The inflation spark that could become a deflation shock?

Memory chips have quietly become the most important commodities in the global economy.

DRAM (Dynamic Random Access Memory) is considered the workhorse of the digital world. It functions as the operating memory when a device is turned on, and this memory is lost when a device is switched off. These chips are used in almost all electronic devices. They play a critical role and sit at the heart of everything from AI servers, cars, smartphones, laptops and more.

The Nvidia type of chips – GPUs (Graphics Processing Units) – are used for computational purposes but are also heavily reliant on DRAM chips.

Many will be aware of the rise of semiconductors and the rapid ascent of Nvidia but few will be aware of the changes ripping through another part of the semiconductor industry: DRAM chips, which have a very direct effect on all of our everyday lives. When Covid disrupted supply chains, we saw all sorts of issues from price increases to availability of goods. Remember when the price of second hand cars were trading at levels close to new cars as the old cars had the necessary chips, while new ones had to go without.

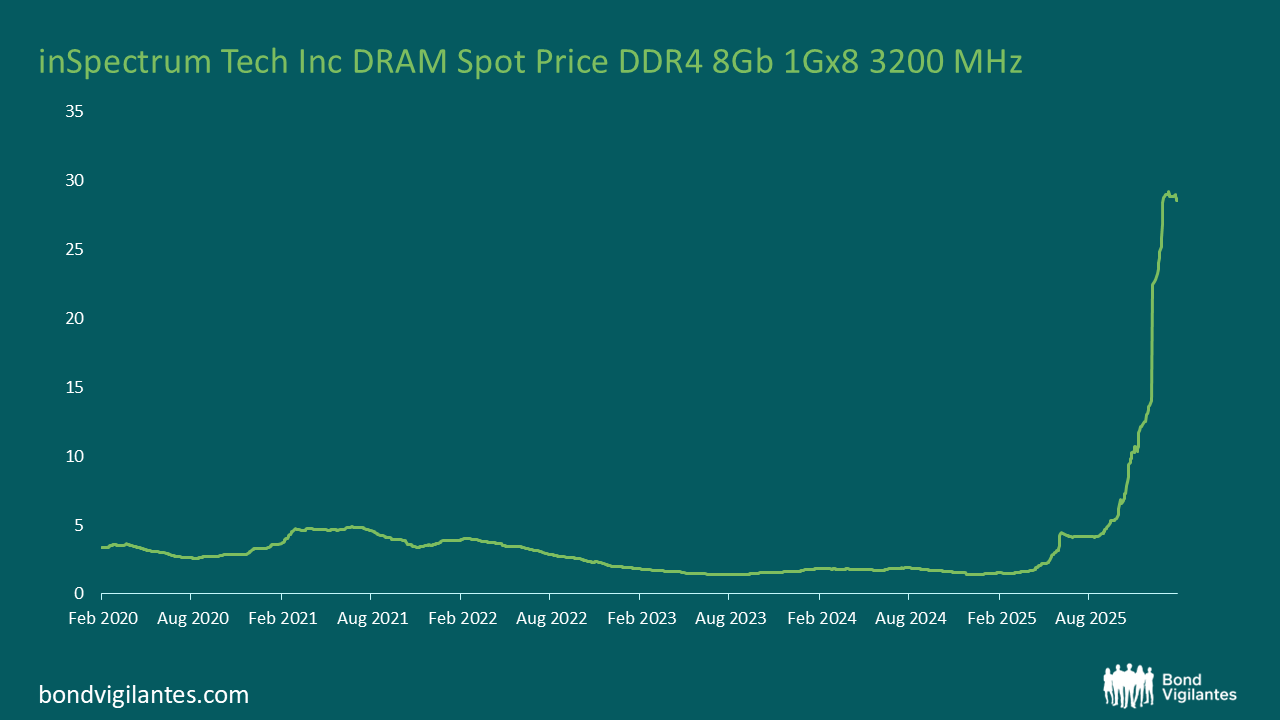

Source: Bloomberg Indices ( Ref. ISPPDR37 index, inSpectrum Tech Inc DRAM Spot Price DDR4 8Gb 1Gx8 3200 MHz) accessed as of 25th February 2026 .

The price of these memory chips has exploded in recent months, helping explain why the Korean Stock Exchange has had such a good run with Samsung and SK Hynix making up circa 35% of the index.

Today’s tight memory market raises a fascinating macro question: Is this inflationary fuel for the global economy or are we at the early stages of a deflationary unwind?

The inflation case: scarcity breeds pricing power

When memory supply tightens, the first-order effect is straightforward: prices rise. The companies that benefit most are the manufacturers themselves, such as Samsung Electronics, SK Hynix and Micron Technology.

The memory market is one of the most cyclical industries in the world. When utilisation rates climb and inventories shrink, pricing power flips dramatically in favour of producers. Margins can expand quickly.

Higher memory prices feed directly into AI servers, cloud infrastructure, PCs, TVs and smartphones, networking equipment and vehicles. For AI in particular, memory is a major component. High Bandwidth Memory (HBM), a subset of DRAM, is essential to modern GPUs. Companies like Microsoft, Tesla, Meta, etc. depend on large volumes of high-performance memory to make their flagship accelerators function as designed.

If memory becomes more expensive, server build costs rise, cloud capex increases and hardware prices edge up. In that sense, the shock is inflationary, a classic cost-push dynamic. And because AI infrastructure investment is currently driven by deep-pocketed hyperscalers, demand is not especially price sensitive. Higher input costs don’t immediately suppress investment. They often get absorbed. That’s inflationary pressure in action. The issue of higher prices falls heavily onto all the other non-hyperscaler corporates.

The deflation counterargument: when scarcity and price choke growth

But what if availability becomes the issue, not just price?

Imagine a scenario where non-hyperscalers simply cannot secure memory chips to build products as a result of availability and price due to the hyperscalers apparent insatiable demand. Production lines stall, revenue slows and inventory sits half-finished. For highly levered firms with large fixed costs, that becomes dangerous, very quickly.

Unlike the large technology companies with bucketloads of cash and the ability to tap credit markets, smaller firms lack a balance sheet buffer. This is where the recession transmission emerges through demand destruction. Insolvencies begin to rise, unemployment increases and credit spreads widen. With credit spreads trading at all time tight levels, we need to be cautious.

Time is currently the enemy. The longer chip prices remain elevated the more macro consequences we can expect. It certainly doesn’t feel like these deep pocketed technology firms are going to be backing away anytime soon. In fact, Google raised $32bn in multiple tranches at the drop of a hat the other day. The 100yr sterling tranche was massively oversubscribed. A £5.5bn issue attracted £30bn in bids.

Let’s keep a close eye on the industries that rely on these chips, with a particular focus on credit spreads and unemployment levels.

Unhelpfully, we are left wondering in which direction inflation will turn next? If you were a gambler, where would you put your chips?

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.