Emerging market debt: 2016 post-mortem and 2017 outlook

Despite a year of high political turmoil – which of course included the UK EU referendum and the US elections – emerging market assets proved surprisingly resilient to the various global events, even with rising core government yields in the second half of 2016. Given that starting valuations at the beginning of the year, both with respect to credit spreads as well as currencies, were pricing in quite a bit of negative news, this initial cushion allowed the asset class to navigate the year relatively well. The return of inflows into the asset class following the Brexit vote and the recovery of commodity prices, particularly oil, also helped spreads to tighten. Below, I give a run-down of the year just gone and highlight my key calls for emerging markets in the year ahead.

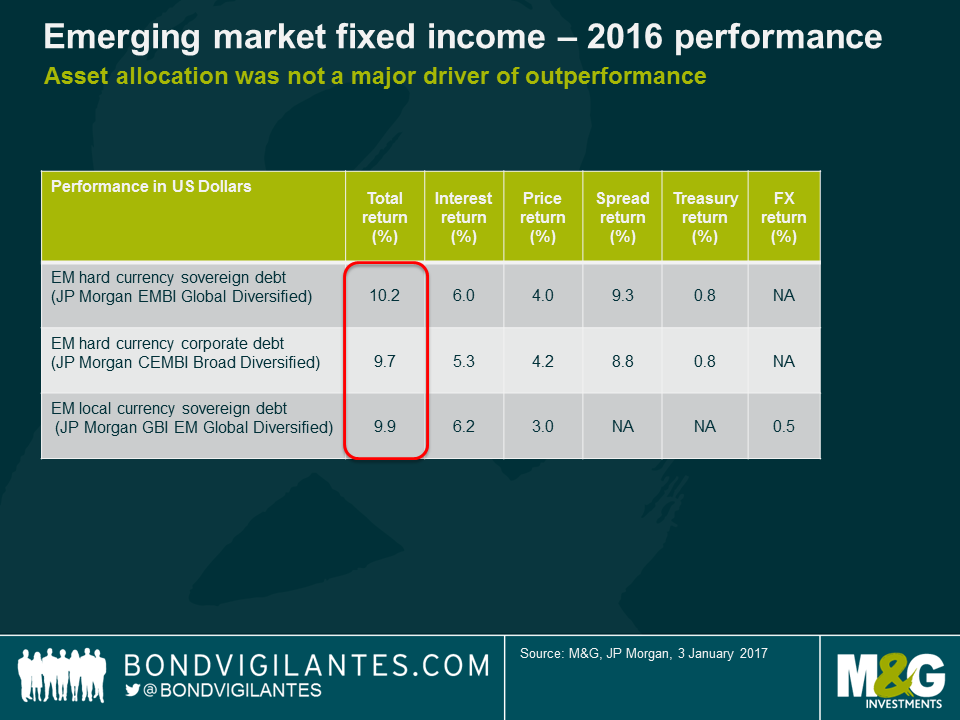

- Asset allocation was not a major driver of performance

Total returns were almost identical for hard currency, local currency and corporates in 2016. In last year’s outlook, I surmised that asset allocation would not be a predominant driver for the asset class and I expect this trend to continue into 2017. Instead, I expect that a call on beta and overall risk will be more important than the asset allocation given starting valuations being less generous this year, particularly in hard currency sovereigns and corporate spreads.

- Currency valuations provide some cushion to a stronger USD

Currencies, for the most part, are in the range of fairly valued to somewhat undervalued and this provides a cushion for a stronger dollar environment, fuelled by higher rates in the US. The recent recovery in oil prices is additionally supportive for currencies such as RUB and MYR and there is quite a bit of bad news priced into MXN, but I do not believe there will be material changes to NAFTA from the upcoming US administration.

Higher oil prices take some pressure off the pegged Gulf cooperation currencies, as this will allow the region to continue borrowing at more favourable rates in the international markets, as tighter spreads partly offset higher US yields.

The current account adjustment is well underway (or complete in many EM countries), with some notable exceptions such as Turkey and South Africa. The big elephant in the room however is the Chinese Yuan Renminbi, which continues to be vulnerable to capital outflows and potentially negative news should the incoming US administration pursue unfriendly trade policies and/or name China a currency manipulator. While my base case scenario does not contemplate the floating of the currency in 2017, it remains a tail-risk to be mindful of.

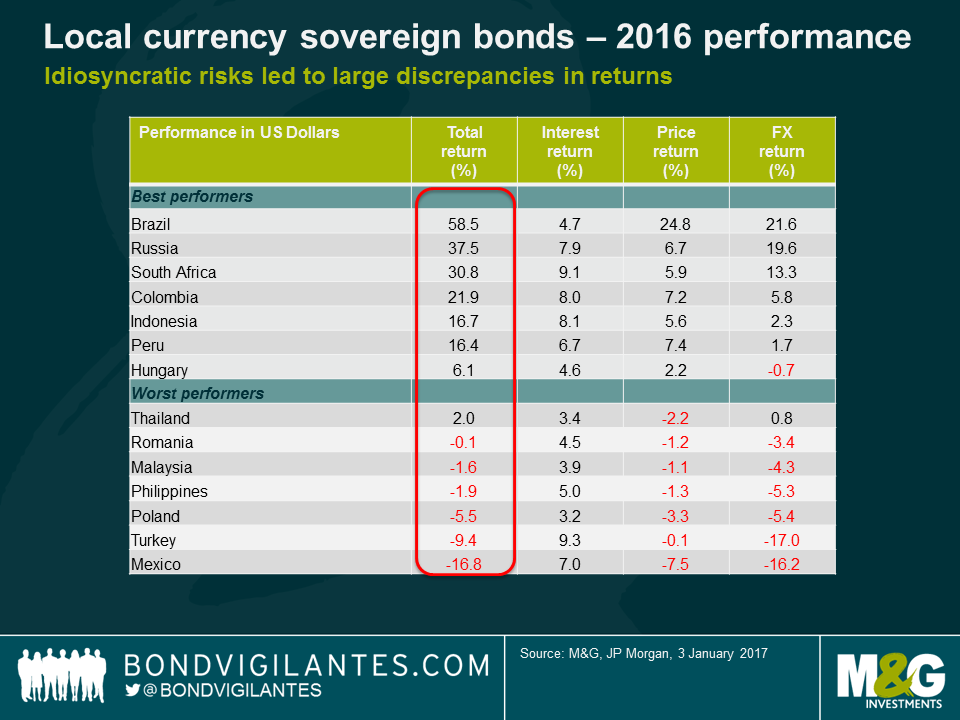

Local markets produced a wide dispersion of returns, both in terms of FX returns as well as yields, but this dispersion should be much less pronounced in 2017.

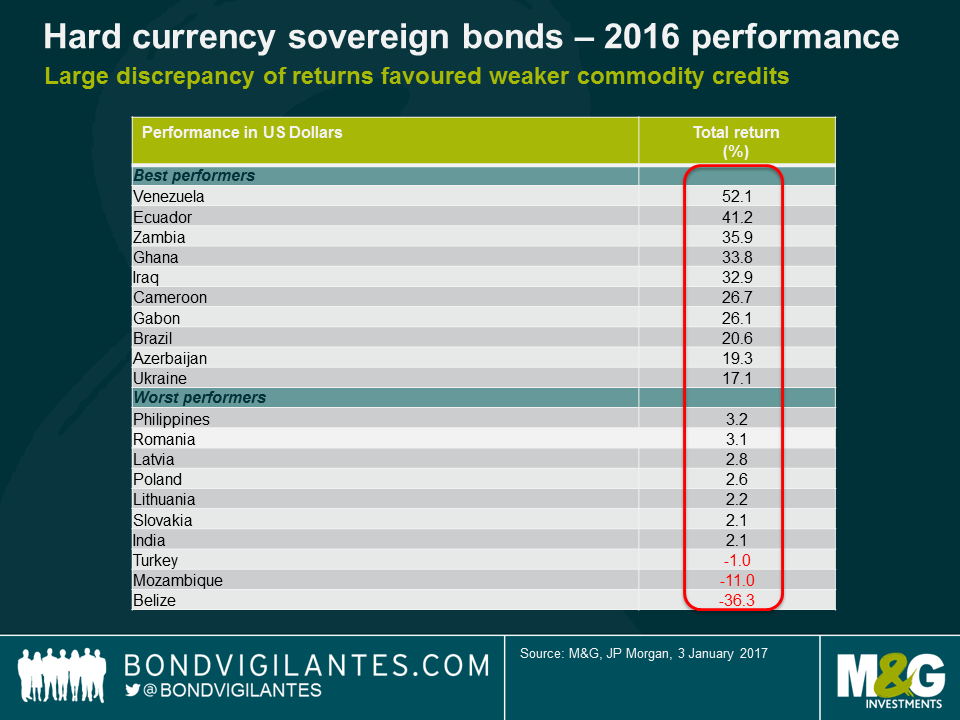

- Spreads tightened, particularly in commodity credits and Brazil

2016 proved to be the mirror image of 2015. In countries such as Brazil and Argentina, the recovery of commodity prices and perceived improvement in the political climate led to a large rally in these credits. In fact, with the exception of Ukraine, all top performers in 2016 were the previously weaker performing lower-rated commodity credits.

At the other end of the spectrum, Mozambique and Belize announced restructurings in 2016 and as such, the likelihood of any additional sovereign credit events is centred on Venezuela, which stands out as the binary call for 2017. The country, once again, will prove to be either the best performing credit if they do not default, or the worst if they do. With the prospect of political change and more pragmatic economic policies dimming, the chances of a Venezuelan credit event have increased in 2017, as rising oil prices are still not enough to close the financing gap. On the whole however, given that there are fewer sovereign credits at risk of default in 2017, return dispersion and bottom-up differentiation within emerging markets should therefore be less extreme this year.

Brazil will not be the outperformer in 2017 as existing valuations are priced for a perfect execution of policy. More importantly, the outperformers of 2016 will not generate double digit returns as this would require them to trade at unrealistic spread levels, i.e. some 200-300 bps of additional tightening. Instead, I expect more moderate mid-single digit returns, basically in line with the carry.

- Idiosyncratic risks continue with developed markets in 2017

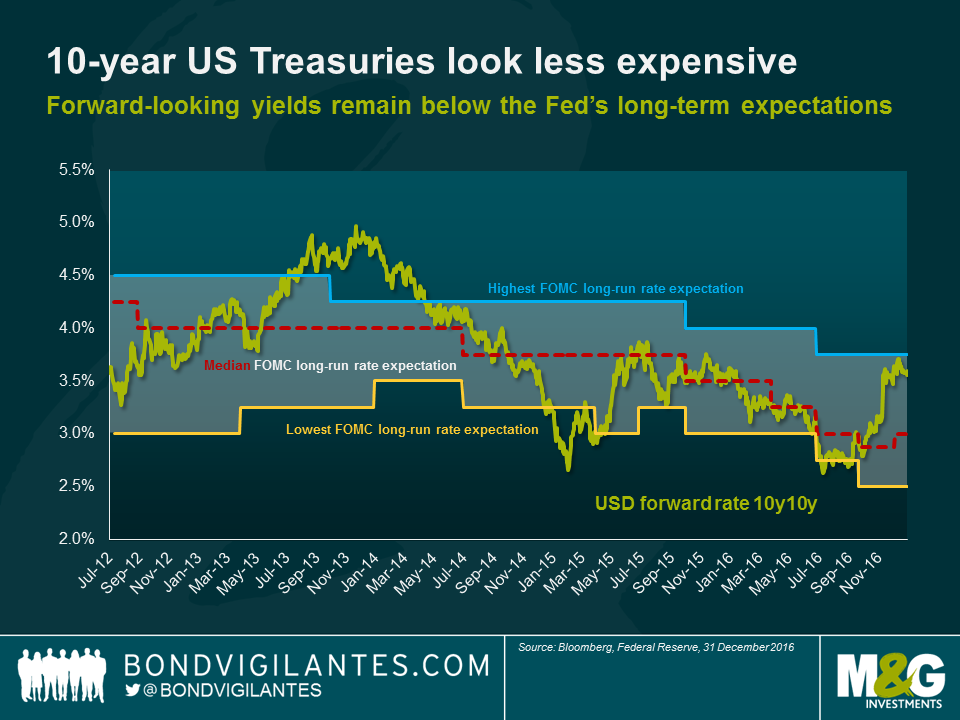

Politics and economic policy developments in the US, as well as key elections in Europe are the major foreseeable events to be digested in 2017. Monetary normalization continues in the US and treasury yields, while not cheap on a long-term basis, have at least adjusted closer to fair value in the near term and should prove to be less of a headwind to returns in 2017. This is relevant as spread returns should be much lower than 2016 as well.

I expect asset allocation between hard and local currency to remain a small driver in 2017. Bottom up hard currency and local currency selection will remain somewhat important, but with a much smaller return dispersion than in 2016. Instead, a call on beta and overall risk will be more important given starting valuations.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox