Colombia: At risk of a rating downgrade to BBB-

Part of the ABC of Latin American debt series (see here for views on Argentina and here for Brazil)

During my recent trip to Latin America it was funny (but not surprising) to hear the locals worrying about Colombia becoming the next Brazil. In turn, Brazilians are worried about becoming Argentina (though I believe the Argentinean problems are much more solvable in the near term than Brazil’s) and Argentineans believe they are a world apart from Venezuela (still true, but if they get four more years of policy inaction, it will go that route as well). It reminds me of the height of the Eurozone crisis when the Portuguese were telling us they were not Greece, Spain was not Portugal and so on.

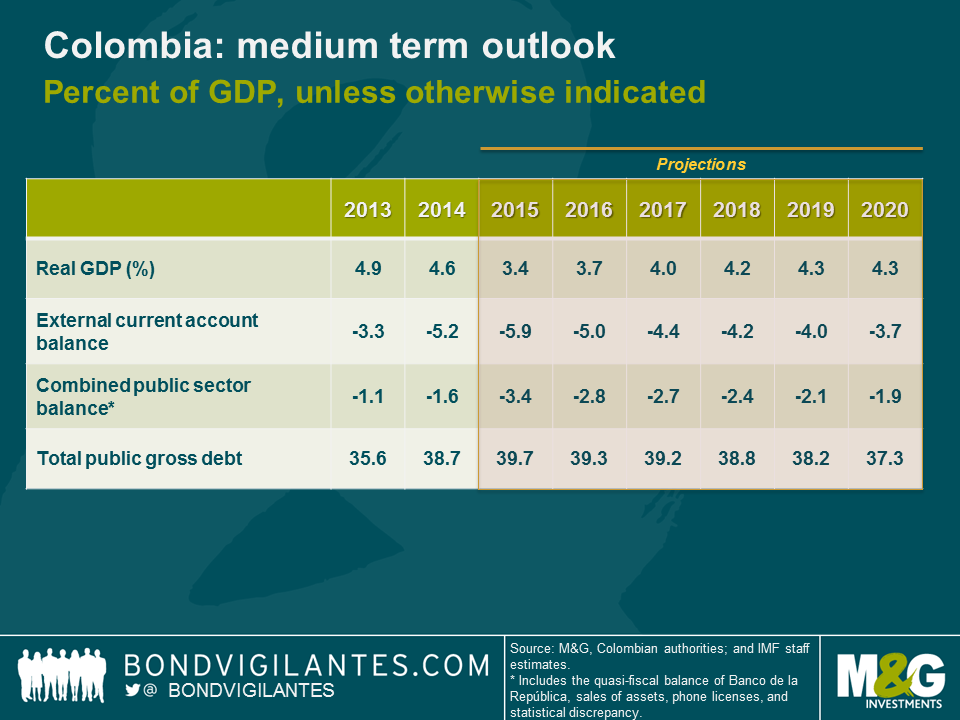

Colombia’s starting point is much healthier than Brazil’s in terms of debt levels, fiscal position and the political environment. However, it does have some similarities that, if not addressed within the next few years, could put the country into a difficult position. Both countries (and Argentina as well) have fiscal challenges and little additional space to raise taxes. Any fiscal improvements will need to come through spending cuts from politically-sensitive earmarked items, as discretionary spending and infrastructure spending has already been reduced to minimum levels. Approximately 1-2% GDP is needed to replace the shortfall in oil-related revenues and large scale tax reforms will need to be approved by the middle of next year, before the next electoral cycle kicks in. The social security system also needs reform. Infrastructure (roads, public transport, etc.) in the region is very poor (Colombia ranks particularly poorly here) and most countries are hoping for public-private partnerships to help fill the gap.

A rebound of growth in the medium-term will also help, but in the short-term growth is under pressure from various shocks: terms of trade and the oil price decline, supply-side inflation pressures (especially if El Nino turns out to be a strong one), a much weaker currency, which is acting as the shock absorber, and potential tax hikes. On the positive side, the peace process between the Colombian government and the FARC could deliver a 0.3-0.5% increase in potential growth over the medium to long term.

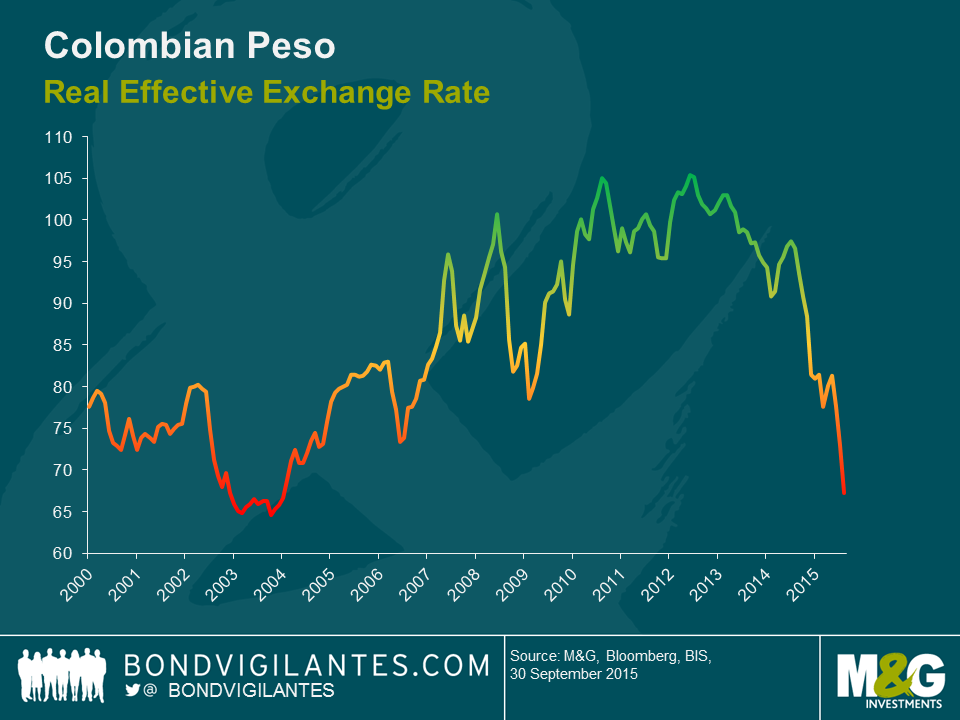

I returned from my trip more cautious than the authorities and the IMF on their near term assessment (see chart above). I see downside growth risks coming from falling consumption as purchasing power declines over the next 1-2 years. I am also concerned about the structural nature of Colombia’s current account deficit, which even after a large real depreciation of the Peso, is expected to hover around 4% of GDP. Unlike Brazil, where I see it as one of the few bright spots, Colombia’s non-traditional exports have a high share of imported content and high transport costs, so the currency depreciation will help to revive exports by much less than I expected. Additionally, exports to its main trading partners (Ecuador and Venezuela) continue to fall. The bulk of the adjustment will need to come from lower imports as a result. With only about 50% of the current account deficit financed by foreign direct investment, the rest will likely need to be financed by sovereign external borrowing. The authorities are expecting that the forthcoming 4G infrastructure concessions will bridge a large share of the investment gap and the upcoming privatization of energy company ISAGEN will be closely watched, as the proceeds will help to leverage the infrastructure concessions. Consequently, there are downside risks to the fiscal outlook as well, which means debt levels will be increasing further. As a result, I expect the rating agencies to change the country’s outlook to negative, with a downgrade to BBB- should the tax reform disappoint and the infrastructure concessions be lower than expected.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox