The US Dollar: from exceptional to average?

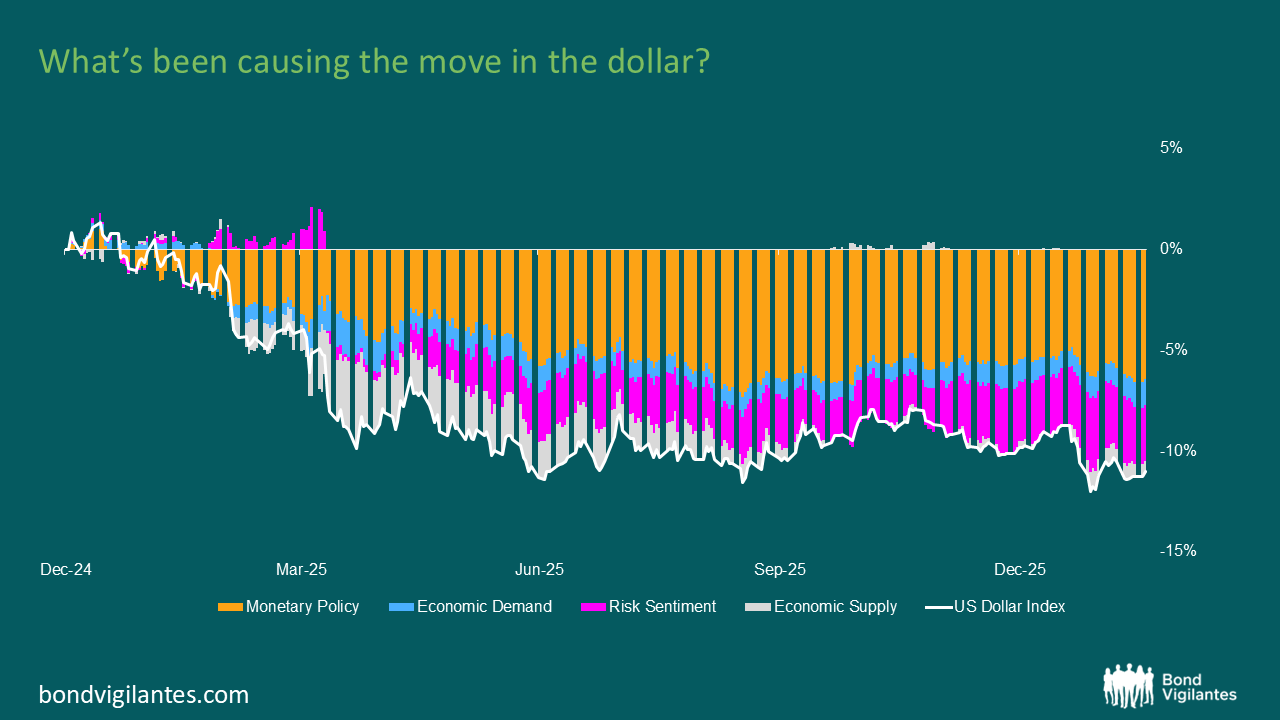

The dollar’s slide last year looks less like a sudden break and more like the culmination of pressures that have been gathering for a while. The fading of US exceptionalism has sat quietly in the background, and once the narrative started to normalise, the cracks became clearer: softer growth expectations, slower capital inflows, and valuations that had been leaning heavily on the idea that the US could keep outperforming indefinitely. The currency came into the year heavily owned and reliant on that growth premium, and when it began to erode, the dollar suddenly felt far more exposed to shifts in sentiment and positioning than it had for some time.

At the same time, the policy backdrop has turned more awkward for the currency. Markets expect the Fed to continue cutting, and the prospect of a more politically influenced leadership has introduced a small but noticeable risk premium around credibility. That is happening just as fiscal policy remains unanchored, with deficits showing little sign of narrowing and spending likely to rise into the election cycle. The steepening we’ve seen in the curve has not offered the dollar much support. Even when nominal yields tick higher, the lack of a credible fiscal path blunts the rate‑differential argument the currency would otherwise be able to lean on.

Trade policy hasn’t helped clarify matters either. Ordinarily, higher tariffs would tighten the inflation narrative and lend support to the dollar, but the market seems to be treating recent announcements with a degree of caution. The reversals, the unpredictability, and the simple fact that these things take time to feed through the system have meant the FX impact has been surprisingly muted. Rather than helping the dollar, tariff headlines have added to the broader sense of uncertainty.

Source: M&G, Bloomberg intelligence.

All of this has fed into the gentler tone around inflation expectations. Long‑dated breakevens suggest a market that is comfortable (perhaps too much so) with the idea that inflation pressures will remain contained. For the dollar, that matters: when inflation is assumed to stay under control, rate differentials compress, and one of the currency’s key supports weakens. A shift in those expectations, whether driven by tariffs or other factors, could prompt a repricing. The more challenging scenario would be one where inflation starts to firm again, yet the Fed continues to ease. That combination would weigh heavily on real yields and raise questions about policy direction and central‑bank independence at a moment when confidence is already fragile.

Against this backdrop it’s no surprise that traditional valuation anchors feel less dependable. Too many competing forces such as policy, flows, and politics, are pulling at once. If the Fed keeps cutting and differentials narrow, a softer dollar is the natural outcome unless other central banks ease more aggressively and/or for longer than expected. And while this doesn’t yet resemble a structural rotation away from the dollar, the combination of drivers could support a gradual diversification at the margins. Reserve managers are still operating within clear limits with USD markets remaining the core of the system, but increased accumulation of alternatives, particularly gold, fits with the broader theme.

Taken together, this episode looks both political and structural. Politics has accelerated the move, but the foundations were already in place: the normalisation of US exceptionalism, the awkward policy mix, and the evolving inflation and reserve‑management dynamics. How long those forces persist will shape the dollar’s path into the next decade. It doesn’t yet feel like a dramatic turning point, but nor does it look like an interruption that will snap back quickly. The more plausible path is a slower, uneven adjustment as the market works out what the right premium for the US actually is.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.