Covenant case study – after the good, the bad

We recently highlighted a bond covenant that benefited fixed income investors. After the good, this week we have seen the bad. In this case, a bond covenant may impact bondholders in a detrimental way. Both examples are evidence of how critical it is to have a thorough understanding of bond documentation ahead of investing in a bond.

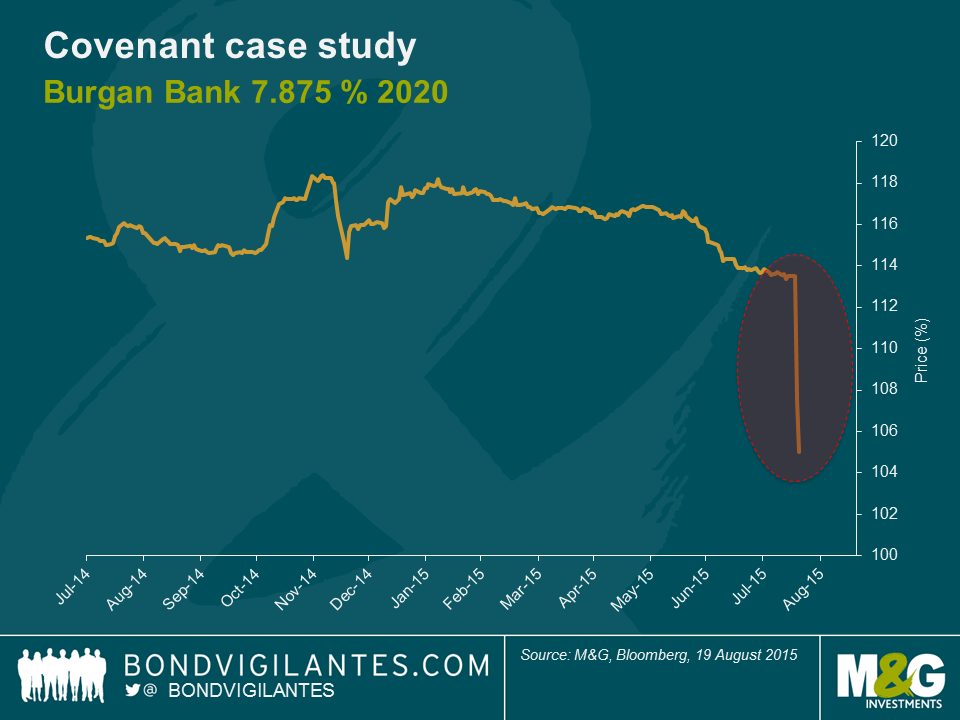

Kuwait’s third largest bank, Burgan Bank, announced in a regulatory filing that they had received approval from the Central Bank of Kuwait to redeem $400 million of outstanding subordinated bonds. In Burgan Bank’s instance, the 2020 subordinated bond – old-style Tier 2 capital – cannot be redeemed prior to 29th September 2015. These bonds were trading at a cash price of 113 as of Monday 17th August 2015.

Approval was granted by the central bank on the “redemption for regulatory capital treatment reasons” covenant. This clause is very common in bank bond documents. It gives the issuer the option to redeem at par or 101 any outstanding bonds that have lost their regulatory capital status in case of a change of regulation.

The Central Bank of Kuwait had announced the transition to Basel III capital adequacy in early 2014, with old-style Tier 2 capital not benefiting of any phase-out period unlike in Europe where there is grandfathering. The implementation of Basel III was effective in June 2014. Hence, nothing new here.

However, the Burgan Bank 7.875% 2020 bond document states on page 25 and 26 that:

Redemption for regulatory capital treatment reasons

If at any time after the date of issue of the Notes a Regulatory Event occurs, subject to the prior written approval of the Central Bank of Kuwait, the Guarantor may on or after 29 September 2015, by written notice, require the Issuer to, having given not less than 30 nor more than 60 days’ prior notice to the Noteholders (which notice shall be irrevocable), redeem in whole, but not in part, the Notes in accordance with these Conditions at their principal amount together with interest accrued to the date fixed for redemption, provided that both at the time when the notice of redemption is given and immediately following such redemption, the Guarantor is or will be (as the case may be) in compliance with the Applicable Regulatory Capital Requirements (except to the extent that the Financial Regulator no longer so requires).”

“Regulatory Event” means an event where, as a result of any change of any law or regulation occurring after the date of issue of the Notes, the Loan ceases to be eligible to qualify in full as Tier 2 Capital for the purpose of the Capital Regulations, provided that no Regulatory Event shall be deemed to have occurred if such non-qualification is as a result of either (a) any applicable limitation on the amount of such capital as applicable to the Guarantor, or (b) such capital ceasing to count towards the Guarantor’s capital base through any amortisation or similar process or any changes thereto (including any amortisation or similar process imposed through any grandfathering arrangements)”

In light of the above clause, Burgan Bank received from the Central Bank of Kuwait the approval to redeem their 2020 subordinated bonds on or after 29 September 2015. The covenant also states that the bonds are redeemable at par, which would result in a potential loss of around 13 points for existing bondholders should the bonds be redeemed.

At this stage, Burgan Bank has not officially announced whether it will or won’t call the bond. Given the high coupon on the bond (7.875%) and the current significant cash position of the bank, one might think the subordinated bonds will likely be called as it will materially reduce interest expenses and be in favour of shareholders. As of today, the bond is quoting 105 mid- price (101.3 / 108.7), reflecting a high probability (more than 50%) – assigned by the market – of the bonds being called.

Existing bondholders will not be happy should Burgan Bank call the bonds at par. This is why other options should not be ruled out. While very unlikely, the bank may choose not to redeem the bond as it has other outstanding bonds, such as a deeply subordinated hybrid security (a 7.25% perpetual), and may fear bondholders’ negative reaction. Another more plausible option is to launch a tender offer on the bonds at a price lying between par and where it was trading a few days ago, i.e. 113. In this instance, existing holders would get compensation for the loss of value. Credit Suisse had chosen this latter option when it called its Tier 1 7.875% hybrid in early February 2015. The bank offered to buy-back the notes at 103, while the notes were trading at 107 prior to the announcement.

This Burgan Bank example highlights how important it is to investors to perform covenant and regulatory due-diligence in order to avoid an ugly outcome.

*Please note we have no economic interest in Burgan Bank debt

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox