UK gilts – “Whoah we’re half way there, Whoah livin’ on a prayer…”

Last week the Bank of England announced a further round of quantitative easing of £50bn, bringing the total to £375bn. It is obvious that the MPC thinks that monetary policy is still not sufficiently loose to create the desired economic effect and hence further stimulus is needed.

We have written numerous times on QE. When we started scribing on this novel experiment we focused on why it needed to be done, and how it was meant to work (like walking on custard) and the bizarre effect this may have on the bond market.

One thing we did not focus on was the length of time monetary policy would have to be kept super accommodative, though we did expect it to be for an extended period of time (certainly until we begin to see a meaningful recovery in employment outcomes as outlined here).

Mervyn King appears surprised by the extent of the crisis. The MPC were slow in aggressively cutting rates after the onset of the credit crunch in 2007, but to his credit Mervyn and the UK authorities have been at the forefront of corrective action and have correctly realised the severity of the credit crisis. The MPC was correct to not interpret the inflation scare of 2008 or the economic rebound of 2009 as economic recovery. They have been spot on.

But how accurate is his current thinking?

The Governor is not one to pre-commit. However he did say something recently that shows how he feels about the potential long term outlook for rates. At the latest Treasury Select Committee he repeated that at this point in time – and he has said it at every committee meeting – that he believes we are not yet half way through the crisis.

“When this crisis began in 2007-2008, most people including ourselves did not believe that we would still be right in the thick of it, in the middle of it, quite this late. All the way through, I’ve said to this committee that I don’t think we are yet half-way through – I’ve always said that and I’m still saying it.” Mervyn King, June 26, 2012.

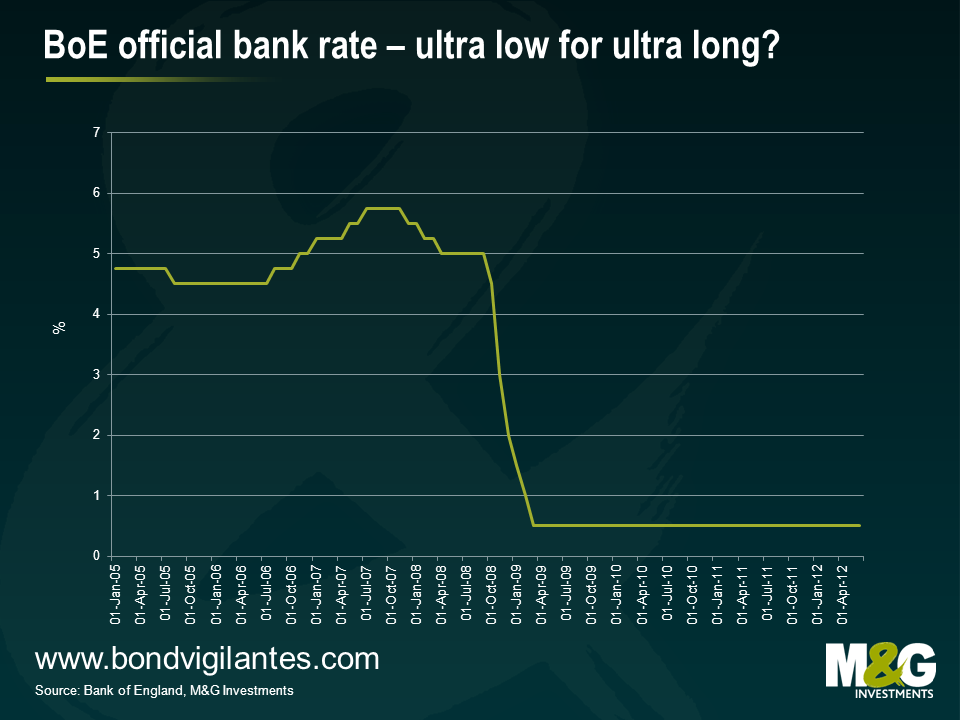

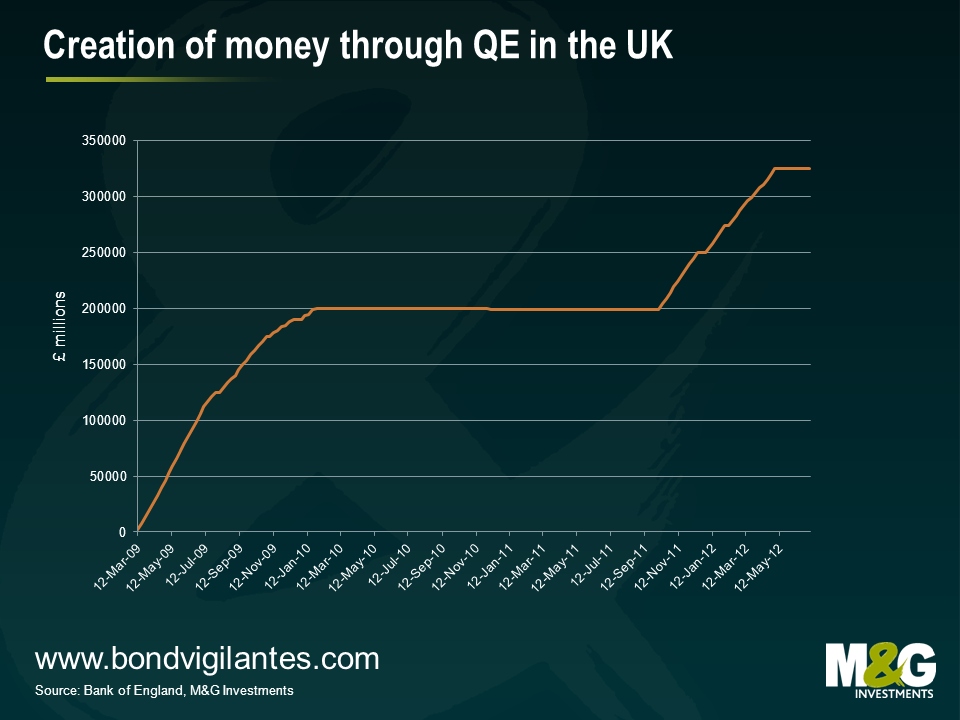

From the chart below we can see that BoE base rate has been set at 0.5% since March 2009, and over £325bn has been pumped into the financial system through QE. If we are not yet half-way through this crisis, then this implies that rates will stay at these levels for at least another 3 years to 2015, and a further round of £375bn of QE is potentially on the agenda.

If this interpretation of the outlook turns out to be correct then these very low levels of short and long term gilt yields begin to look more logical to gilt investors. And we can assume that the UK won’t recover fully until the US and Europe does as well, which means that ultra low yields on Treasuries and Bunds may also make sense.

Monetary policy is living on the edge, and if Mervyn King were to do a turn at a city karaoke machine, then the bar could well be ringing out to this Bon Jovi classic…

“Whoah we’re half way there, Whoah livin’ on a prayer…”

Naturally, his audience of gilt investors – despite the ultra low yield they are currently receiving – will sing back “We got to hold on to what we’ve got”.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox