Panoramic Weekly: EMs 1 – Trump 0

Despite US president Trump’s plans to build walls between countries and impose barriers to global trade, the asset class which was once seen as the most vulnerable to his policies not only has emerged victorious in July – but also since he won in Nov. 2016: Emerging Markets (EM) fill 9 of the 10 best-performing fixed income asset classes in July, as their improving fundamentals and recent sell-off have made some valuations attractive, luring investors back into the asset class. EMs are also among the top performers since Trump won the election in November 2016: Mexican government bonds have returned 21% since, the 2nd-best rank among a group of 100 fixed income asset classes tracked by Panoramic Weekly. They only lag US Non-Agency Residential Mortgage-Backed Securities, which have gained on the back of improving US and global economic growth.

July’s general risk-on mode continued over the past five trading days as its sweet-spot conditions were bolstered: global trade tensions waned after the US and the Eurozone agreed to both reduce tariffs towards zero; US economic growth accelerated to 4.1% in the second quarter, the fastest pace since 2014, but sufficiently below expectations to keep the US dollar flat, and to quieten those calling for tighter US monetary policy; the European Central Bank (ECB) and the Bank of Japan (BofJ) also confirmed their supportive, easing programmes, underpinning traditional risk assets; and oil, a key and expensive import for many EMs, eased to US$67 per barrel, down from $70. On the other hand, European sovereign bonds suffered as Eurozone inflation accelerated to 2.1%, the fastest since 2012.

Heading up:

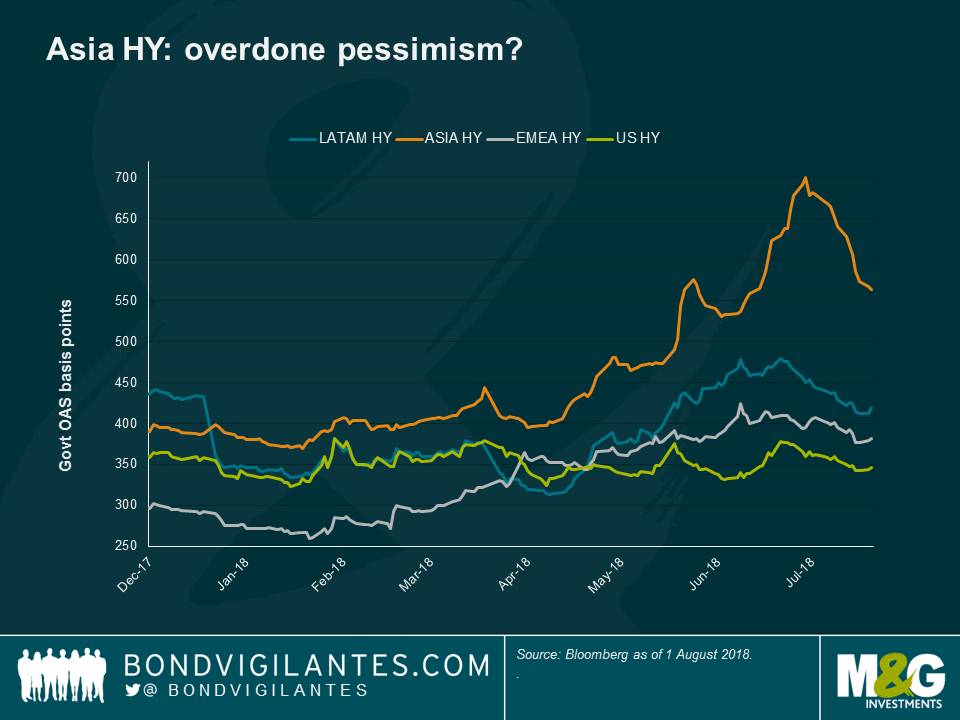

Asia HY – back with force: Asian HY bonds gained 1.6% over the past five trading days, enough to erase previous losses, bringing their 12-month return to a breakeven level. The asset class had widely sold off earlier this year, especially as the China-US trade tensions intensified, raising concerns that Chinese exporters, and their regional neighbour suppliers, would be hit by the new US tariffs on Chinese products. The tensions seemed to stall towards the end of July, especially after the US-EU trade agreement. US-dollar denominated Asian HY names were also supported by a new battery of Chinese fiscal measures, aimed at helping corporates at the same time that the government tries to rein in surging credit. The recent sell-off has also made some valuations attractive: the spreads of some Chinese property names reached as much as 800 basis points over Treasuries, a level that, according to some investors, had a total disconnect with their fundamentals – some provided double-digit returns in July. According to the World Bank, China has already overtaken the US as the world’s No. 1 economy on a purchasing power parity basis. Learn more about EM bonds’ performance and outlook in this Q&A with fund manager Claudia Calich.

Indian bonds – good hike: Locally-denominated Indian sovereign bond prices rose, despite the central bank’s increase in its benchmark interest rate by 25 basis points to 6.5%. At an annualised 5%, inflation is running above the bank’s 4% target. However, the central bank kept its neutral stance, relieving investors who feared that this year’s second hike would be the beginning of a tightening cycle. The move pushed down the sovereign 10-year yield to 7.7%, a three-month low, and strengthened the rupee to 68.4 units per US dollar, the strongest since June. Some investors, however, are still concerned about the country’s budget deficit, especially ahead of next year’s general election.

Heading down:

US Super Retail – choose your 501s: The risk premium that investors demand to hold US Super Retail bonds over Treasuries rose in July – while it narrowed for all the other 16 categories within the asset class. US Super Retail sector extended its three-month slump, hit by rising leases, online competition, continued mall traffic declines, and the difficulty of attracting screen-glued millennials. Shoppers of all ages continue to favour the ease of a mouse click over a trip to the shops, no matter how glamourous it might appear: some of the worst performing HY names in July included a high fashion store chain and women’s lingerie brands. More resilient were some well-established jeans makers, such as Levi Strauss – with a 1.5% excess return over Treasuries in July, its bonds seemed to be a better fit for investors. To learn more about the retail digital shift, read Stephen Wilson-Smith’s “Where have all the shops gone?”

Yen – yawn meeting: The yen was the worst-performing developed market currency against the US dollar over the past five trading days, dragged down by the central bank’s commitment to its ultra-loose monetary policy earlier this week. The move denied previous speculation that the bank would remove its present lid on 10-year yields, a move that would have most likely steepened the yield curve, helping bank profits and therefore improving the flow of credit into the economy. But none of this happened as inflation continues to be subdued; in fact, the Bank of Japan cut its inflation forecast for this year, 2019 and 2020. Investors will have to wait a bit more for some action.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox