiums

Are investors still compensated adequately for investing in peripheral rather than core European debt, or has the on-going convergence eroded debt valuation differentials altogether? In his latest blog entry, James highlighted five signs indicating that the bond markets consider the Eurozone crisis resolved. Inter alia, James pointed out that risk premiums for peripheral vs. core European high yield credit had essentially disappeared over the past two years. Here I would like to extend the periphery/core comparison by taking a look at investment grade (IG) credit and sovereign debt.

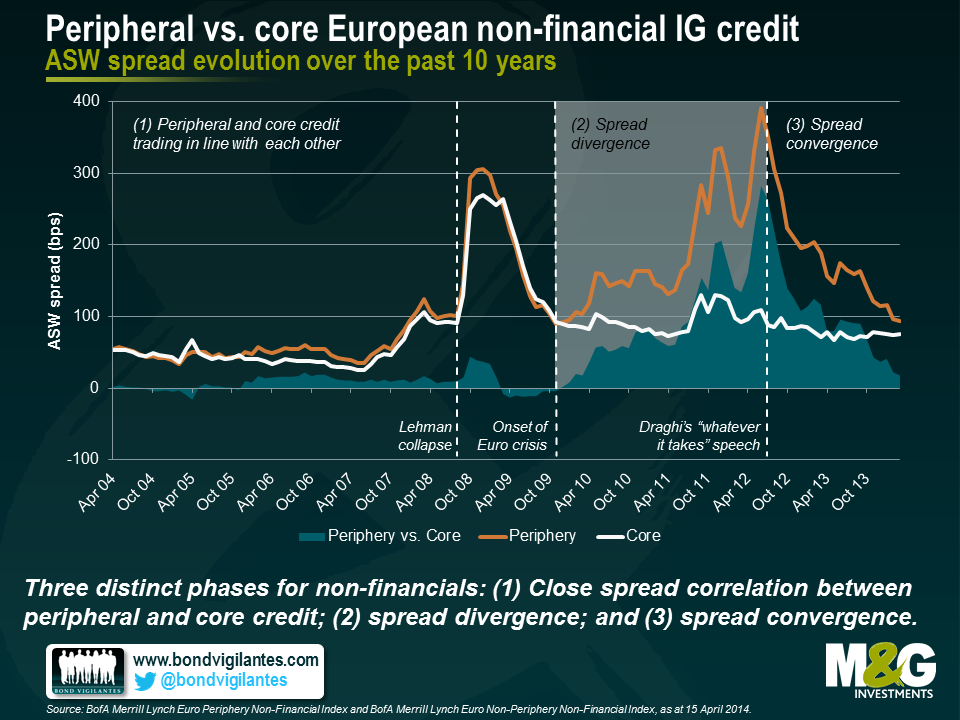

First, let’s have a look at the spread evolution of peripheral and core European non-financial (i.e., industrials and utilities) IG indices over the past 10 years. In addition to the absolute asset swap (ASW) spread levels, we plotted the relative spread differentials between peripheral and core credit. The past ten years can be divided into three distinct phases. In the first phase, peripheral and core credit were trading closely in line with each other; differentials did not exceed 50 bps. The Lehman collapse in September 2008 and subsequent market shocks lead to a steep increase in ASW spreads, but the strong correlation between peripheral and core credit remained intact. Only in the second phase, during the Eurozone crisis from late 2009 onwards, spreads decoupled with core spreads staying relatively flat while peripheral spreads increased drastically. Towards the end of this divergence period, spread differentials peaked at more than 280 bps. ECB President Draghi’s much-cited “whatever it takes” speech in July 2012 rang in the third and still on-going phase, i.e., spread convergence.

As at the end of March 2014, peripheral vs. core spread differentials for non-financial IG credit had come back down to only 18 bps, a value last seen four years ago. The potential for further spread convergence, and hence relative outperformance of peripheral vs. core IG credit going forward, appears rather limited. Within the data set covering the past 10 years, the current yield differential is in very good agreement with the median value of 17 bps. Over a 5-year time horizon, the current differential looks already very tight, falling into the first quartile (18th percentile).

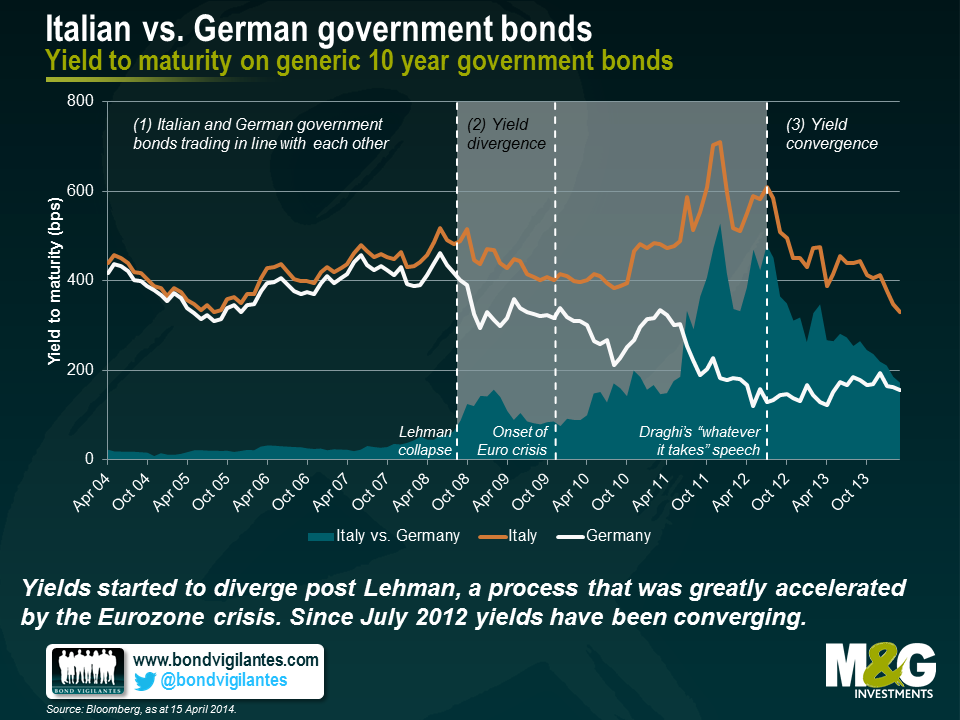

Moving on from IG credit to sovereign debt, we took a look at the development of peripheral and core European government bond yields over the past 10 years. As a proxy we used monthly generic 10 year yields for the largest economies in the periphery and the core (Italy and Germany, respectively). Again three phases are visible in the chart, but the transition from strong correlation to divergence occurred earlier, i.e., already in the wake of the Lehman collapse. At this point in time, due to their “safe haven” status German government bond yields declined faster than Italian yields. Both yields then trended downwards until the Eurozone crisis gained momentum, causing German yields to further decrease, whereas Italian yields peaked. Once again, Draghi’s publicly announced commitment to the Euro marked the turning point towards on-going core/periphery convergence.

Currently investors can earn an additional c. 170 bps when investing in 10 year Italian instead of 10 year German government bonds. This seems to be a decent yield pick-up, particularly when you compare it with the more than humble 18 bps of core/periphery IG spread differential mentioned above. As yield differentials have declined substantially from values beyond 450 bps over the past two years, the obvious question for bond investors at this point in time is: How low can you go? Well, the answer mainly depends on what the bond markets consider to be the appropriate reference period. If markets actually believe that the Eurozone crisis has been resolved once and for all, not much imagination is needed to expect yield differentials to disappear entirely, just like in the first phase in the chart above. When looking at the past 10 years as a reference period, there seems to be indeed some headroom left for further convergence as the current yield differential ranks high within the third quartile (69th percentile). However, if bond markets consider future flare-ups of Eurozone turbulences a realistic scenario, the past 5 years would probably provide a more suitable reference period. In this case, the current spread differential appears less generous, falling into the second quartile (39th percentile). The latter reading does not seem to reflect the prevailing market sentiment, though, as indicated by unabated yield convergence over the past months.

In summary, a large portion of peripheral to core European risk premiums have already been reaped, making current valuations of peripheral debt distinctly less attractive than two years ago. Compared to IG credit spreads, there seems to be more value in government bond yields, both in terms of current core/periphery differentials and regarding the potential for future relative outperformance of peripheral vs. core debt due to progressive convergence. But, of course, on-going convergence would require bond markets to keep believing that the Eurozone crisis is indeed ancient history.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox