Asian currency markets in the Year of the Fire Horse; ready to gallop?

Asian currency markets enter the Year of the Fire Horse at a delicate but potentially consequential juncture.

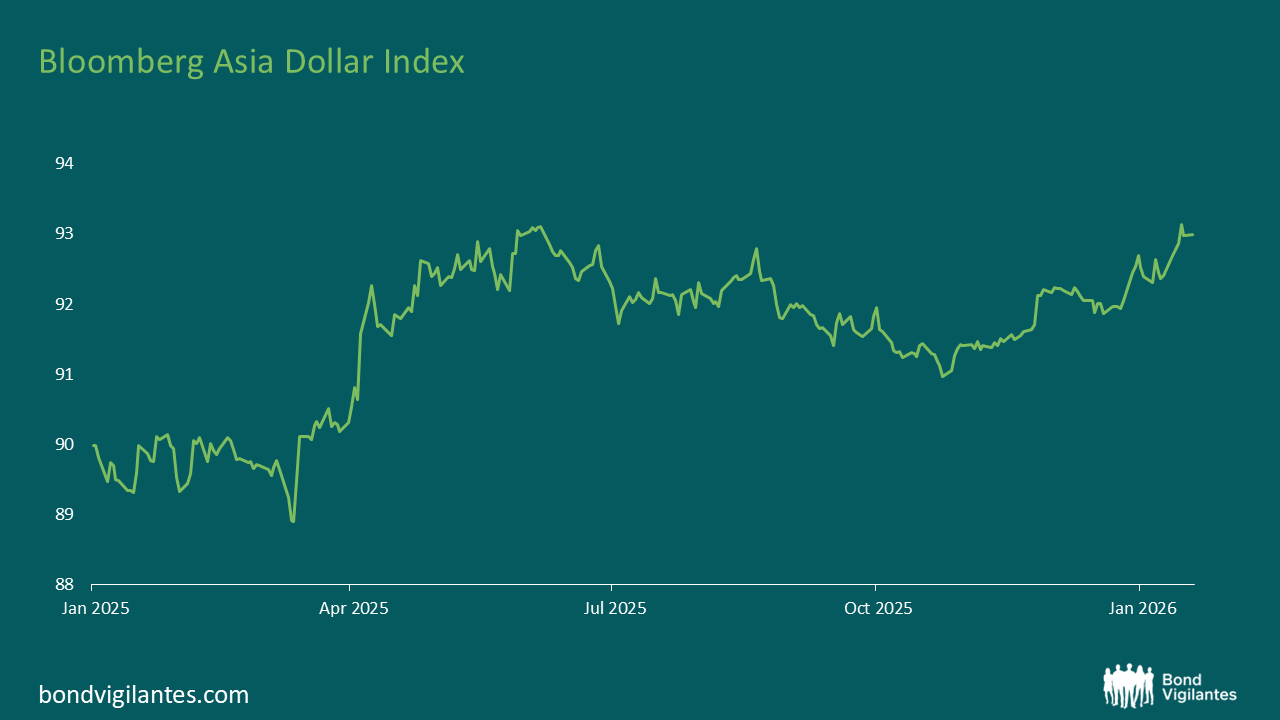

The Year of the Green Wood Snake closed on firmer footing. After four consecutive years of depreciation against the US dollar, Asian currencies edged cautiously higher. The Bloomberg Asia Dollar Index rose more than 3% over the last Lunar Year , a steady but deliberate ascent, much like a coiled snake gradually rising.

Source: Bloomberg, February 2026

Yet beneath that aggregate recovery lay sharp divergence. The Malaysian ringgit appreciated more than 12% against the greenback, while the Indian rupee declined nearly 5% over the same period. Even at the regional level, Asian currencies continued to lag broader emerging market peers. This serves as reminder that the recovery was partial and that the relative underperformance is instructive. The Snake year was defined less by resurgence and more by cautious rebuilding.

If the Snake year was characterised by patience and gradual repair, the Fire Horse suggests a change in tempo.

In the lunar calendar, the Fire Horse is associated with intensity, speed and sudden shifts in direction. Unlike the deliberate ascent of the Snake, the Horse carries momentum. In 2026, that symbolism resonates with the possibility that Asian currency markets may be approaching a turning point – where stronger trade dynamics and evolving capital flows begin to carry more weight relative to the US dollar. In that sense, 策马扬鞭 (spur the horse and raise the whip) – urging the need to press forward quickly – captures the spirit of the moment.

This year also carries a rare ‘Double Fire’ element, which is traditionally associated with heightened energy and volatility. In market terms, that parallel may lie in the interaction of resilient trade surpluses and shifting portfolio allocations. When both gather pace simultaneously, movements across regional currencies can become more forceful and less incremental.

Acceleration, however, does not imply uniform speed or direction.

Three interconnected forces could shape the trajectory: the AI-driven reshaping of trade flows, the potential reconfiguration of capital allocation, and differentiated domestic dynamics.

Saddling the AI cycle: from innovation to external balance

The Fire Horse’s symbolism of speed aligns naturally with the current artificial intelligence (AI) investment cycle – but the relevance for Asian currency markets lies in how that cycle feeds into trade performance and regional resilience.

AI is no longer merely a thematic equity driver. It is reshaping trade volumes and corporate capital expenditure – developments that matter directly for currencies.

Demand from the AI wave — spanning semiconductors, high-performance servers, networking equipment and data centres — continues to drive substantial investment by companies globally. The emergence of increasingly “agentic” AI models capable of autonomous multitasking, reinforces expectations of sustained productivity gains and corporate spending.

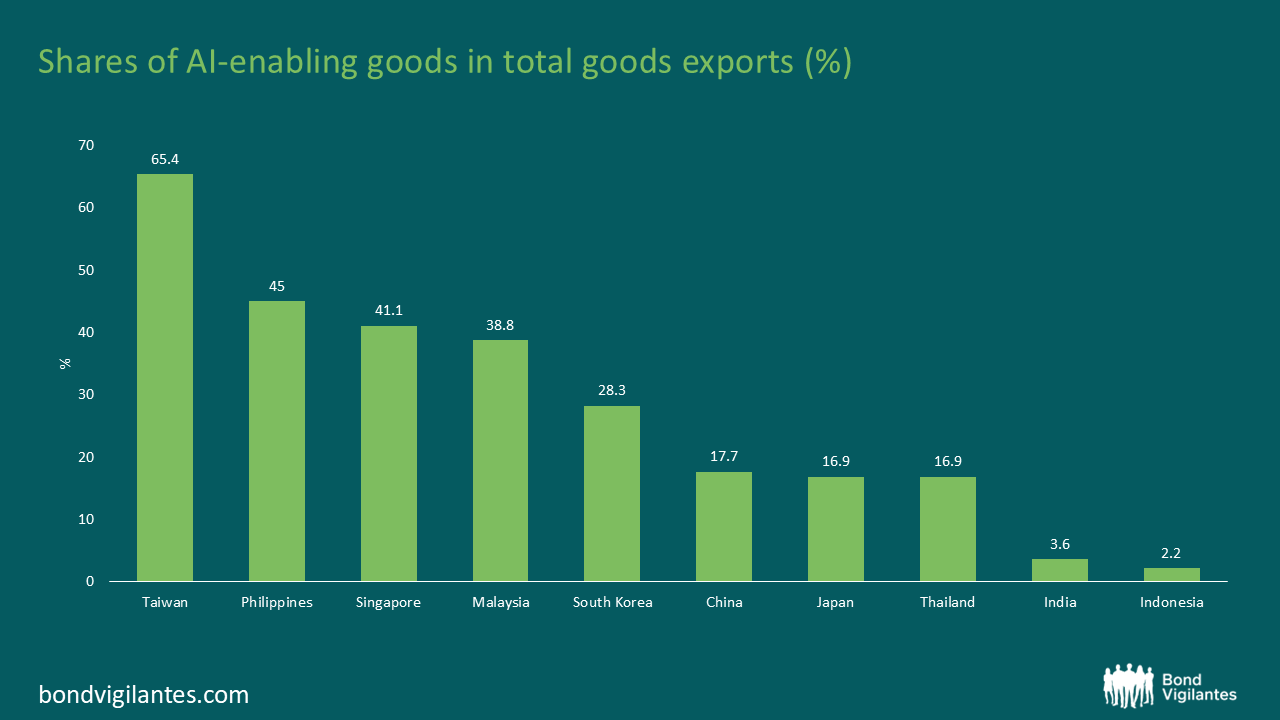

Asia occupies a central role in this transformation. While the US leads in foundational large language models, Asia functions as the hardware backbone of the global AI ecosystem. According to the World Trade Organisation, the region accounted for nearly two-thirds of global AI-related trade growth in H1 25, with AI-enabling exports forming a significant share of total exports in 2024.

The impact is increasingly visible in external accounts. The region’s aggregate current account surplus rose to an estimated 4.5% of GDP in 2025, compared with around 2.3% over the preceding five years. Korea and Taiwan recorded record surpluses, while demand for legacy chips supported economies across the broader semiconductor value chain, including Malaysia, Singapore, Thailand and the Philippines – markets benefiting from assembly, testing, data-centre investment and related supply-chain activity.

Source: World Trade Organisation, ITC Trademap, CEIC and Nomura Global Economics. Data as at 2024.

For Asian currency markets, stronger trade performance provides a more supportive external backdrop. Beyond exports, rising foreign direct investments into AI-related fields in Asia, including digital infrastructure and data centres, also supports capital flows.

That said, expectations around AI remain elevated and capital expenditure cycles are inherently cyclical. Exposure across the region differs – from advanced semiconductor fabrication in Korea and Taiwan to assembly, testing and related supply-chain activity in Southeast Asia. The benefits are real, but unlikely to be evenly distributed.

As with previous technology cycles, momentum can shift quickly. A moderation in investment or a reassessment of earnings expectations would likely introduce volatility into both trade flows and regional currencies.

Changing reins: when surplus savings shift

In that context, Asia’s surplus recycling dynamic becomes critical.

For decades, the region has generated current account surpluses, yet a substantial portion of those savings has been invested in US financial assets. The US share of Asia’s overseas investments rose from 37% in 2020 to a peak of 41% in late 2024 before easing modestly in 2025 to 40%.

This pattern has historically supported the US dollar, but in an environment marked by geopolitical uncertainty and evolving monetary policy expectations, diversification away from US assets remains under discussion.

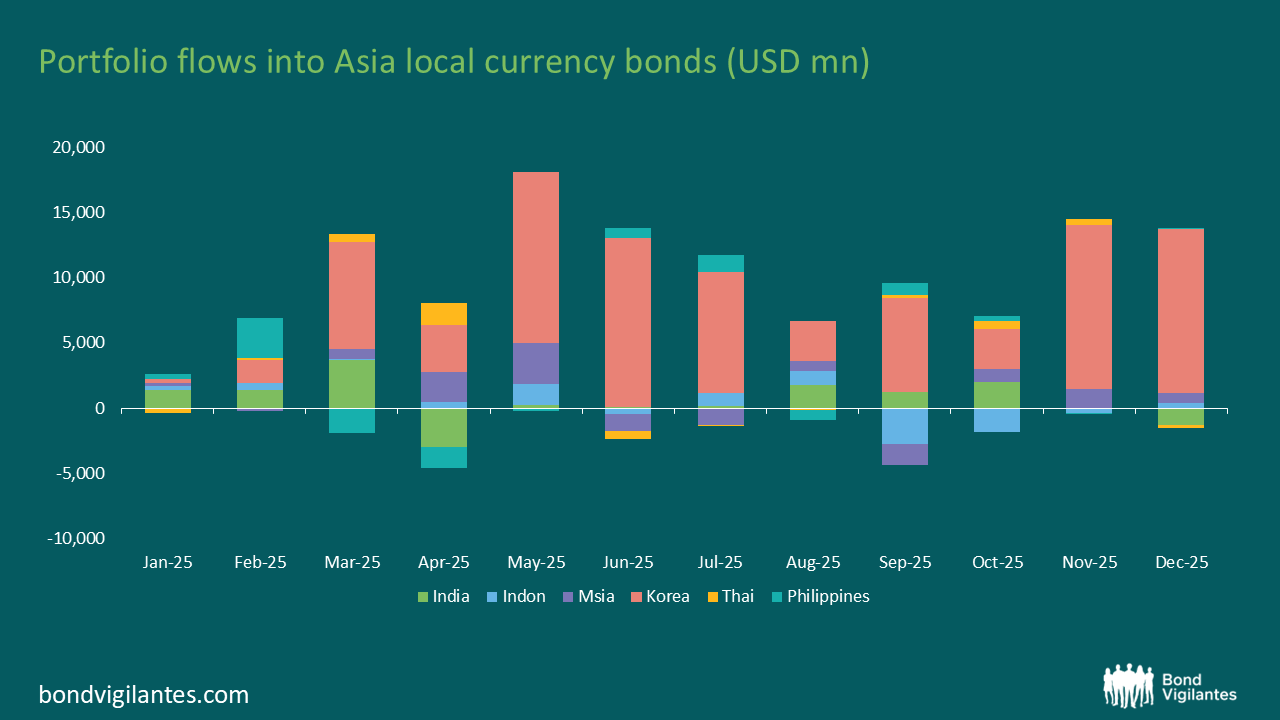

Recent episodes illustrate how sensitive currency markets can be to shifts in allocation. In Q2 25, uncertainty surrounding US policy contributed to inflows into Asian local currency debt. Over the same period, regional currencies appreciated by around 4%.

Source: Bloomberg, February 2026

With investor positioning in Asian bonds and currency markets still relatively light, scope remains for further inflows. A shift in hedging behaviour could reinforce this trend. Should expectations of Federal Reserve easing materialise, higher hedge ratios on US assets would mechanically generate additional USD selling.

Even so, capital flows are rarely linear. Shifts in global risk appetite or policy expectations could just as quickly reverse recent momentum.

Each horse runs its own race

Macro themes may set the track, but domestic fundamentals ultimately determine outcomes. Dispersion remains a defining feature of Asian currency markets.

The Malaysian ringgit, the standout performer of 2025, staged a dramatic recovery from record weakness in 2024. Structural reforms, improved policy stability, economic diversification, and AI-linked capital expenditure combined to drive appreciation. Gains from here may prove steadier rather than explosive, but the foundations appear firmer than in prior cycles.

The Korean won, by contrast, presents a different profile. Despite deep exposure to the AI capital expenditure cycle, which provides upside leverage, domestic outflows have at times tempered performance. The inclusion of Korea Treasury Bonds in the FTSE World Government Bond Index in April 2026 could attract meaningful inflows, while corporate governance reforms may gradually support sentiment in the equity market.

The Indian rupee follows a different trajectory. Its performance is less tied to the AI cycle and more anchored in domestic factors, Indian domestic bonds provide an attractive source of income, supported by comparatively high nominal and real domestic bond yields relative to other Asian markets. Domestic fundamentals – including fiscal consolidation and an inflation targeting framework – help anchor macro credibility. A recent sovereign rating upgrade by S&P to BBB (from BBB–) marked its first upgrade in 18 years, reinforcing perceptions of macro stability.

Elsewhere, not all domestic stories are aligned. Moody’s downgrade of Indonesia’s sovereign rating outlook due to governance concerns and an ongoing corruption investigation in the Philippines serve as reminders that domestic developments remain critical in differentiating outcomes.

In a year characterised by speed and shifting leadership, relative performance may change quickly – but dispersion is likely to persist. Remaining nimble is key.

Holding the reins

Improved fundamentals do not imply a straight-line rally.

Shifts in US trade policy illustrate how quickly legal or procedural adjustments can reshape market expectations. Even incremental changes in tariff implementation or regulatory interpretation can alter capital allocation decisions and risk sentiment, with spillovers into currency markets.

There are also risks embedded in elevated AI expectations. The current investment cycle rests on assumptions of sustained productivity gains and corporate monetisation. If earnings delivery lags investment intensity, or if global demand softens, trade momentum could moderate more abruptly than anticipated.

Financial conditions also matter. A reassessment of the expected Federal Reserve easing path, renewed US dollar strength, or tighter global liquidity conditions could constrain capital inflows into the region, even where external balances remain sound.

As the Monetary Authority of Singapore noted in its 29 January 2026 Macroeconomic Review, a synchronised correction in AI investment cannot be ruled out if productivity gains prove harder to monetise.

In periods of rapid change, discipline becomes critical. 老马识途 (the old horse knows the road) is instructive. Speed may define the year, but navigation determines the outcome.

The road ahead

In recent years, Asian currency markets have often played a secondary role in portfolio construction, overshadowed by equities and bonds. The Year of the Fire Horse may test that hierarchy.

The combination of resilient trade performance, evolving capital allocation patterns and healthy (albeit differentiated) domestic fundamentals in Asia creates conditions under which regional currencies could assume a more prominent role.

The Fire Horse symbolises momentum, acceleration and intensity, which could signal greater heights for Asian currencies. However, the path may not be smooth and may diverge at times in such period of rapid changes. Being disciplined and nimble will be key in seizing the opportunities.

A version of this blog was first published in The Edge Singapore on Friday, 27 February 2026.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.