Emerging Markets: 5 key issues to watch in 2019

Emerging Markets (EM) debt had a torrid 2018 as global macro risks (including general geopolitics and trade wars), softer EM growth and idiosyncratic stories (Argentina, Turkey), all repriced relatively expensive valuations at the beginning of the year. Are the new prices a better reflection of fundamentals? This will largely depend on the evolution of 5 key topics.

- China-US – upside surprise? The ongoing trade conflict has been a significant driver of global asset prices as the tension has hit global trade as well as corporate earnings (including Apple). If the present trade talks go nowhere, one should expect further global growth weakness, something which could affect EMs, as we highlighted last summer in “How vulnerable are Emerging Markets to trade wars?” For China, the conflict comes at a difficult time for the economy, as the cost-benefit of additional policy stimulus is lower than it was a decade ago, given the higher leverage in the system – inflation is good to cut debt, but comes at a very high competitiveness cost. Despite the negative headlines, investors should not rule out any potential positive tailwind: the US-China relationship could stabilise this year, having a positive impact on asset prices, including EM debt.

- The US Federal Reserve (Fed) – more dovish, but higher issuance? Markets were quick to price in additional Fed hikes this year, but plunging oil prices, a dovish Fed and lukewarm data has made them now forecast the end of the tightening cycle. However, and in the absence of a significant US slowdown, treasuries appear to be pricing in little risk premia, especially since supply remains healthy – usually a negative for bond prices. US government debt is expected to remain high, given current projections of a US fiscal deficit and also because some natural buyers, including some central banks, have recently diminished their Treasury holdings. China, for instance, is not running big Current Account surpluses any more, hence it has less ability to park those extra dollars elsewhere.

- Elections and idiosyncratic risks – volatility and opportunity: There is a stream of EM general elections scheduled for 2019 which may bring a degree of volatility, and opportunity. In terms of potential market reactions, Argentina’s poll, in October, may be the most binary: pro-market incumbent Macri is likely to seek re-election (bullish outcome), but he might face former President Christina Kirchner (expect a negative market reaction if she wins), while the Peronist Party will also be contending (expect a neutral reaction if they decide to continue the IMF-led adjustment path and a negative reaction if they do not). Other elections in Ukraine (March), Indonesia (April), India (April/May) and South Africa (May), may also bring volatility. In other countries, key elections are now behind, so the focus has shifted towards the implementation (or not) of the promises made – for instance, we are monitoring the progress of Brazil’s much-expected pension reform, while expecting further clarity on Mexico’s economic policies. Elections of course are crucial as government action can either lead to or reduce potential idiosyncratic risks. As ever in EMs, avoiding those – usually the largest underperformers – is paramount. Last year, for example, the worst performers were not linked by any common theme, but suffered from specific, idiosyncratic issues, such as large financing needs (Argentina), plunging oil prices (Nigeria, Ecuador and Venezuela), or an unconvincing fiscal adjustment (Zambia and Costa Rica).

- Commodities – symptom or cause? Despite the common perception of a strong link between oil and EMs, developing nations’ sensitivity to oil prices is rather uneven. Should oil go up, Turkey, India and other importers will see a deterioration in their Current Accounts, while Middle East and other EM oil exporters (e.g. Russia, Nigeria) will benefit. Therefore, oil price volatility is likely to generate diverse asset returns. On the other hand, a significant decline in metal-based commodities tends to have a negative impact on most EMs not only because it hits exporters, but also because it often signals weak demand from importers (like top-consuming China), suggesting slower global growth. For instance, the slowdown in China’s property market has negatively affected steel and iron ore prices globally.

- Corporate fundamentals – the bright spot again? Low corporate default rates and credit improvements of corporate issuers were the bright spot of EMs last year (for more, don’t miss Charles de Quinsonas’ “Emerging Markets High Yield: is there value after the sell-off?”) Stronger earnings and disciplined capital expenditures resulted in a net debt reduction throughout the year: as of the end of June (latest data available), EM corporates’ net leverage was below 2.75x, down from 3.5x times at the peak in 2016. Looking into 2019, we believe corporate fundamentals will start stabilising, at the same time that EM High Yield default rates may pick up slightly to 2 to 3% (from less than 2% in 2018), on the back of tougher macro fundamentals in a few countries, such as Turkey, China and Argentina. Default rates are nevertheless likely to remain below their long-term average.

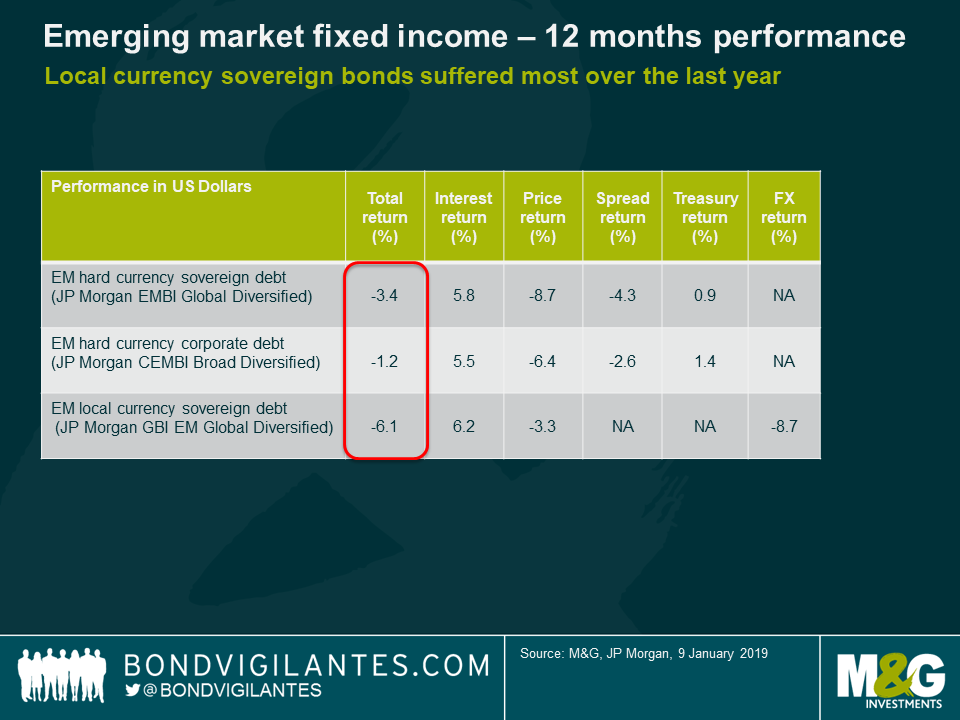

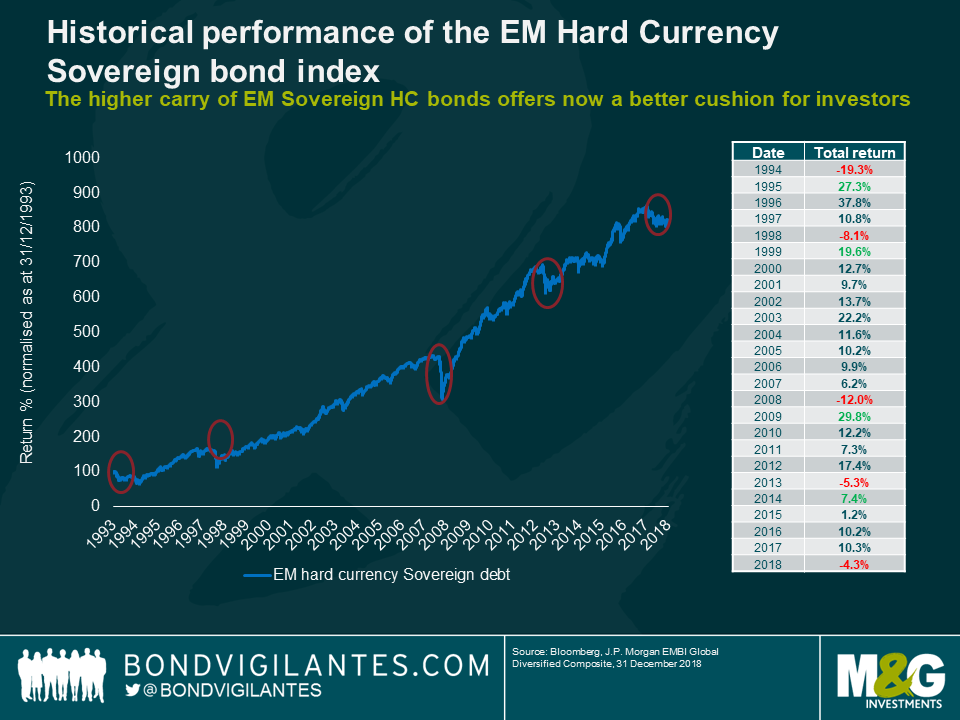

So, whilst global macro risks are unlikely to recede in 2019, the yield on offer by EM debt (around 7% in sovereign US dollar bonds) is at its highest level since the 2007-2008 Global Financial Crisis, raising prospects for improved returns relative to last year. In fact, since 1994, hard currency bonds have never posted two consecutive years of negative returns.

Local debt is a different matter, as currency adjustments often last for a few years depending on the economic cycle, monetary policy and the outlook of the balance of payments. However, and looking at valuations, the Current Account adjustment that has taken place in many countries and the rise in real yields, we believe that the bulk of the local currency correction is behind us. But, since hard currency debt has also cheapened, we remain neutral in terms of allocation between hard and local currency – 2019 will bring opportunities in both.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox