Drifting apart: The decoupling of USD and EUR credit spreads

The decoupling of European and U.S. yields has been one of the key bond market themes in 2014 and therefore a much-discussed topic in our blog and elsewhere. Over the past two and a half months, however, a second type of transatlantic decoupling has emerged, this time with regards to credit spreads.

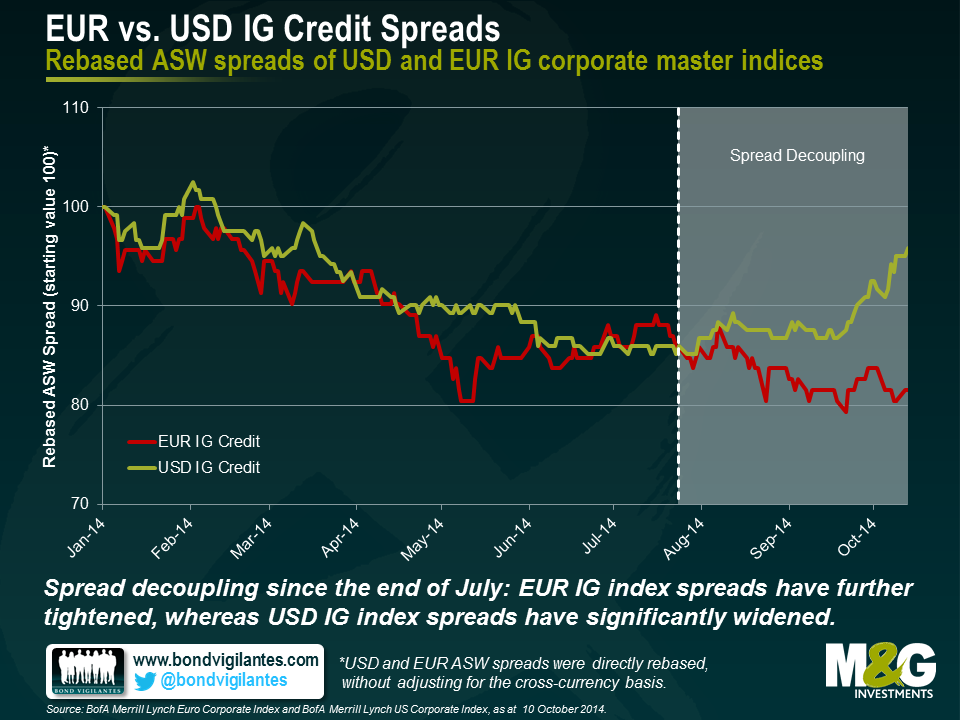

Let’s first have a look at the relative year-to-date (YTD) performance of USD and EUR investment grade (IG) credit. Both data series in the chart below were rebased, i.e., set to a common starting value of 100. With some minor exceptions, spread levels of both indices have been tending downwards fairly consistently over the year until late July. From this point onwards, a decoupling has been taking place. Whereas EUR IG asset swap (ASW) spreads have further tightened, USD IG ASW spreads have significantly widened.

Considering the divergent economic momentum over the past months, this development seems at first glance somewhat counterintuitive. The economic recovery in the U.S has been notable with 2.6% real GDP growth (Q2 2014, yoy) and a remarkable decline in unemployment rate from 10% (Oct. 2009) to 5.9% (Sep. 2014). In contrast, the Eurozone’s economy has been fairly stagnant with an anaemic real GDP growth of 0.7% (Q2 2014, yoy) and a persistently high unemployment rate of 11.5% (Aug. 2014). Against this backdrop, one might expect that U.S. corporations are in a much better position in terms of growth and profitability prospects than their European competitors, and should therefore be in general less risky bond issuers. Investors should in turn demand higher risk premiums for EUR IG credit. Therefore, USD spreads should have tightened relative to EUR spreads. So why is it exactly the other way round? Why have EUR IG spreads outperformed USD IG spreads over the past two and a half months?

First of all, from a methodological point of view, one could argue that European bond issuers suffering severely from the economic malaise have probably been downgraded into high yield territory by now, and thus cannot adversely affect IG index credit spreads. Apart from this technical side note, three reasons come to mind:

- Different central bank policies, adjusted in response to the deepening economic divergence between the U.S and the Eurozone, and their effects on refinancing costs must be taken into consideration. The Federal Reserve is about to exit Quantitative Easing (QE) and is widely expected to hike rates next year, whereas the European Central Bank (ECB) is currently in the process expanding its balance sheet and will most likely keep interest rates close to the zero bound for the foreseeable future. Going forward, U.S. companies might face higher refinancing costs relative to their European peers. To put it the other way round, an increasingly accommodative ECB is likely to keep refinancing for EUR issuers easy and thus keep corporate default rates at ultra-low levels. Therefore, EUR IG credit spreads are permanently suppressed.

- Central bank intervention has a strong effect on liquidity in corporate bond markets, too. When a central bank engages into QE, which the ECB is currently doing one way or another, investors are to a certain degree crowded out of (nearly) risk-free assets and forced into riskier assets, such as corporate bonds. More investors rushing into corporate bond markets increase trading activity and thus liquidity there. Therefore, the illiquidity premium embedded in credit spreads should drop. In contrast, if a central bank, like the Fed now, winds down QE, corporate bond liquidity is expected to fall and thus higher illiquidity premiums trigger credit spread widening.

- Another argument addresses supply side effects. According to Morgan Stanley Research, global EUR IG bond net issuance has been significantly lower than global USD IG net issuance since August (EUR 21.8 bn vs. USD 135.7 bn, respectively). On a YTD basis, EUR IG credit has in fact been in net redemption territory (maturities exceeding new issuance!) of EUR 2.3 bn, compared to a strong USD IG net issuance of USD 490.3 bn. Hence, EUR IG credit has been in short supply, effectively adding a scarcity premium to EUR bond prices, which in turn has caused spread compression.

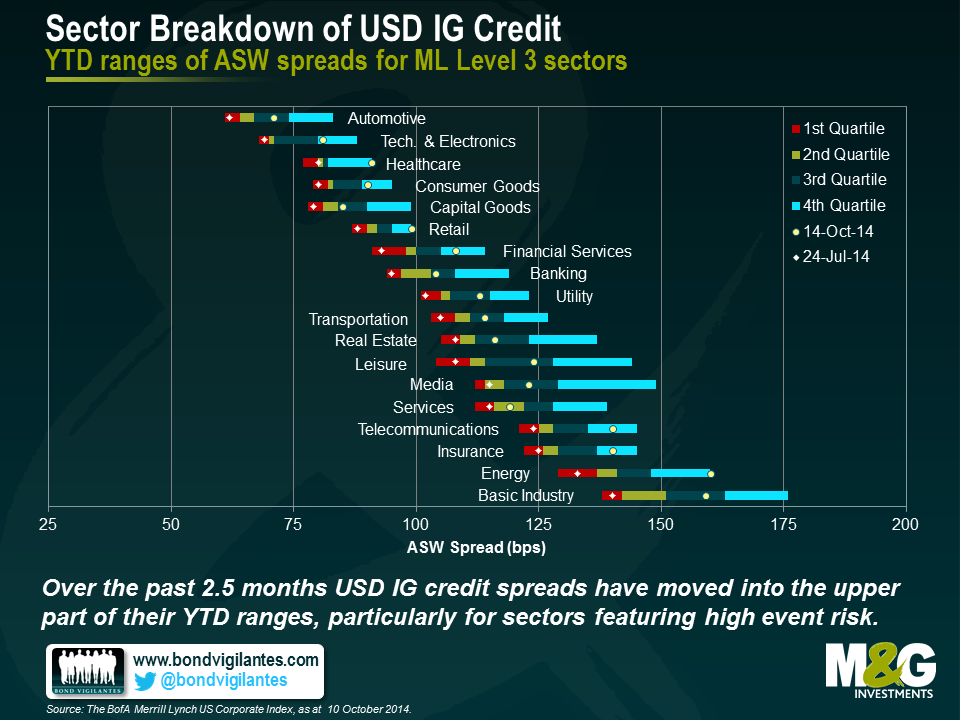

Now let’s add some more granularity by decomposing the overall index credit spread levels into individual sector spreads. The chart below shows YTD ranges of ASW spreads for USD IG corporate bond sectors (ML Level 3). All bars are subdivided into four sections, which we refer to in the following as quartiles, each of which containing 25% of the YTD spread readings. Dots and diamonds mark current sector spreads (14 Oct.) and spread levels at the start of the decoupling (24 Jul.), respectively.

It is striking that over the past two and a half months all USD IG sector spreads have widened. In the vast majority of cases, spread levels have risen from 1st quartile values near the bottom end of the YTD ranges right into 3rd or even 4th quartile positions. The spread widening has been particularly pronounced for sectors which have recently experienced an elevated level of event risk in the form of actual or rumoured M&A activity (namely healthcare, energy and telecommunications). This leads to another important point: It becomes more and more clear that the U.S. economy has entered a new phase of the business cycle, whereas Europe is still well behind the curve. American companies are increasingly taking on balance sheet risk, for example in the form of M&A, to pursue growth opportunities. Consequently, fixed income investors demand a spread premium for USD IG credit to be adequately compensated for this additional risk exposure.

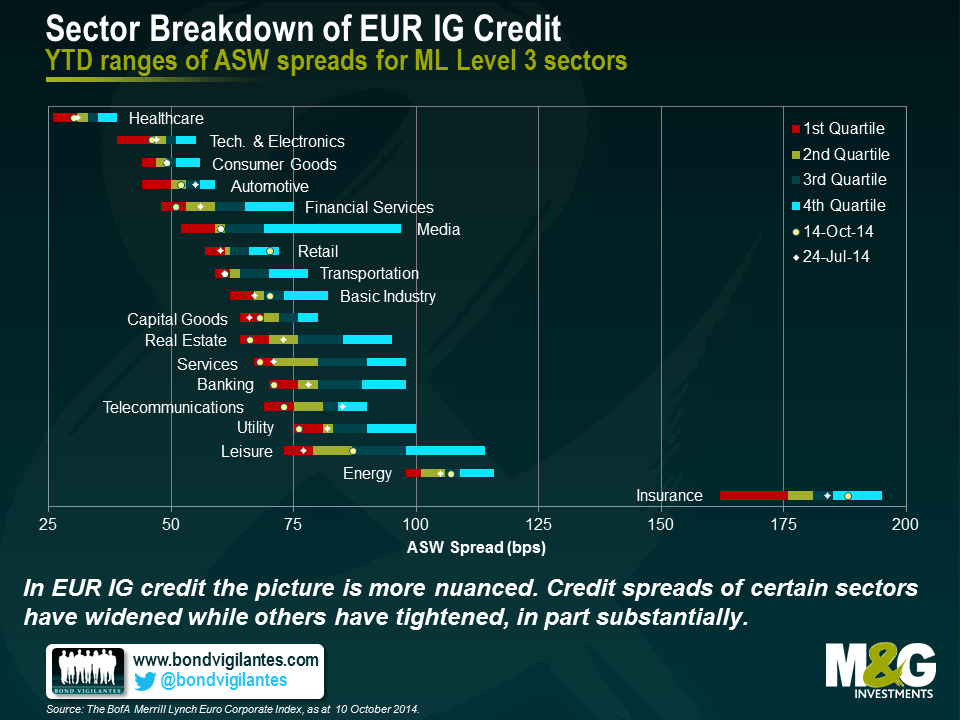

In terms of EUR IG credit, the picture is more nuanced. Credit spreads of certain sectors have widened (e.g., retail, leisure and insurance) while others have tightened (e.g., healthcare, financial services and telecommunications). This pattern, or rather the absence of a clear pattern, suggests that there are sector-specific factors overlaying the more general reasons listed above. Let’s focus on financials, for example. Banking and financial services credit spreads have substantially tightened and are currently deep in the first quartile of their YTD ranges. This is in very good agreement with a supportive ECB and reduced refinancing costs, which are a particularly important concern for financial bond issuers. In contrast, the already high insurance credit spread has widened into the 4th quartile. One explanation for this contrarian behaviour would be that lingering uncertainties around the approaching implementation of the Solvency II Directive, which selectively affect the European insurance companies, simply eclipse favourable central bank policies and supply side dynamics.

So what are the implications of spread decoupling on the relative attractiveness of USD vs. EUR IG credit? Well, the situation resembles the old Treasuries vs. Bunds debate; it ultimately comes down to the question whether one considers the current decoupling trend sustainable or not. If one genuinely believes that the divergence in terms of economic recovery, central bank policy and credit supply continues to progress, the case in favour of EUR IG credit could easily be made. The prospect of further EUR IG spread tightening, and hence capital appreciation, would outweigh lower spread and yield levels. We have in general preferred USD IG credit for quite a while now, precisely because of the higher average spreads compared to EUR IG credit, even when taking the cross-currency basis into account. Although the decoupling has certainly not worked in our favour in recent times, it has simultaneously strengthened the relative value argument. We are now obtaining an even bigger spread pick-up when investing in USD vs. EUR IG bonds than two and a half months ago. The currently low absolute level of EUR IG spreads makes the upside potential appear rather limited going forward. Finally, the global nature of corporate bond markets is likely to prevent an ever-increasing decoupling. If EUR IG spreads continue to fall relative to USD IG spreads, companies worldwide would try to minimise their borrowing costs by issuing EUR instead of USD denominated bonds. This trend would reverse current supply side imbalances and thus counteract the decoupling.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox