The hunt for emerging market yield is killing covenants

Would you buy a 7-year unsecured bond at 6% yield from a B1/B+ rated Brazilian airline (first time issuer) with well-below-standard credit covenant protection for investors? Many did last week. Few would have a year ago.

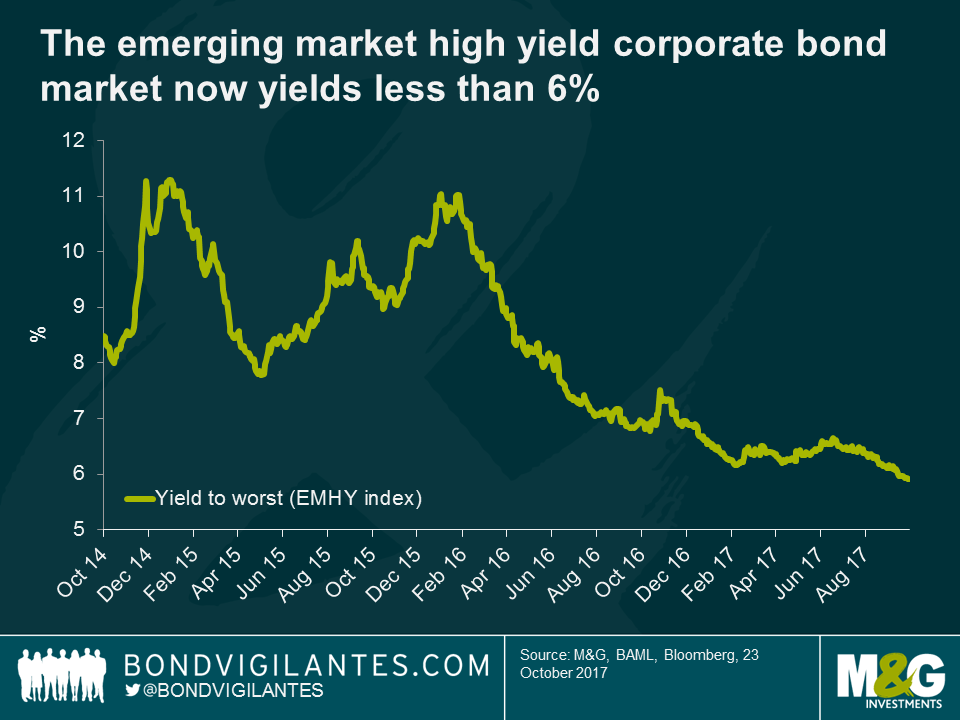

This year, many emerging market bond investors have been tempted to lend further down the credit spectrum in search for higher yields. Strong inflows into the asset class combined with the current low default rate environment has helped to encourage this trend. The primary market and in particular debut bond issuance have become key areas of focus, as this is usually where investors find mispricing opportunities and capture new issue spread premium. The flip side of the high demand for EM high yield primary deals has been an erosion of covenant protection. Corporate issuers and their financial advisers have been increasing issuers’ financial flexibility by reducing credit investors’ protection in bond documentation. Long story short, the search for yield in emerging markets has been killing EM high yield covenant standards recently.

I have come across multiple examples in the past six months. The most bizarre one was when a Pan-Asian healthcare provider issued non-rated perpetual bonds with a change of control call, not put! This gave the issuer (not the bondholder) the right, but not the obligation, to buy back their own bonds at 101 in the event that the company changes ownership. This essentially amounts to a blank cheque for an M&A transaction without having to refinance the existing capital structure. I asked my European and US HY fund manager colleagues if they had seen this before, and they too had never heard of such a feature.

Then we had a number of mid-BB bond issuers, in particular from Latin America, coming to market with some standard HY covenants such as a restriction on how much debt they can issue based on meeting a minimum level of fixed charge coverage ratio (EBITDA to interest) and similarly restriction on payments like dividends based on the same ratio. However, none of the restrictions were based on a leverage ratio (debt to EBITDA) which is usually a market standard.

Finally, we had a Brazilian airline last week which successfully issued B+/B1 rated bonds with no restrictions on how much debt they can issue, nor how much in dividends they can pay to shareholders. This means, on paper, that the financial policy might favour shareholders at the expense of the credit profile of the company with no controls from unsecured bondholders. I doubt that any of the lending banks would allow a similar situation on secured debt.

I think EM corporate bond investors have it all wrong. In periods of economic recovery – like EM is currently experiencing – corporates tend to engage more in dividend upstream or transformational projects (M&A, large expansion capex). In periods of economic troubles, financial discipline is usually implemented to preserve cash flows, credit metrics, investor confidence and ultimately access to capital markets. This happens in order to attempt to ensure that refinancing maturities remain at an acceptable yield for issuers. In other words, credit covenants are a protection against the downside and in my view are even more vital when corporate bond spreads are tight. In the current market environment, capital that is chasing higher yielding assets is agnostic to the risks of any possible downturn. This poor security selection will hamper returns in a selloff scenario, with those that have implemented careful credit differentiation in the good times more likely to weather the storm.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox