Panoramic Weekly: Risk Assets Rally Despite Trade Wars

Traditional fixed income risk assets, such as Emerging Markets (EM) and High Yield (HY), rallied over the past five trading days, shrugging off an escalation of the trade tensions between the US and China. The world’s No. 1 economy announced plans to set tariffs on an additional US$200bn worth of Chinese goods, adding to the $34bn that came into effect on Friday. The almost 200-page list of goods, including live fish, antiques and wooden doors, raised new concerns about China’s exports and weakened the renminbi to 6.67 against the US dollar, its weakest level in almost one year. Chinese debt and equity markets suffered, particularly High Yield (see more below).

The renewed trade tensions, however, did not deter EMs from a sharp rebound, partially fuelled by a weaker dollar. The greenback dropped following Friday’s US jobs report, which sent a mixed picture of the economy: while hiring was up, wage gains ebbed, pushing down breakeven inflation rates and market-implied probabilities of future rate hikes. EM currencies soared, led by the Mexican peso, which surged 2.7% against the dollar after president-elect López Obrador announced meetings with US officials to discuss the North American Free Trade Agreement (NAFTA). López Obrador has also reached out to business leaders and committed to keeping the country’s deficits under control.

Commodity markets, however, were hit by the renewed trade wars, with copper down 2.45% over the past five trading days (read more below). The Turkish lira didn’t survive the week, either: it lost 2% against the US dollar after the country’s current account deficit widened and president Erdogan assumed new powers to name the central bank governor and appointed his son-in-law as chief economic policy maker. Sterling gained 0.5% against the US dollar over the past five trading days, unscathed by recent political turmoil (more below). The Bank of Canada raised rates by a quarter point to 1.5%, the second hike this year.

Going up:

China corporate spreads – high enough? The gap between China’s HY corporate spreads and US Treasuries continued to rise in July, reaching 367 basis points – the widest since April 2015, when the central bank was cutting rates to stem a declining pace of growth. The recent move reflects rising investors’ concerns about the renminbi’s 5.3% drop against the US dollar over the past 3 months and mounting fears about the effects of the new US trade barriers on China’s exporters. The ongoing domestic battle to reduce leverage, a rising greenback and higher US interest rates have also led investors to demand more compensation for risk. Spreads have now risen to a level that, for some, may be high enough to buy the dip. China’s economy is also on track to meet its c. 6.5% growth target this year, mainly boosted by internal consumption – the country, for instance, sells more cars domestically than the US. Growth may also be less challenged by trade wars than it is often believed: while the current account surplus used to represent 10% of GDP in 2007, it barely accounts for 1% now. More domestically-geared economic growth could also underpin leading economic sectors, such as real estate. The housing industry, however, is going through a recovery phase on concerns of unsustainable high prices and a rising default rate. More defaults, however, are sometimes considered as a positive as they improve the country’s credibility at a time that China is planning to open up its credit markets to international investors.

World Cup, weather, royal wedding outweigh political turmoil: Growth is coming home: Sterling gained 0.5% against the US dollar over the past five trading days, unharmed by the resignation of the country’s top Brexit and Foreign Affairs officials. The currency was instead more responsive to economic growth, which rose 0.2% in the three months to May, and to improving consumer spending data: a combination of good weather, the recent Royal wedding and World Cup success helped lift consumer spending by 5.1%, year-on-year, in June. The optimism pushed up the market-implied possibilities of an August rate hike to 82%, the highest since April.

Going down:

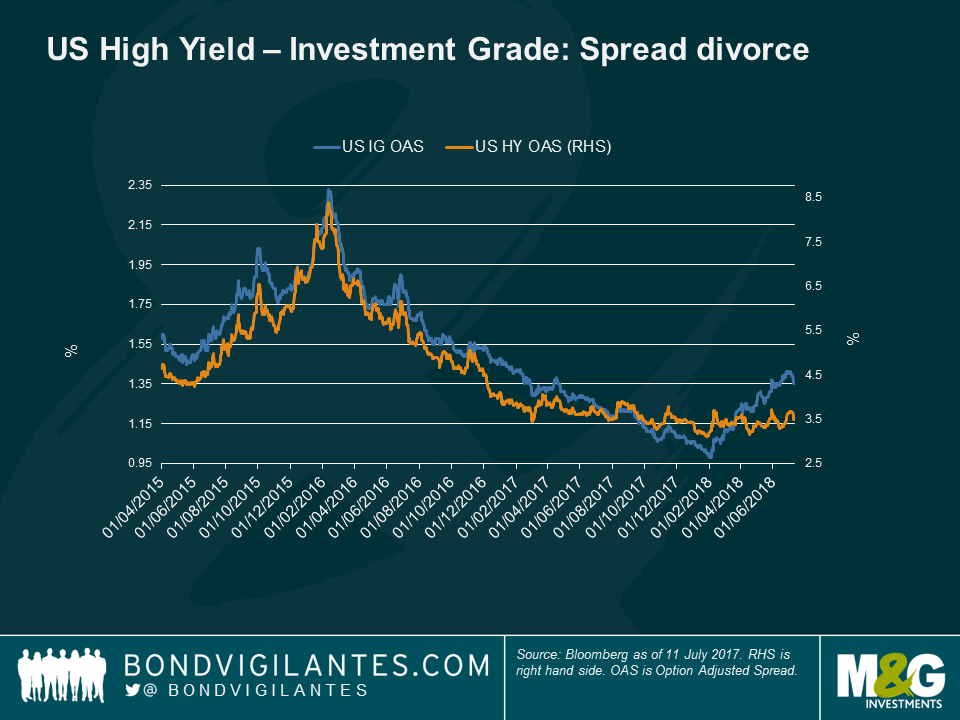

US High Yield and Investment Grade: decoupling: After months of moving in lockstep, US Investment Grade (IG) and HY debt started decoupling in the second quarter of the year, although in this instance, it is not so much HY spreads that have flown away, but the traditionally steadier and quieter Investment Grade ones. The move follows this year’s heavy IG supply, which has lifted the premium demanded by investors, as well a dearth of HY issues as investors are more reluctant to buy issues at low yield levels. US IG is also suffering from a deterioration in quality: companies with a BBB rating (the lowest IG rank) now account for half of the asset class, up from 34% in 2006. Along with US loans, UK inflation-linked bonds and EM bonds, US HY is one of this year’s top performing asset classes – it has gained 3.2% over the past 12 months, surviving trade wars, political turmoil in Italy and a general rising rate environment. Some market observers, however, say US HY may look expensive and may continue to do so: limited supply is expected to continue, given a weak M&A calendar and major refinancing deals already done, and also because of strong competition from the loan market. Floating rate loans have become increasingly popular in the belief that they may protect investors from rising rates. The ongoing trade wars have also helped increase the gap between IG and HY, as HY issuers tend to be more domestically focused and less internationally exposed. For how long?

Commodities – trumped: Copper, silver and palladium were some of the commodities to post losses over the past five trading days, hit by the escalation of the US-China trade tensions. Metals suffered a double blow as they are included in the latest list of products that face new US tariffs, as well as from potential lower demand from China, the world’s largest consumer of commodities over the past decade. Currencies of commodity-exporting countries dropped: Chilean peso lost 0.3% over the past five trading days against a falling dollar on concerns that its copper exports could be challenged.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

18 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox