How bond investors should assess the opportunities in the US high yield energy sector

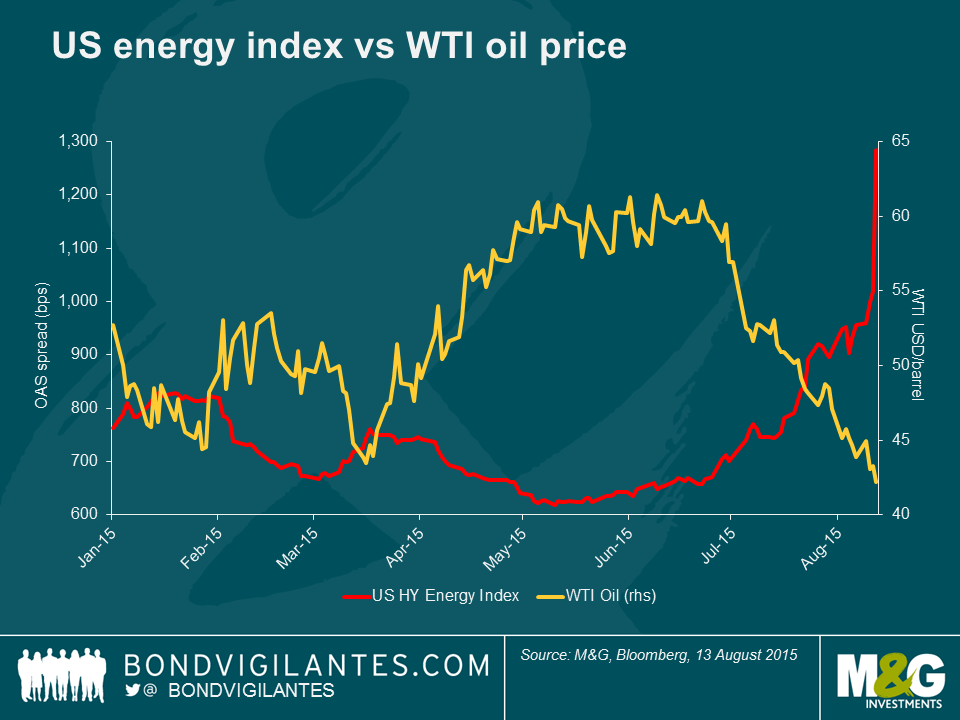

U.S. high yield energy bonds have sold off recently, virtually reversing their Q1/Q2 rally. The main culprit is, again, oil prices. The recent re-re pricing in oil has led to energy bonds trading at levels worse than the last time oil sold-off at the beginning of 2015. In fact, the BAML U.S. high yield energy index this week reached its widest levels (in terms of spreads) since April 2009 at 1019 bps.

While oil prices were trending lower throughout 2014 on slow global growth expectations, the sharp decline in late 2014 was prompted by OPECs decision to not curb production. Oil prices recovered briefly in Q2 as U.S. production cuts were expected to stabilise supply and support prices in the latter part of the year. So what has prompted oil to sell-off this time around? Well, global growth remains subdued and China’s outlook has worsened. Additionally, the devaluation of the yuan will exacerbate the pressure on commodity prices. Plus, U.S. production cuts have not been enough to offset unexpected supply from the Middle East including Iraq, while Saudi Arabia and Kuwait both posted record production levels last month. Oil prices also moved lower on the anticipation of new supply from Iran next year (estimates as high as 900k/bbd) on the back of sanctions potentially being lifted following the recent, tentative, nuclear accord.

There are a few reasons why high yield energy bonds have sold off more dramatically this time around.

Firstly, several energy companies that issued bonds secured by their assets (called Second Lien bonds) in Q1 and Q2 to extend their financial liquidity profiles have seen these bonds underperform massively. This has scared investors to the extent that this potential source of funding is effectively closed to other companies that would benefit from additional liquidity. This has had a knock-on effect on investor sentiment, with investors even abandoning bonds of companies that were not expected to need this additional liquidity.

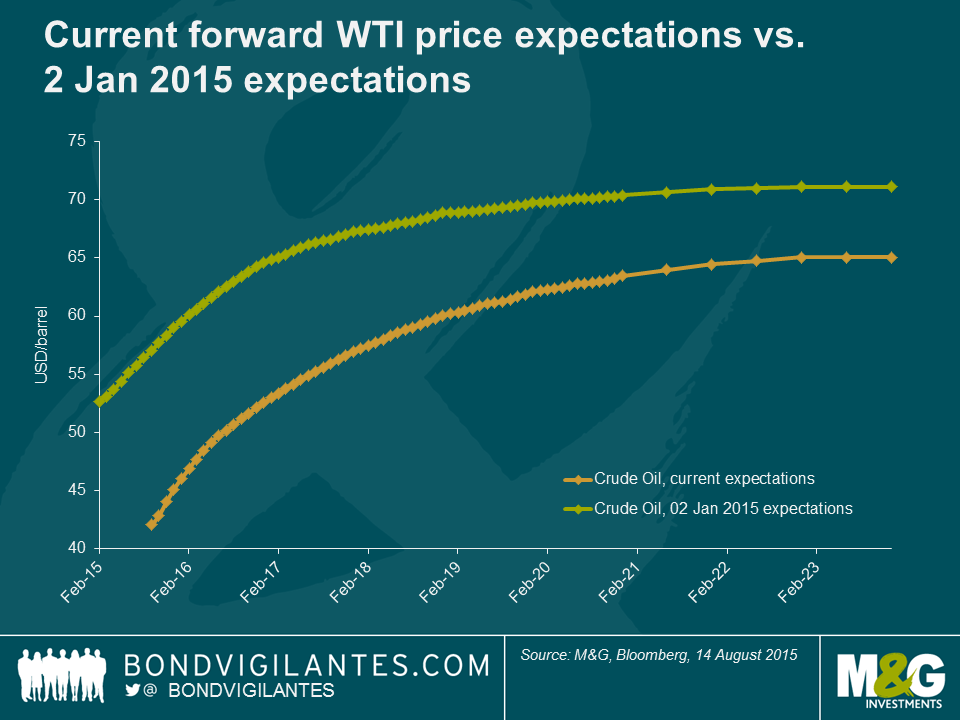

Secondly, the forward oil curve has flattened. Previously, the market was expecting a fairly robust rebound in prices in the second half of 2015 and 2016; now forward price expectations are more subdued. With many companies well-hedged for 2015 they were effectively insulated from the drop in oil prices and had time to wait for the oil price environment in improve. However, hedges eventually roll-off and the sector as a whole is, generally speaking, less-hedged in 2016. This suggests that companies will have to operate in a low-cost environment longer-than-previously expected without the benefit of hedges which is likely to impair earnings and stretch liquidity.

Finally, with the Second Lien market basically closed barring a rebound in WTI, this places greater burden on companies RBLs (Reserve Backed Lines – their asset-backed bank credit facilities) to provide liquidity. These RBLs are re-valued by the companies’ bank groups generally in October; and a lower forward curve suggests that the borrowing capacity of these facilities will be trimmed precisely at the time that earnings and cash flow are under additional pressure, stretching companies’ liquidity profiles.

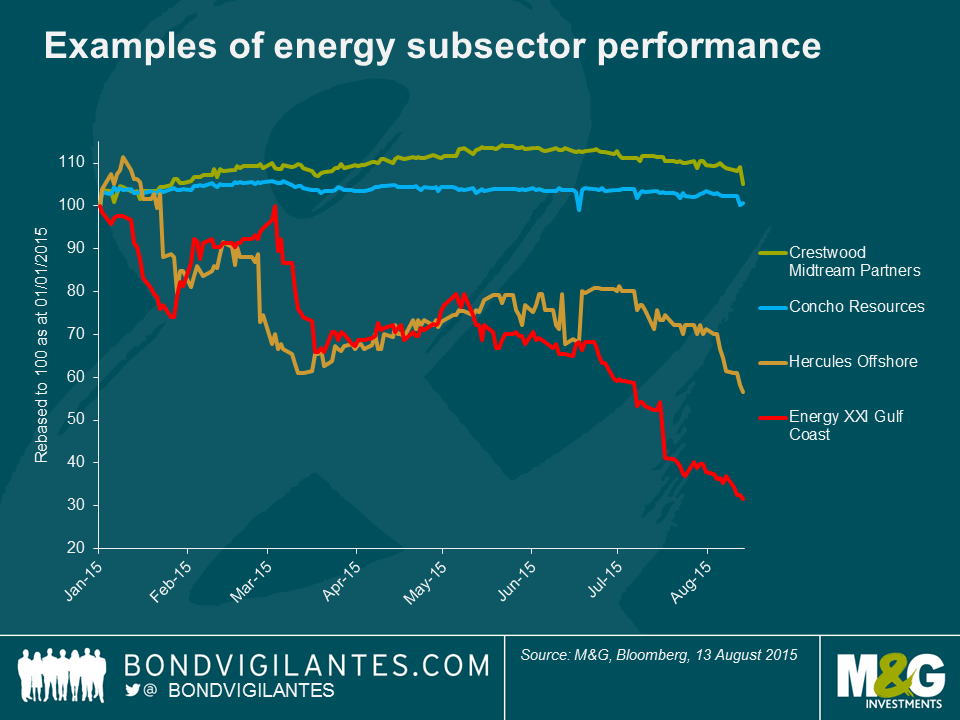

Now to be fair, the market hasn’t punished all companies indiscriminately. Service providers, offshore producers and highly-indebted exploration & production (E&P) companies have sold-off more dramatically than stable midstream (pipeline) and E&P companies with sound balance sheets and low operating costs.

The following demonstrates the price action of a few of the bonds within these individual subsectors:

- Crestwood Midstream Partners – stable pipeline company

- Concho Resources Inc. – E&P company with solid balance sheet:

- Hercules Offshore, Inc. – an offshore service provider

- Energy XXI Gulf Coast, Inc. – an offshore, Gulf of Mexico E&P company

So how should bond investors approach this space? With energy-related bonds accounting for 13.5% of the broader U.S. high yield index (off from its’ peak, but still the largest component of the index), it is difficult for investors to completely avoid the energy sector. Shunning it entirely now may result in missing out on any eventual recovery.

Despite the carnage, there is still some opportunity for patient investors to capitalise on those names that have been too severely punished and are likely to survive what now looks to be an extended low oil-price environment. In particular, investors should focus on:

- Low-cost operators capable of continuing profitable production levels at sub $50 (or even lower) WTI prices.

- Producers in good basins (the quality of basin is important as well as its location which limits transport costs).

- Manageable debt levels with limited or no near-term maturities and low financial leverage vis-à-vis earnings.

- Solid financial liquidity – solid cash levels and ample borrowing capacity from bank groups. Note, not all companies are stretched in terms of their liquidity and several were shrewdly proactive during the Q2 recovery in WTI to enhance their liquidity profiles through borrowings, extending maturities and even issuing equity.

- Dry powder regarding cost cuts – virtually all companies have cut costs, some more so than others. Those companies that have cut less but have the capacity to cut more without too severely affecting production levels have some flexibility to manage the lower price environment.

- Midstream operators with a high percentage of fixed-fee, take or pay contracts with investment grade counterparties are better insulated to manage the low-price environment.

- Identify possible M&A opportunities. The sector is ripe for consolidation and there have been a few examples of high yield companies being bought by investment grade companies to the delight of those companies’ bondholders. Rosetta Resources, for example was bought by investment grade rated Noble Energy, Inc. Similar to bond investors, investment grade companies will look at high yield operators in good basins, with low production costs and solid reserves. Investment grade companies will also look at vertically acquiring distribution and refining assets such as pipeline partners that they already have arrangements, joint ventures or similar relationships with. The chart below highlights the bonds of Regency Energy Partners which is being bought by investment grade rated Energy Transfer Partners.

We continue to avoid the service and offshore companies as, despite the extremely low prices, the risk of further downside is still high and bond volatility will be exacerbated by the entrance of aggressive, distressed investors playing in these bonds.

Will oil prices recover? It’s hard to say, but probably not in the near-term; China data, supply levels and the forward price curve suggests that oil prices will remain depressed for some time. One potential positive catalyst could be if the Iranian nuclear deal fails to pass the U.S. Congress (a real possibility), but this is likely to have only a moderate impact on oil prices given the relatively small impact on worldwide production/supply levels.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox