Brazil trip notes – first-hand feedback from the EM desk

I just returned from a week-long research trip in Brazil where I met with several local investors and corporate bond issuers. From a fundamental standpoint, I came back more bearish on the country’s fundamental outlook. The macro outlook is challenging and low growth and high interest rates are taking their toll on various sectors. Policy risk is elevated with the new Lula government and the bond market is pricing it to various degrees. Against this backdrop, we favour local currency over hard currency in Brazil but find opportunities in high-yield corporate bonds issued in US dollar in sectors that benefit from global trends (e.g. China reopening) and some idiosyncratic stories less correlated to the Brazil macro noise.

Politics have taken centre stage. The new Lula administration has not been well received by the business community at all. For context, Lula was particularly vocal about the central bank during my trip. At best some corporate issuers and a few local investors expect words to not be followed by action and some said that the new Finance Minister, Fernando Haddad, in private was much more sensible than the government public statements. Other investors expect the worst from Lula with fiscal slippage on the back of increased government spending to revive growth and they do not give him the benefit of the doubt. Lula is seen as an excellent politician and locals believe he will be able to secure a majority at the Congress. Brazil’s political checks and balances may therefore be weaker than the counter-powers facing left-wing governments in Chile, Peru or Colombia (the Latam pink tide). On the positive side, a consensus emerged that Lula was taking Brazil back onto the international stage and that investments in the green economy and protection of the Amazon forest were much needed. Interestingly, absolutely no-one mentioned the Brasilia riots during my trip.

The macro outlook is challenging and Brazil has been facing a mini credit crunch since the beginning of the year. Growth is expected to slow down materially, from 3% last year to 0-1% in 2023. Inflation has been slowing down (5.77% Jan. print) but should remain in the mid-5% for the full year. Against this backdrop, local interest rates are very elevated at 13.75% and should remain so for longer – likely until the summer. Low growth combined with higher interest rates are hurting most companies. Whilst mortgages and consumer NPLs are on the rise, this is not a worry for the moment because individuals have fixed-rate loans. More worrisome, companies are heavily loaded in local floating-rates notes – bank loans, and double-digit rates have been making debt service a challenge in the context of low growth. The recent default (USD and local bonds) of Lojas Americanas – one of Brazil’s largest retail chains – is seen as a one-off by most market participants because it was likely related to fraud (under-reporting of $4bln of supplier financing debt). Nevertheless, it added fuel to fire and has made investors and, in particular, local banks very nervous about corporate governance across the Brazilian complex. The surprise hiring of a financial advisor by Light SA, a large utility in Rio de Janeiro, also took the local market off-guard.

For the USD bond market in Brazil, risks are skewed to the downside because the sovereign dollar curve looks not to be pricing a scenario where the new Lula administration under-delivers for the budget announcement (growth agenda vs fiscal anchor). Therefore, we find hard-currency sovereign debt expensive. State-owned companies’ bonds similarly look unattractive for the most part with very tight spreads over sovereign, in our view not pricing in Lula’s policy and vertical integration risks. This is particularly true in the oil and gas sector. In the corporate space, high local rates for longer in the context of low growth would lead to more defaults locally, itself increasing the risk of a credit crunch.

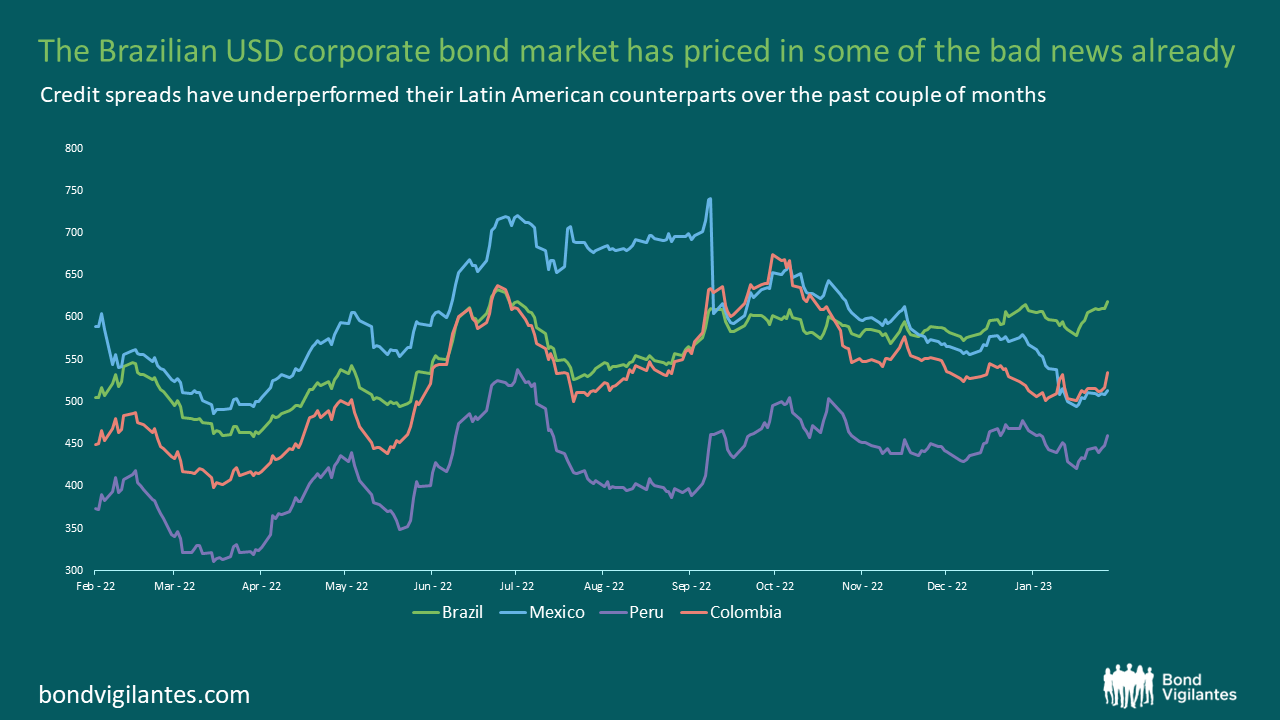

The Brazilian USD corporate bond market has nonetheless priced in some of the bad news already with credit spreads underperforming their Latam counterparts in the past couple of months (see chart above) and they also trade wide against their 5-year average. This creates investment opportunities in sectors which have been holding up well, such as miners (a China reopening story), the agribusiness, or the more niche private healthcare segment. On the other hand, we remain cautious when it comes to the logistics and consumer sectors because of high interest rates locally and the low growth outlook.

We currently find more value in FX: Brazil’s strong balance of payments and the expectation of higher rates for longer should support the Brazilian Real. Rates also offer high positive real yields (nominal yields adjusted by inflation expectations) after the central bank of Brazil adopted a proactive approach to increasing rates ahead of the Fed in the past couple of years. However, we are slightly more cautious on rates than FX as we don’t discount the risk that the governor of the central bank leaves or negative macro and/or political developments materialise in the short-term (e.g. inflation target, budget announcements). In a worst-case scenario, a saying I heard from a local investor during my trip comes to mind: “we Brazilians are very often at the edge of the cliff, but we never fall”.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.